The China Alternative – Malaysia

The China Alternative is our series on other foreign investment destinations in emerging Asia that may soon be competing with China in terms of labor costs, infrastructure and operational capacity. In this issue we look at Malaysia.

The China Alternative is our series on other foreign investment destinations in emerging Asia that may soon be competing with China in terms of labor costs, infrastructure and operational capacity. In this issue we look at Malaysia.

By Cindy Tse

Oct. 25 – The Malaysian government recently announced an ambitious goal to become a high-income nation by 2020, necessitating equally bold changes to the country’s social and economic policies. The state’s reform program, the New Economic Model, was launched in March of 2010 and involves ambitious schemes to restructure the economy and pull it out of low value-added manufacturing and increase private investment.

The NEM is just one of four economic programs to come out of Prime Minister Datuk Seri Najib Razak’s office in 2010. The Tenth Malaysia Plan will direct the state’s public sector capital expenditures, the Government Transformation Program will address corruption and issues with Malaysia’s social welfare provisions, and the Economic Transformation Programs will be dedicated to spurring growth in foreign and domestic private investment.

Background

Malaysia’s 13 states and 3 federal territories are divided by the South China Sea into the two regions of West and East Malaysia. West Malaysia, or “Peninsular Malaysia,” borders Thailand, while East Malaysia, or “Malaysia Borneo” borders Indonesia and Brunei.

Malaysia is governed as a constitutional monarchy, though Peninsular Malaysian states retain hereditary rulers who are often referred to as “Sultans.” The capital city is Kuala Lumpur, a bustling metropolis of 1.6 million.

Malaysia’s population of 28.7 million is comprised of three main ethnic groups – Malay, Chinese and Indian. As would be expected in a society where multiple cultures and religions co-exist, relations between various groups are not always harmonious. However, in the case of Malaysia, most policy changes have to take into account the effect on the often competing interests of these ethnic groups.

English is widely used as a second language, particularly in the workplace, making Malaysia a relatively easy place for foreign enterprises to operate in. Most Malays are multilingual, with Bahasa Malaysia as the official national language. Various mother tongue languages are spoken as well, such as different dialects of Chinese, Tamil, or Bahasa Indonesia, which is quite similar to Malaysia’s official first language.

Economy

The export-led economy in Malaysia was affected significantly in 2009 by overseas declines in demand for consumer goods brought about as a result of the Global Financial Crisis, though the country managed to bounce back in 2010. Malaysia’s GDP reached US$414.4 billion in 2010 with a high concentration in industrial (10.5 percent) and service sectors (48.2 percent), as well as agricultural production (10.3 percent) in rubber, palm oil, timber, and rice. The industrial sector consists predominantly of rubber and palm oil processing and manufacturing, pharmaceuticals, medical technology, electronics, tin mining and smelting, logging, and timber processing. Malaysia is also a significant oil and natural gas producer, making the country quite vulnerable to fluctuations in oil prices. The government is noticeably dependent on the state-owned oil company Petronas to fill its coffers, as it contributes roughly 44 percent of the government’s revenue.

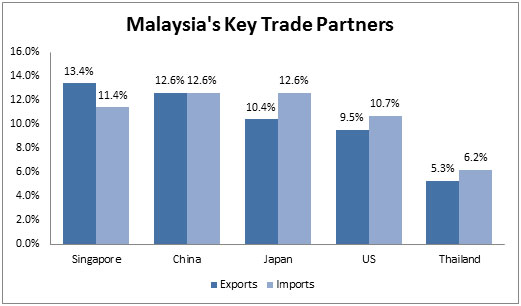

The country’s account balance is in a comfortable position, with its US$34.14 billion surplus ranked 13th in the world – though naturally a minor point when compared with China’s US$305.4 billion surplus. Aside from the United States, Malaysia’s trading partners are highly concentrated in the Asia-Pacific region, with Singapore, China, Japan, Thailand and Hong Kong having the highest shares of imports and exports.

Investment climate

Foreign direct investment (FDI) in Malaysia has climbed modestly over the last 10 years, though growth may reflect the reinvested earnings from existing multinationals that make up a significant share of total FDI.

Given the highly racialized nature of politics in Malaysia, governments throughout much of Malaysia’s recent history have been quite cautious in enacting policies to encourage FDI. Since the 1970s, there has been a “30 percent equity rule” in Malaysia, which requires 30 percent equity of any enterprise to be held by a Bumiputra – an ethnic Malay or indigenous person. The purpose of the policy was to increase Malays’ share of the nation’s wealth to a fair 30 percent. And while the government maintains that it has yet to reach this target (they claim Malay ownership is at 18.9 percent), studies on the subject say the 30 percent target may have already been surpassed.

Since 2009, there have been more and more exceptions to these Bumiputra ownership rules. Investment in the manufacturing sector, 27 non-controversial services sub-sectors, and investment in the Iskander Development Region are exempt. Prior to 2009, all initial public offerings (IPO) on the Bursa Malaysia were required to set aside 30 percent for purchases by Bumiputra. This 30 percent has since been reduced to 12.5 percent for new listings of foreign-owned corporations.

