China-ASEAN Wage Comparisons and the 70 Percent Production Capacity Benchmark

Op-Ed Commentary: Chris Devonshire-Ellis

As wage increases in China continue to rise – along with the comparatively high national welfare costs – increasing comment is being made as to the legitimacy of the “China Plus One” scenario. Coined some years ago, this theory – in reality, more of a shrewd observation – suggests that future manufacturing capacity will be placed both in China and externally in another location by the same manufacturer.

In fact, this has been going on for years, most notably between China and Vietnam. The recent anti-Chinese riots there have even prompted Hong Kong Shippers’ Council chairman Willy Lin Sun-mo to state that Hong Kong manufacturers based in the Pearl River Delta are running out of alternative, low-cost factory locations with ample labour following recent instability in their two preferred destinations, Vietnam and Thailand. I wrote about the Vietnam and Thai issues – along with a risk analysis for doing business in the rest of Asia – and China, earlier this week here, in this article “Anti-China Vietnam Riots a Passing Phase,” and Willy Lin’s comments can also be construed as a mild political point to Beijing that placing oil rigs in disputed waters hurts Hong Kong manufacturers.

But beyond the recent China-Vietnam clashes, what is the real deal behind the China Plus One issue? Why haven’t thousands of China-based factories closed in face of increasing costs? Where is the economic point at which China wages become non-competitive? And is China’s superior infrastructure the reason why manufacturing will stay in China? These are all important strategic questions for both the China based manufacturer, and the foreign investor to be asking. I will deal with these issues as follows:

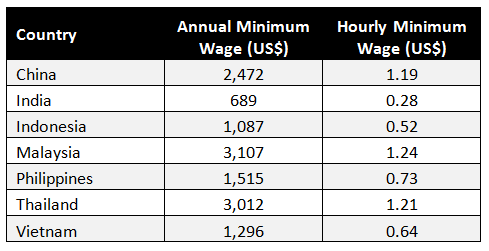

How High in Comparison to the Rest of Asia are China’s Wages?

This is not such a simple question to answer. Firstly because China is a large country with a considerable variables in costs of labour on a national basis. Secondly because the cost of employing staff in China usually involves an additional expense in mandatory social welfare contributions – as is also the case in other countries. But to get a handle on this, we can look at indicators – and in this case, compare the average minimum wage in China as against the other primary manufacturing destinations in Asia. I have taken the main ASEAN manufacturing nations as well as India to compare.

Note that this figure is average. That means that it combines lower minimum wage levels in China with more expensive minimum wage levels – which tend to be precisely where manufacturing labour is required. The average China figure then is actually a bit lower than it would be should we just take minimum wages around the manufacturing hubs of Guangdong, Zhejiang and Jiangsu.

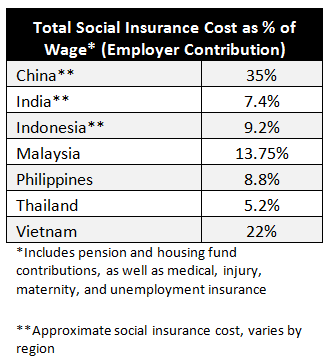

In this comparison, China looks competitive when compared with Thailand and Malaysia. However, the minimum wage comparison is only part of the story. What then kicks in, are mandatory social welfare contributions. These need to be paid by the employer on top of the salary, and are calculated on a percentage basis against salary. There is some regional variation here, but not so much as to make huge differences to the mean average.

