China Releases 2012 Advance Pricing Arrangements Report

Sept. 12 – China’s State Administration of Taxation (SAT) released the “China Advance Pricing Arrangement Annual Report (2012)” in both English and Chinese on August 13, which introduces China’s advance pricing arrangement (APA) system, implementation procedures, and practice development, as well as covers the statistical data and analysis of APAs negotiated or concluded during 2005 to 2012. Detailed information can be found below.

An APA refers to an arrangement whereby an enterprise applies in advance to negotiate and reach agreement with the tax authorities with respect to the transfer pricing methods and corresponding calculation methods to be applied to the enterprise’s related party transactions for future years in accordance with the “arm’s length principle.”

As transfer pricing arrangements between related parties are becoming more and more complicated in recent years, multinational companies are calling for more certainties in transfer pricing policies and relevant tax obligations. The APAs serve as a powerful tool for enterprises to obtain more legal certainties to their tax obligations as well as for tax authorities to have stable revenue in the future.

The APA may be categorized as unilateral, bilateral or multilateral based on the number of competent tax authorities of the countries (or regions with independent tax jurisdictions) involved in the APA.

According to the Report, Chinese tax authorities have concluded and signed 85 APAs by December 31, 2012, among which, 56 are unilateral and 29 are bilateral. In 2012 alone, China signed 3 unilateral APAs and 9 bilateral APAs.

Advantages

APAs are an effective way to deal with transfer pricing issues and potential transfer pricing disputes through cooperation between tax authorities and enterprises, and have the following advantages:

- Providing clear responsibilities and obligations for tax authorities and enterprises in regards to transfer pricing issues for future years, thereby offering certainties to taxpayers’ operations and relevant tax obligations;

- Reducing tax authorities’ costs related to transfer pricing administration and audit, effectively mitigating the risk of transfer pricing audits, and lowering tax compliance costs for enterprises; and

- Improving the tax compliance services provided by tax authorities, facilitating the balanced development of administration and services, and assuring taxpayers of their relevant rights and benefits.

Besides, bilateral and multilateral APAs are able to offer the following additional advantages:

- Facilitating communication and collaboration among the competent tax authorities of different jurisdictions; and

- Enabling enterprises to avoid transfer pricing adjustments as well as double taxation risks in two or more tax jurisdictions.

Eligibility Requirements

In general, an enterprise meeting all of the following three criteria may apply for an APA:

- The annual amount of related party transactions exceeds RMB40 million. The types of related party transactions include the following:

- Purchase, sale, transfer and use of tangible assets;

- Transfer or use of intangible assets;

- Financing transactions; and

- Provision of services.

- The enterprise has complied with the related party disclosure requirements according to relevant laws.

- The enterprise has prepared, maintained and provided contemporaneous documentation in accordance with relevant requirements.

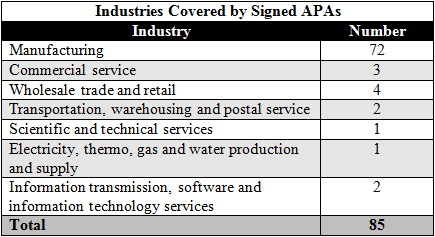

Industries Covered by Signed APAs

According to the chart, APAs from manufacturing industry still takes up the largest portion of signed APAs, reaching 85 percent; while APAs from other industries only account for 15 percent.

Protection of Taxpayers’ Rights

Confidentiality of Taxpayer Information

According to the Report, an enterprise may conduct preparatory talks with the tax authorities on an anonymous basis. Moreover, both tax authorities and the enterprise have the duty to keep confidential all information obtained during the whole process of the APA negotiation.

Taxpayers’ Freedom of Contract

Before signing of the APA, both the tax authorities and the enterprise can suspend or terminate the negotiation. Moreover, if the tax authorities and the enterprise fail to reach an agreement, the non-factual information of the enterprise, including various suggestions, inferences, ideas and conclusions obtained by the tax authorities during discussions and negotiations, shall not be used in future tax investigations of the transactions covered by the proposed APA.

Dezan Shira & Associates is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in emerging Asia.

For further details or to contact the firm, please email china@dezshira.com, visit www.dezshira.com, or download the company brochure.

You can stay up to date with the latest business and investment trends across China by subscribing to Asia Briefing’s complimentary update service featuring news, commentary, guides, and multimedia resources.

Related Reading

![]() Transfer Pricing and Cross-Border Inter-Company Transactions

Transfer Pricing and Cross-Border Inter-Company Transactions

In the issue, we further outline what information documentation should consist of, and what transfer pricing methods can be applied. We also look at payment arrangements among HQ, WFOE, and clients in China.

![]() Transfer Pricing in China (Second Edition)

Transfer Pricing in China (Second Edition)

This book deals with all aspects of transfer pricing in a practical perspective, from designing and implementing a transfer pricing system, to managing China compliance and preparing for an audit.

China Releases 2011 Advance Pricing Arrangements Report

- Previous Article Setting Up a Wholly Foreign-Owned Enterprise (WFOE) in China

- Next Article China Strengthens Personal Information Protection