While there are substantial incentives offered by the government to encourage foreign investment, they are not without performance requirements, and they certainly won’t last forever. Specific requirements are incorporated directly into each individual business license for both foreign and domestic investors. These can include export targets, local content requirements, and mandatory transfers of technology.

In 2003, in an effort to increase investment in high value-added sectors, the government extended the existing tax exemption from 10 to 15 years for firms that qualified for “Pioneer Status.” This status is given to enterprises involved in specific geographical regions, as well as products or services deemed by the government to be of high priority for development. There is also a more modest 5 to 10 year tax holiday in some lower priority sectors under the “Investment Tax Allowance” scheme. These incentives are said to be provisional, though it’s unclear when they will expire.

As part of the 2010 Economic Transformation Program, the state has selected 13 sectors in which to boost private investment, though it remains to be seen how welcome foreign participation is in these plans. These sectors include electronics, medical devices, green energy, machinery and equipment, oil and gas, and transportation equipment. Resource-based industries and services like logistics are also targeted sectors.

Doing business in Malaysia

Malaysia ranks relatively high in the International Finance Corporation’s Doing Business rankings in terms of the ease of doing business. In the 2012 rankings for data up to June 2011, Malaysia is ranked 18th overall out of 183 economies; well ahead of China which is positioned at 91st, yet still behind neighbouring Singapore, which tops the rankings.

Malaysia has been climbing in the rankings gradually, bolstered by the ease of getting credit in the country (ranked 1st overall) and its protection of investors (4th). Its recent jump into the top 20 can be attributed to this past year’s dramatic improvements in the ease of starting a business (from 111th in the 2011 rankings to 50th this year) and enforcing contracts (from 60th to 31st).

Starting a business in Malaysia has become significantly faster, easier and cheaper over the last few years. In 2006, it took an average of 37 days, 10 procedures and 25.1 percent of the average Malaysian’s income to start a business. Now, just five years later, it takes only 6 days, 4 procedures, and about 16.4 percent to get your business off the ground. Online filing of registration documents started in 2009 with more and more procedures done online each year. As of this year, companies can register various business and tax documents with the government’s “SSM e-lodgement” web service 24 hours a day.

However, as is the case with China, the difficulty of dealing with construction permits in Malaysia – where a process like acquiring building plan approvals can take up to 90 days – contributed to keep Malaysia behind other Asian countries including Singapore, Hong Kong (2nd) and South Korea (8th).

Another major deterrent for potential investors in Malaysia is the weak enforcement of patents. Without a special court dedicated to dealing with patent infringements, one cannot be certain that innovations will be protected.

Labor

Employers in Malaysia are often frustrated by issues relating to Malaysia’s labor pool and the government’s unpredictable labor and immigration policies. The country has long been plagued with an acute shortage of skilled, local labor, as the labor force only numbers 11.63 million, supplemented with a foreign labor pool of 2 million legal workers and an estimated 800,000 illegal immigrants.

Aggregate numbers on the legal work force in Malaysia are slightly worrying, as their productivity growth is low (3.3 percent) compared to that of China’s (8.7 percent), which is the highest globally and has risen steadily. However, Malaysia’s advantage over China might be its low turnover (5 percent) and wage inflation (5.5 percent). With China’s highly mobile workforce, some enterprises in concentrated industrial zones in China’s manufacturing hubs complain of extremely high turnover, such that competitors are merely swapping workers and raising salaries. Official estimates show average wage increases of 13 percent per year since 2005. Enterprises in Malaysia can expect to retain their employees longer with more stable wage increases.

In addition to this sustained labor shortage, it’s the state’s fluctuating policies on immigration and labor that have led many companies – local and foreign alike – to relocate their businesses outside of Malaysia. The government has at various times cracked down severely on illegal workers. In 2006, Malaysia saw periodic raids from government task forces attempting to flush out illegal immigrants. One factory alone was found to be employing around 1,500 illegal immigrants. More recently, during the global economic recession in 2009, the government enacted a complete ban on new hires of foreign employees in the manufacturing and services sectors, which was subsequently lifted.

Investors are currently waiting on legislation proposed in June of 2011 to offer amnesty to the existing illegal workers in Malaysia, thereby increasing the legal labor pool. For the state, the dramatic move will raise much-needed tax revenues, improve national security, reduce human trafficking, and most importantly, attract more foreign investment. Naturally, this proposal has faced staunch opposition from Malay nationalists, whose interests lay with the rights of local workers. Nonetheless, until a decision is made official, employers should be cautious in knowingly hiring illegal migrants, as the government reportedly performs approximately 16,000 canings per year, many of which are on illegal migrants working in Malaysia’s manufacturing, agricultural and services sectors. The law also stipulates caning as the maximum punishment for an employer who hires illegal workers, though an offending employer has yet to receive the brutal lashing.

