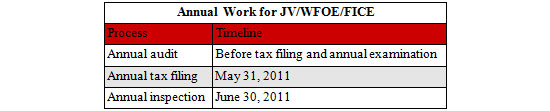

Annual Audit Work for JV/WFOE/FICE

Jan. 7 – Much hard work needs to be done with regards to annual compliance for joint ventures (JVs), wholly foreign owned enterprises (WFOEs) and foreign invested commercial enterprises (FICEs) operating in China.

Below is a list of the annual work required for JV/WFOE/FICE as well as their respective timelines:

Foreign invested enterprises (FIEs) need to be fully aware of the procedures and make sure they are completed on time as all these annual procedures are required according to the law, and there may be monetary punishments if the deficiency is not rectified on time.

FIEs can distribute and repatriate their profits back to their home country after the annual audit and settlement of their relevant tax liabilities. On the other hand, it is also a good opportunity for companies to do an annual health check internally. In this article, we summarize the main steps that may be the key considerations of tax officers and your auditors.

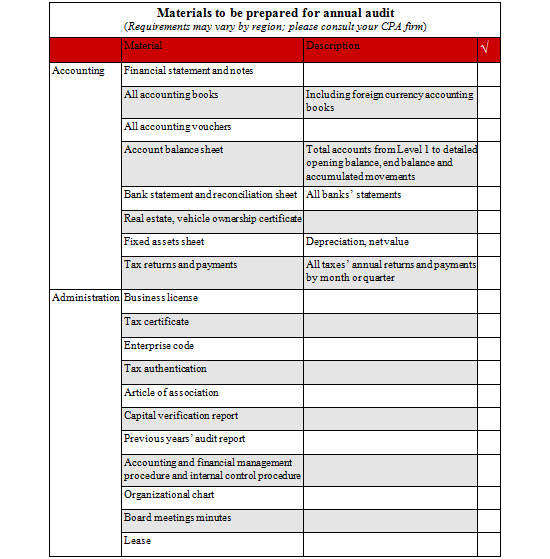

Step 1: Annual audit

Annual audit of FIE statutory accounts must be conducted by a certified public accounting (CPA) firm registered in China under PRC regulations. The annual audit procedures for JV/WFOE/FICE are complicated and these points need to followed carefully.

Bank statement

The balance on your bank book should be the same as stated in the bank statement. If not, please prepare a correct bank reconciliation to verify the differences.

Cash

The balance on your account should be the same to the physical cash in your cash box. The auditors will perform cash count during their field work.

Employment and individual income tax

Employment of staff has to be registered in accordance with the pertinent regulations: valid work permits for expatriate staff. Individual income tax has to be correctly assessed and filed.

Expense reports

Audit fees, salaries, rentals, utilities, and any expenses belonging to the calendar fiscal year should be properly accrued with contracts or agreements as support.

Bad debt

Generally speaking, enterprises could provide reasonable bad debt according to the end balance of their accounts receivables. However, the tax authority has the power to adjust any unapproved provided bad debt allocations and reassign them as subject to income tax.

Reserve funds

Prior to the annual audit, and the subsequent settlement of taxes with the tax bureau, there are items that need to be calculated and presented in the accounts as mandatory fund dispersals. For WFOEs, not less than 10 percent of the after-tax profit should be appropriated to the general reserve fund. By law, WFOEs need to specify the amount for the reserve fund in its articles of association. This must not be less than 10 percent of after-tax profits, and must be contributed to until a ceiling is reached, being the equivalent of 50 percent of the total registered capital in the company. Once this amount is achieved, no further amounts need to be contributed to the reserve fund. Appropriations to other funds should be made in accordance with the articles of association and a board resolution.

Special attention to inventories

Inventory comprises raw materials, components, and finished products. Many companies do not adequately control inventory utilization and disposal of inventory. Common problems include discrepancies of bills of lading and goods received, improper storage of raw materials and safeguarding inventory and the illegitimate disposal of scrap materials and containers.

The process that ties inventory into the financial controls of a company is working-capital management, one of the key components of return on invested capital. For both trading and manufacturing companies, inventories must form a significant proportion of total assets. Auditors will therefore pay close attention to the existence and valuation of such stocks. The inventories valuation can be clearly identified from the purchase invoices or cost calculation sheet. But auditors will also take care to confirm the existence of the inventory and how stocktaking is carried out.

The following steps should be followed:

- Observe whether the stocks are neatly kept, whether large items are properly piled and marked

- Check that counting is systematic to ensure everything is counted and counted just once

- Pay attention to high value items

- Investigate whether discrepancies arise between the physical count and stock records

- Note any items that appear to be damaged, obsolete or slow moving

Internal audits and business reviews are recommended in order to improve company performance (primarily through process improvement) and, in China especially, establish a control system to reduce the risk of irregularities. They provide an additional level of analysis to complement financial statements and often raise serious issues that management may not be aware of, whereas statutory audits tend to be centered on financial figures.