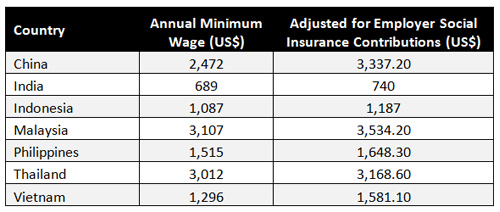

China has relatively high social welfare compared to the rest of Asia. This means that when trying to get a handle on labour cost comparisons, it is important to take the wage level, and adjust it to take into account the additional welfare costs in each country. An adjusted chart taking both into account tells a more accurate story:

China has relatively high social welfare compared to the rest of Asia. This means that when trying to get a handle on labour cost comparisons, it is important to take the wage level, and adjust it to take into account the additional welfare costs in each country. An adjusted chart taking both into account tells a more accurate story:

It should also be noted that in China’s rush to wean the country from being an export-driven economy and onto a consumer based economy, it is State policy to place more money in the hands of Chinese nationals. This means that China is the only country among those shown that has a specific agenda of raising workers salary levels on an annual basis. There are some variables concerning this, but over the past five years these have averaged 15 percent, per annum. And any salary increase also impacts upon the welfare costs. These are useful figures that can be utilised to chart future costs in Chinese salaries looking forward.

It should also be noted that in China’s rush to wean the country from being an export-driven economy and onto a consumer based economy, it is State policy to place more money in the hands of Chinese nationals. This means that China is the only country among those shown that has a specific agenda of raising workers salary levels on an annual basis. There are some variables concerning this, but over the past five years these have averaged 15 percent, per annum. And any salary increase also impacts upon the welfare costs. These are useful figures that can be utilised to chart future costs in Chinese salaries looking forward.

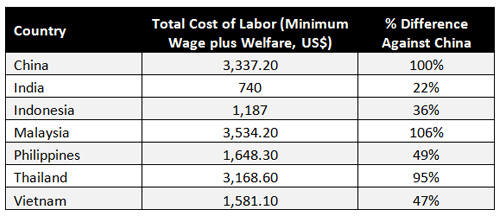

To make it easier to break down, we can compare regional wages, including the added social welfare component, against China as follows:

Why Aren’t Thousands of China-Based Factories Closing?

Why Aren’t Thousands of China-Based Factories Closing?

In fact, they have been. The Hong Kong Federation of Industries warned back in 2011 that some 16,000 Hong Kong owned factories were at risk of closure. Of those, it is estimated about 30 percent actually shuttered their doors. The figures for Taiwanese owned factories are similar. Many slipped away to Vietnam or elsewhere. This movement has largely gone unreported in international media as it has not tended to involve Western investors to the same degree. However, what has been happening is that the business model of many Western-invested factories in China has changed. Instead of being limited to purely export-driven manufacturing, the regulatory environment for foreign invested manufacturers changed a decade ago to permit local production to be sold onto the domestic China market. That was a game changer, and such factories are now concentrating on servicing the China demand. Many are also engaged in improving their China supply chain and distribution networks. So the answer is, cheap Hong Kong/Taiwanese labour-intensive factories aside, manufacturing investment in China has evolved to service increasing China demand. Those factories are staying put.

At What Point Does Manufacturing in China Become Uncompetitive?

This question is actually industry specific. Many manufacturers in China are doing very well, others not. We wrote about the winners and losers in different types of industry in China recently in this article, “South China’s Balancing Act Between Rising Wages and Keeping Investors Happy.”

But essentially, depending upon industry, the nature of how some China based businesses began to become uncompetitive can be traced back to January 1st, 2010. This is when the China-ASEAN Free Trade Agreement came into effect. What this agreement broadly did was to reduce the import/export duties on 90 percent of all products traded between ASEAN nations and China. This impacted specifically on the more advanced manufacturing nations of Indonesia, Malaysia, Philippines, Thailand and Vietnam. Initially, Chinese manufacturers had a field day as they suddenly found these markets very close to home were completely open, and cheap, labour intensive factories – many owned by the Hong Kong and Taiwanese investors I mentioned earlier – flooded into these countries.

But what has gradually been happening since then is the consistent rise in Chinese labour costs. This has meant that countries such as Vietnam are now highly competitive when measured against China. But again, the issue is mainly industry specific, and many factory operations are still highly profitable and likely to remain so. China is moving up the value chain, and these industries are doing well – for the time being. Labour intensive industries or those with thin profit margins for error are however at high risk. For further details and downloads of the China-ASEAN Free Trade Agreement, please see our sister ASEAN Briefing website here.

