Withholding Tax in China

By Dezan Shira & Associates

Editor: Jake Liddle

In China, withholding tax (WHT) is levied on the income of foreign enterprises that do not have a physical establishment in China but provide services to China-based businesses. Any China-derived income arising from such a transaction between an overseas entity and a Chinese business is withheld by the China-based client, deducted from the gross income amount, and taxed by the Chinese tax authorities at a flat concessionary rate of 10 percent.

Thus, it is the responsibility of the China-based client to ensure the transfer of tax onto the tax bureau. If they fail to do so, or do not pass on the correct or relevant amount from an invoice, the local tax bureau will take up repayment with the China-based client, and not the overseas entity.

![]() RELATED: The BEPS Action Plan in China and Hong Kong

RELATED: The BEPS Action Plan in China and Hong Kong

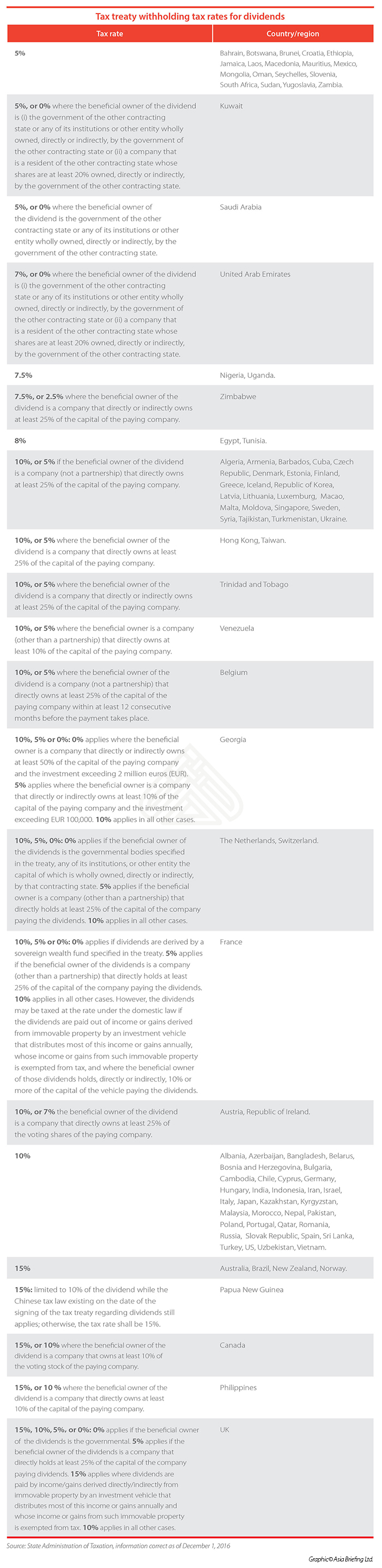

According to China’s Corporate Income Tax Law (2008), passive income of non-tax resident enterprises in China is taxed at 20 percent, though this was reduced to 10 percent in the detailed implantation regulation of the law. This rate is applied to any dividends obtained by an overseas entity from a resident company. However, rates vary under the various tax treaties that exist between China and other countries, as shown here:

China’s withholding tax policies have tightened and changed. For non-tax resident enterprises, with or without a physical presence in China, as well as those with income not effectively connected with a physical presence, their China-sourced income is subject to CIT. This includes income deriving from:

- Sales of goods;

- Provision of services;

- Transfer of property;

- Dividends and profit distribution;

- Equity investments;

- Interest;

- Rent;

- Royalties; and

- Donations.

Corporate income tax payable will be withheld at the source, with the payer acting as the withholding agent, who will withhold tax from the amount of each payment when it is due. Therefore, the withholding obligation arises when income is either remitted or when the payer accrues the amount as a cost or expense. Correct calculation of tax liability is as follows:

Withholding tax payable = Taxable income × Tax rate

For dividends, interest, rental, and royalty income, the taxable amount is the gross amount remitted before deduction of any taxes, including business tax. If the withholding tax and business tax is borne by the payer, the amount of income should be added up to produce the taxable income.

![]() RELATED: Audit and Financial Services from Dezan Shira & Associates

RELATED: Audit and Financial Services from Dezan Shira & Associates

For dividends paid overseas, no business tax is levied. For income from the transfer of property, the taxable income amount is the balance of the total income amount minus the net value of the property. For other income, the taxable income amount can be calculated according to the formulae of the preceding two items.

Determining tax liabilities

Though it is common for overseas non-tax resident entities to provide services for clients in China, or their own subsidiaries located there, whether or not withholding tax applies to their transactions is not always clear. Even if it is certain that China-sourced income is subject to withholding tax, the correct tax base and rate still may not be apparent.

Enforcement is not uniform in China, with each case and transaction subject to the discretion of local tax authorities. The actual applicable tax rates are therefore only set once tax officials have completed a review of tax clearance documentation and have issued their final decision.

General taxation frameworks provide only a guideline, and more precise estimations can be obtained by narrowing down to the type of service activities provided by overseas entities. It is advisable that such entities obtain professional consultation when determining the nature of withholding tax for their services.

Editor’s note: This article was originally published on September 22, 2010, and has been updated to include the latest regulatory changes.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email china@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

|

Dezan Shira & Associates Brochure

Dezan Shira & Associates Brochure

Dezan Shira & Associates is a pan-Asia, multi-disciplinary professional services firm, providing legal, tax and operational advisory to international corporate investors. Operational throughout China, ASEAN and India, our mission is to guide foreign companies through Asia’s complex regulatory environment and assist them with all aspects of establishing, maintaining and growing their business operations in the region. This brochure provides an overview of the services and expertise Dezan Shira & Associates can provide.

An Introduction to Doing Business in China 2017

An Introduction to Doing Business in China 2017

Doing Business in China 2017 is designed to introduce the fundamentals of investing in China. Compiled by the professionals at Dezan Shira & Associates in January 2017, this comprehensive guide is ideal not only for businesses looking to enter the Chinese market, but also for companies who already have a presence here and want to keep up-to-date with the most recent and relevant policy changes.

New Considerations when Establishing a China WFOE in 2017

New Considerations when Establishing a China WFOE in 2017

In this edition of China Briefing, we guide readers through a range of topics, from the reasons behind foreign investors’ preference for the WFOE as an investment model, to managing China’s new regulations. We discuss how economic transformations have favored the WFOE, as well as the investment model’s utility, and detail key requirements that businesspeople need to examine before initiating the WFOE setup process. We then walk investors through the WFOE establishment process, and, finally, explain the new and idiosyncratic “Actual Controlling Person” regulation.

- Previous Article China’s New Cybersecurity Law to be Implemented on June 1

- Next Article Changing Tastes: China’s Imported Wine Industry