Fixed assets

Purchase of the fixed asset should be recorded in the fixed assets account and annual depreciation should be calculated and allocated to expenses. All construction in progress items should be transferred into fixed assets when they are put into use with any interest expenses, and the disposal gain or loss should also be recorded and approved by the tax authority.

- Fixed asset definition: Fixed asset includes houses, buildings and structures, machinery, mechanical apparatus, means of transport and other such equipment, appliances and tools related to production and business operations with a usage period of 12 months or more.

- Residual value: There is more flexibility on residual value as it can be determined based on the nature of the assets and conditions.

- Depreciation years: Transportation facilities except aircraft, trains and vessels: four years; electronic equipment: three years.

- Accelerated depreciation: If assets need to be updated frequently, the depreciation period can be shorter (limited to 60 percent of the statutory minimum depreciation period).

Stamp duty

Although not a material issue with much cost, FIEs should not forget to pay stamp duty on all books, records and applicable contracts. Fines for non-compliance outweigh the dutiable value.

Step 2: Annual tax filing

All FIEs also need to submit to both the national tax bureau and local tax bureau the Annual Taxation Consolidation Reporting Package authorized by a CPA firm by the end of May each year. In this reporting package, a CPA firm shall verify all the taxes including VAT, business tax, consumption tax, CIT, and other taxes on the basis of the audit result.

The CIT is obviously the most important issue to be disclosed in this report. The related taxable elements, and in particular items involved in CIT such as income, cost and expenses, are specified in detail, while the auditing firm shall make the CIT reconciliation between financial profit and taxable profit in accordance with PRC CIT regulations.

If the audited taxes are different from the taxes paid, the FIEs shall discuss the variation with the tax bureau. For example, should the audited tax figure be lower than the figure paid, the FIE will need to apply for a tax rebate or tax reduction for the fiscal year in question. Accordingly, should the audited tax figure be higher than the paid CIT, once the FIE submits the report, it would have to pay the balance due to the tax bureau. Your auditors should handle such rebate issues.

Although China’s regulations can be burdensome, the key is to be organized, on time and ensure proper supporting records. The regulations are continually changing and overall it should become easier for foreign firms going forward.

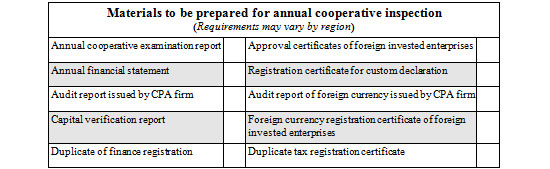

Step 3: Annual cooperative inspection

According to the “Notice of the Implementation Plan for the Joint Annual Examination on Foreign Investment Enterprises” promulgated by the Ministry of Foreign Trade and Economic Cooperation on December 10, 1998 the annual inspection is conducted across the board to ensure that all FIEs should carry out the business in compliance with the legal requirements. The FIEs shall submit to the governing administrative body a signed “Joint Annual Examination Report” and other prescribed financial information including the annual examination report, the audited financial statements and other materials, all signed and stamped by the end of June.

Every company needs to apply for and obtain the annual cooperative examination documents from the same office of the Administration for Industry and Commerce from which they have obtained their original business license. They must also download the annual cooperative examination report form from the relevant provincial or municipal AIC web site. Companies must also select one of two options to apply for annual examination—they can apply either through the internet or through hard copy printed forms.

Materials need to be submitted to seven different government departments: the local office of the Ministry of Commerce, the Finance Bureau, the Administration of Industry and Commerce, the State Administration of Taxation, Customs, the State Administration of Foreign Exchange and the Statistics Bureau.

For professional advice, information and assistance with these filings, please contact Dezan Shira & Associates‘ National Tax and Audit Partner Sabrina Zhang at tax@dezshira.com. You can also download the Dezan Shira & Associates brochure by clicking here.

Parts of this article were taken from the January/February issue of China Briefing Magazine.

Related Reading

Annual Compliance and Audit for Expatriates and Foreign Investors in China

Annual Compliance and Audit for Expatriates and Foreign Investors in China

In this issue of China Briefing, we highlight the annual audit procedures all foreign invested enterprises in China must go through. Specific instructions are given for the audit requirements of representative offices, foreign invested commercial enterprises and wholly foreign owned enterprises.

The China Tax Guide (2010, fourth edition)

The China Tax Guide (2010, fourth edition)

A comprehensive overview of all the taxes foreign investors are likely to encounter when establishing or operating a business in China. (PDF priced at US$40)

- Previous Article China’s NDRC Introduces New Anti-Monopoly Regulations

- Next Article Jiangsu Province to Raise Minimum Wage Standards