Why China?

The big deal about China is its transition from export manufacturing to a consumer-driven society. Briefly put, the impact of this means that China’s middle class consumer population is expected to rise from approximately 250 million today to 600 million by 2020. That means an additional 350 million middle class consumers will emerge across China in the next seven years. The question then becomes this. Where is the manufacturing capacity going to be to service those consumers? The answer is Asia. The existing China operations will evolve, and continue to provide some manufacturing facilities. But they are also changing to become more logistics and planning based, even to the extent of importing, warehousing and distributing products manufactured in a related factory elsewhere in Asia. The China facility is still needed, but its function is changing. And the big win is in being able to sell to a Chinese consumer market more than doubling its existing size. The real question then is whether the additional manufacturing capacity required to service this market should be added to the existing China facility or based in elsewhere in Asia. Increasingly, the cost dynamics are in favour of it being placed elsewhere in Asia. Hence the “China Plus One” issue.

The ASEAN-China Infrastructure Gap: 70 Percent Productivity is the Rule of Thumb.

Also kicking in to the entire picture is the infrastructure issue. China’s infrastructure, and especially in South China and the Zhejiang / Jiangsu regions is generally excellent, less so once factories start to move inland. China actually has a serious shortage of central and inland warehousing, distribution and logistics facilities inland. However, there is still an infrastructure gap between Shanghai for example and Ho Chi Minh City; Guangzhou and Manila and any other permutations. Operating a factory in many ASEAN countries means having to deal with an infrastructure not as well developed as on China’s eastern seaboard, and this eats into productivity levels. However, even this can be measured. As a general rule of thumb, when asking Dezan Shira & Associates clients in Vietnam, Indonesia, India, Philippines and elsewhere, it often makes economic sense to place manufacturing capacity into a secondary location if the facility can get production levels up to 70 percent of the equivalent operation achievable in China. There is another caveat to this too. China wages are only going to keep increasing. And additional investment means the infrastructure gap is going to keep decreasing. In ten years’ time, production managers are going to be far less likely to complain about infrastructure problems elsewhere in Asia when held up against China.

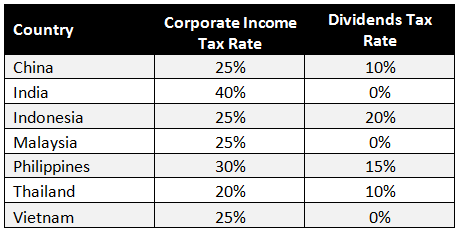

Additional Profitability Issues

Another issue to bring into the equation is the rate of profits tax. This is a moving target in Asia, although the situation in China is quite consistent. Foreign investors who are taking the bulk of their profits in China may also wish to examine the regional alternatives. Dividends taxes apply to foreign investors who wish to repatriate their profits back to their parent company.

Of these, it should be noted that several countries are set to reduce taxes below that listed above. India, for example, is expected to finally get its tax reform bill through Parliament, and this is likely to see a reduction in CIT from 40 percent down to 30 percent. The Philippines too has been discussing the same, with reductions to 25 percent. Vietnam has already said it will reduce CIT by 2016 also to 20 percent. These will make the economic debate concerning the placing of additional manufacturing capacity into Asia much easier to acknowledge.

Withholding Taxes

It should be noted that use of applicable Double Tax Treaties on certain charges such as services rendered by the parent company as a strategy can decrease the amount of withholding tax payable. This is commonly used to legitimately decrease the amount of annual profits a company declares. Withholding tax rates on corporate charges such as royalties are usually permissible at a 10 percent rate, lower than the Profits tax rate. DTA typically reduce withholding taxes by 50 percent. However all of the countries mentioned in our comparisons already have significant DTAs in place, and there is not much benefit to be gained over one or the other in this regard when compared with China: nearly all have similar mechanisms in place. For an overview of how Double Tax Treaties can impact upon your China operations, please see our article on the subject here.