In addition to shortages in low-skill labor, Malaysia’s labor force also suffers from a sustained “brain drain,” as talented and highly-skilled professionals have been lured overseas by seemingly better job opportunities. From March 2008 to August 2009 alone, an exodus of 304,358 Malaysians did little to help the growth of the nation’s economy, as the majority of those who left were professionals.

The newly established Talent Corp Agency under the Prime Minister’s office will create programs and incentives to encourage the country’s nationals engaged in key sectors and professions to return home. The World Bank estimates that approximately 1 million Malaysian nationals are currently working overseas, with 60 percent of those surveyed by the World Bank citing “social injustice” as the primary cause for Malaysia’s brain drain. Many of Malaysia’s most talented and experienced professionals settle in Singapore instead for its stable and financially promising work environment.

It remains to be seen how the government will balance the need to build a highly-skilled labor force when higher education levels remain relatively low compared to the former East Asian Tigers, such as Korea, Taiwan and China.

Free trade zones and free trade agreements

There are currently a number of free industrial zones (FIZs) and free commercial zones (FCZs) in Malaysia that facilitate manufacturing and trade activities. Imports coming through these zones are duty free and face limited customs procedures.

In order to make use of the ASEAN free trade area’s Common External Preferential Tariff rates, there is a procurement requirement that 40 percent of a product be sourced from ASEAN member states. Manufacturing and storage activities in these FIZs and FCZs can often be difficult, as approvals from the zone’s administrators are required for different activities. Operating factories and warehouses outside these zones gives a greater range of freedom.

Malaysia is a member of the ASEAN Free Trade Area, and has seen significant growth in trade with AFTA member states, which include Indonesia, the Philippines, Singapore, Thailand, Brunei Darussalam, Cambodia, Laos, Myanmar, and Vietnam.

Through ASEAN, Malaysia has also signed multilateral trade agreements with a number of trade partners such as China, India, Korea, Japan, Australia, and New Zealand. A few promising FTAs with Chile (2010) and the European Union (under negotiation) bode well for the country’s hopes to improve its trade surplus and find comparative advantage in high value-added sectors.

Transportation

Malaysia’s ports are integral to its economy, as 90 percent of the country’s international trade is by sea. The country operates seven major ports connecting Malaysia to various shipping routes. However, the International Maritime Bureau reports that shipping vessels are at high risk of piracy and armed robbery in the territorial and offshore waters of the South China Sea and Strait of Malacca. Though incidents in the past have resulted in the deaths of crew members, naval patrols have been stepped up in the region since 2005 and 2010 saw no reports of incidents of robbery.

Real estate

Investors in the region with plans to purchase residential property will be pleased to know that Malaysia’s regulations on foreign property ownership are extremely liberal. In fact, there are no federal restrictions on residential purchases of property over RM500,000 (approximately US$160,000), and previous requirements for approval from the government’s Foreign Investment Committee have been removed. Nonetheless, individual state governments may impede the process with various formalities.

The Malaysian government has started a program to induce foreigners to relocate to the country with the “Malaysia, My Second Home” program, which offers 10 year visas with property purchases above RM400,000 (approximately US$128,000). Other privileges under the program, like duty-free car purchases, sweeten the deal further for those whose investments in the country might keep them there for a long period of time. While prices are on the rise, particularly in Kuala Lumpur, they are nowhere near the prices one can invariably expect to find in nearby Hong Kong, Singapore, and Shanghai.

Conclusion

Thus it seems that Malaysia’s lofty goal to become a high-income nation by 2020 bodes very well for foreign investors in the region. Despite losing competitiveness – particularly in low-wage manufacturing – to neighboring countries, the government’s New Economic Plan and Economic Transformation Plan indicate a much more inviting investment climate in Malaysia than one might have found in the past. As is the case with China, Malaysia’s state-led push into high tech industries and emerging sectors offer investors a wide range of incentives that are sure to improve the profitability, attractiveness, and ease of doing business in Malaysia.

Related Reading

The China Alternative

The China Alternative

Our complete series on other manufacturing destinations in Asia that are now starting to compete with China in terms of labor costs, infrastructure and operational capacity.

China’s Neighbors (Second Edition)

China’s Neighbors (Second Edition)

This unique book is an introductory study of all 14 of China’s neighbor countries: Afghanistan, Bhutan, India, Kazakhstan, Kyrgyzstan, Laos, Myanmar, Mongolia, Nepal, North Korea, Pakistan, Russia, Tajikistan and Vietnam.

Operational Costs of Business in China’s Inland Cities

Operational Costs of Business in China’s Inland Cities

It is widely held that land and labor costs in inland provinces offer quite significant cost savings over major east coast and southern cities. In this issue, we take a quick look at the numbers behind these beliefs.

- Previous Article China’s Net International Investment Position Hit US$2 Trillion in Mid-2011

- Next Article Financial Institutions Eligible for Stamp Duty Exemptions