Investment Incentives & Tax Breaks

China essentially standardized its tax position a decade ago and apart from a few examples, did away with many of the 15 percent profits tax rates and five year tax breaks that marked much of the 1980’s and 1990’s that encouraged foreign investment to pour into the country. Now restricted to specific key underdeveloped geographical regions and highly specific sought after technologies, China isn’t so much of a bargain hunting ground when it comes to such deals nowadays. But that doesn’t mean the rest of Asia is the same, and far from it. All ASEAN nations as well as India possess free trade, special economic and export processing zones, many of them offering the same sort of tax breaks and low tax rates that China did a decade ago. The list is too long to reproduce in this article, although we did cover the subject in this issue of Asia Briefing Magazine “An Introduction to Development Zones Across Asia.” When it comes to ASEAN and India, there are many tax breaks and investment incentives around just as there used to be in China – so do your research and shop around.

Winners & Losers

For China, this is all gain. However, existing China-based manufacturing facilities will need to evolve a different set of skills, most notably in developing supply chain, distribution, warehousing and marketing skills into new regional China markets. The China facility will become not just a manufacturer, but also a facilitator, and this will mean a change of focus in addition to scope of business to take advantage of the new China consumer dynamic.

Winners in Asia as we stand today include Vietnam, who are set to lower their corporate income tax rate to 20 percent (against China’s 25 percent) by 2016 specifically to better compete. India too, with a new government in place, has both the benefit of an inexpensive, huge and growing labour pool, and an improving infrastructure. China has itself recognised the growing importance of India as a manufacturing hub to service the China market – the Chinese government have offered to foot 30 percent of India’s US$1 trillion infrastructure development requirements to allow this to happen. And as sage China watchers well note, it is always wise to follow China’s State policy. Plus India also has a massive consumer market – one reason Ford have placed their entire non-U.S. auto manufacturing capacity into Gujarat.

In terms of India’s relationship with ASEAN – it should be noted that it too has a Free Trade Agreement with ASEAN – meaning that 90 percent of all trade and services between the two are now duty free. This provides an added incentive to establish an ASEAN manufacturing facility to service not just China, but ASEAN and the Indian markets in one fell swoop.

The Philippines and Indonesia are also likely to do well. Despite the recent row over maritime borders, these have been kept to diplomatic levels and bilateral trade has been increasing. A booming Manila gambling scene, away from the eyes of the Chinese secret service and spectacular beach resorts are fuelling a Chinese tourism boom, while wide usage of English language and again, an improving infrastructure is seeing the Philippines become an Asian investment sweet spot.

Indonesia too, although the Jakarta traffic situation remains dire, is also offering large numbers of competent labour, an increasingly educated workforce and a sizable Chinese diaspora who have seen first hand the management techniques employed in mainland China and are setting up similar operations in Java. There is a lot of truth to the notion that the Indonesian city of Surabaya is set to become that countries equivalent of Guangzhou – yet how many foreign investors have heard of it?

Malaysia also offers a number of joint venture business parks, run along the proven Chinese model, and these too offer tax incentives and breaks no longer available in mainland China. The country is politically stable, and provides excellent infrastructure – as anyone who has taken the highway from the Airport to downtown Kuala Lumpur will testify.

On the cautious side, Thailand looks set for a period of military rule, which until the country is considered politically stable enough, is likely to put off some foreign investors. Yet when viewed as a longer term play, it has excellent dynamics and is strategically placed in the centre of ASEAN. This makes the country an ideal base from which to reach out to ASEAN’s own consumer market, as well manufacture to service China and beyond. This is the reason Volkswagen have decided to base their Asian production facility in Thailand – reaching out to the ASEAN market, while their existing China operations will continue to focus on the growing Chinese domestic market.

Other commentators may ask why I haven’t mentioned Cambodia, Laos or Myanmar. While they may sound adventurous, the reality is that none of these countries as yet have any significant infrastructure in place. Salary levels may well be low, but generally speaking the infrastructure gap is too wide at present to make them viable except for perhaps smaller manufacturers willing to spend a great deal of time, effort, education and investment into these countries. Neither are their international tax obligations especially advanced – Cambodia, for example, has signed no double tax treaties at all, with anyone.

For the next decade, these countries will remain the preserve of big ticket infrastructure developers and will remain a step too far for many, although over time this will change – just as countries like Vietnam and Thailand start to become expensive. But that is some way off yet.

Conclusion

The “China Plus One” issue is not just a theory, it has already arrived and is being put into practice. Foxconn, for example, are in the process of relocating their entire assembly operations for Apple products to Indonesia.

Much of South China’s shoe-wear and fabrics industry has already set up shop in Vietnam and Bangladesh, the latter to such an extent that Bangladesh is now the world’s second largest producer of textiles – after China.

Operational and economic trends as we have seen dictate that Chinese labour is and will continue to become more expensive, while the Asian infrastructure gap is narrowing. Yet China’s own domestic consumer market is growing, as are those in the rest of Asia – ASEAN and India included. The locating of a secondary production facility elsewhere in Asia is not just a theory, it is an economic necessity. Foreign investors wishing to sell product onto the China market must now start to compare the economic costs of doing that from China with that of placing that capacity elsewhere into Asia, and using the China-ASEAN DTA to avoid import duties.

Chris Devonshire-Ellis is the Founding Partner of Dezan Shira & Associates – a specialist foreign direct investment practice providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in emerging Asia. Since its establishment in 1992, the firm has grown into one of Asia’s most versatile full-service consultancies with operational offices across China, Hong Kong, India, Singapore and Vietnam, in addition to alliances in Indonesia, Malaysia, Philippines and Thailand, as well as liaison offices in Italy, Germany and the United States. For further information, please email asia@dezshira.com or visit www.dezshira.com.

Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

Related Reading

The Gateway to ASEAN: Singapore Holding Companies

The Gateway to ASEAN: Singapore Holding Companies

In this issue of Asia Briefing Magazine, we highlight and explore Singapore’s position as a holding company location for outbound investment, most notably for companies seeking to enter ASEAN and other emerging markets in Asia. We explore the numerous FTAs, DTAs and tax incentive programs that make Singapore the preeminent destination for holding companies in Southeast Asia, in addition to the requirements and procedures foreign investors must follow to establish and incorporate a holding company.

An Introduction to Tax Treaties Throughout Asia

An Introduction to Tax Treaties Throughout Asia

In this issue of Asia Briefing Magazine, we take a look at the various types of trade and tax treaties that exist between Asian nations. These include bilateral investment treaties, double tax treaties and free trade agreements – all of which directly affect businesses operating in Asia.

An Introduction to Development Zones Across Asia

An Introduction to Development Zones Across Asia

In this issue of Asia Briefing Magazine, we break down the various types of development zones available in China, India and Vietnam specifically, as well as their key characteristics and leading advantages. We then go on to provide a snapshot of the latest development zones across the rest of Asia. With several hundred development zones operating in the region, it is impossible to cover them all in the pages of just one publication. However, we hope that this issue will provide the basic fundamentals to understanding one of the most important business tools available to international businesses operating in Asia.

Expanding Your China Business to India and Vietnam

Expanding Your China Business to India and Vietnam

In this issue of Asia Briefing Magazine, we discuss why China is no longer the only solution for export-driven businesses, and how the evolution of trade in Asia is determining that locations such as Vietnam and India represent competitive alternatives. With that in mind, we examine the common purposes as well as the pros and cons of the various market entry vehicles available for foreign investors interested in Vietnam and India. We also examine the advantages of using Hong Kong and Singapore as corporate bases to reach out to Asia’s emerging markets. Finally, we comment on how the proposed Trans-Pacific Partnership will affect both China-based and Vietnam-based manufacturers.

China Outbound: Shifting Demographics and Manufacturing Trends in Asia

- Previous Article The East is Green: The Future of China’s Environmental Regime (Part 1)

- Next Article China Puts the Brakes on Additional Free Trade Zones