China Expat Tax Filing and Declarations for 2013 Income

Determining IIT Liability for Foreign Employees in China

SHANGHAI – Individuals residing in China are subject to the country’s individual income tax (IIT), which is normally withheld from wages by employers and paid to the tax authorities on a monthly basis.

The IIT liability of a foreign individual in China depends on the individual’s duration of stay in China and his/her source of income. The IIT Law of China stipulates that a resident or non-resident individual residing in China for one year or more is subject to Chinese IIT for both China sourced income and non-China sourced income. A non-resident individual residing in China for less than one year is only subject to Chinese IIT for China sourced income. However, to fully understand these rules and how they are implemented, we need to examine them in greater detail.

Duration of Stay in China

It is notable that “one year” in the context of the IIT law refers to one tax year. The tax year of China is the same as the calendar year, i.e. January 1 to December 31, and “residing in China for one year” is defined as residing in China for 365 days in a tax year. However, a non-resident who has taken temporary absences from China for less than 30 days continuously or 90 days total in a tax year will still be considered having resided in China for 365 days of the tax year. Additionally, if there is a double taxation agreement (DTA) between a foreign country and China, the 90-days may be extended to 183 days, depending on the relevant DTAs.

It is also worth mentioning that the day on which the individual enters or leaves China is considered a full day in determining his/her duration of stay in China.

Source of Income

With regard to the source of income, China’s IIT regulation defines China-sourced income as income received by the individual while working in China, regardless of whether the income is paid by an employer domestically or overseas; foreign-sourced income refers to income received by an individual for working outside of China, regardless of whether the payment is made by an employer in China or overseas.

RELATED: China Clarifies IIT Rules Regarding Share Capital Increase after Equity Acquisition

In addition, the following income types are deemed as China-sourced income regardless of who makes the payment:

- Income from providing services in China;

- Income from leasing property to a lessee for use in China;

- Income from transferring properties located in China, such as buildings and land-use rights, and transferring other properties in China;

- Income from licensing for use of proprietary rights in China;

- Interest, dividend, and bonus income derived from companies, enterprises, and other organizations or individuals in China.

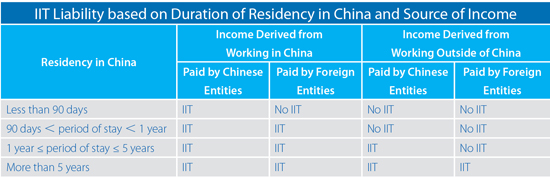

Foreign Individuals Residing in China for Less than 90 Days in a Tax Year (“90-day Rule”)

A non-resident individual who has worked in China continuously or cumulatively for less than 90 days in a tax year is exempted from IIT on income paid by a foreign employer outside of China. This means that the individual is only subject to IIT for income he/she received from Chinese domestic institutions, entities and individuals for work done in China.

Foreign Individuals Residing in China for More than 90 Days but Less than One Year (“One-year Rule”)

An individual who has resided in China for more than 90 days but less than one year during the tax year is subject to IIT on all China-sourced income, which includes income paid by both Chinese and overseas entities for his/her work in China. Income earned while working overseas (i.e. foreign-sourced income) in the tax year is not Chinese IIT taxable.

Foreign Individuals Residing in China for More than One Year Consecutively but Less than Five Years

A foreign individual who has resided in China for more than one year but less than five years must pay IIT for income received from both Chinese and foreign employers for work conducted in China (China-sourced income), and also for income paid by Chinese employers during any temporary absences from the country.

Under these circumstances, income obtained from foreign employers for work done during a temporary absence is still not taxable in China.

Foreign Individuals Residing in China for More than Five Years Consecutively

A foreign individual who has resided in China for more than five years continuously may face IIT liabilities identical to those of a resident individual of China, depending on the duration of his/her residency in China starting from the sixth year. It is notable here that “five years” still refers to five tax years, i.e. January 1 to December 31.

RELATED: IIT Calculation for Hong Kong and Macau Residents’ Mainland-Derived Income

If a foreign individual resides in China for one year in the sixth or any following single year, he/she would be considered a resident individual under IIT and is taxable on income received globally for that specific tax year; if the individual resides in China for less than one year in the sixth or any following single year, he/she is subject to IIT on only China-sourced income, and the One-year Rule applies.

The five-year threshold will be reset if the individual resides in China for less than 90 days in any single tax year starting from the sixth year, in which case the “90-day Rule” will apply for that tax year.

Understanding the “five-year rule” is especially important for foreign companies with expats working in China for the long-term as their IIT burden may be significantly reduced if their stay in China is managed properly.

To better clarify IIT liabilities, a demonstration of the above rules is given in the table below:

Note: The 90-day and one-year rules do not apply to foreign individuals hired as directors or other senior executives of enterprises located in China. Their full income as senior executives is subject to Chinese IIT starting from the initial tax year of employment and lasting until the tax year of the end of employment, regardless of how long they have actually resided in China. The IIT liabilities of their foreign-sourced income, however, are still determined by the rules we discussed above.

Individual income tax rates and calculation methods, as well as an overview of the declaration process for expatriates in China are covered here.

Dezan Shira & Associates is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in emerging Asia. Since its establishment in 1992, the firm has grown into one of Asia’s most versatile full-service consultancies with operational offices across China, Hong Kong, India, Singapore and Vietnam in addition to alliances in Indonesia, Malaysia, Philippines and Thailand as well as liaison offices in Italy and the United States.

For further details or to contact the firm, please email china@dezshira.com, visit www.dezshira.com, or download our brochure.

You can stay up to date with the latest business and investment trends across Asia by subscribing to Asia Briefing’s complimentary update service featuring news, commentary, guides, and multimedia resources.

Related Reading

Payroll Processing Across Asia

Payroll Processing Across Asia

In this edition of Asia Briefing Magazine, we provide a country-by-country introduction to how payroll and social insurance systems work in China, Hong Kong, Vietnam, India and Singapore. We also compare three distinct models companies use to manage their payroll across various countries with external vendors, and explain the differences among three main models: country-by-country, managed, and integrated models while highlighting some benefits and drawbacks of each.

Annual Audit and Compliance in China

Annual Audit and Compliance in China

In this issue of China Briefing, we discuss annual compliance requirements for foreign-invested enterprises, including wholly-foreign owned enterprises, joint ventures and foreign-invested commercial enterprises, as well as the less demanding requirements for representative offices. We also highlight the most recent tax and legal changes that will significantly influence the way companies do business in China in 2014.

China to Cancel Preferential IIT Policy for Foreigners

Employers’ Overseas Social Insurance Contributions are IIT Taxable

How to Calculate Your 2013 Expatriate Individual Income Tax in China

- Previous Article Why ASEAN Overtook China’s Foreign Investment Last Year

- Next Article How to Calculate Your 2013 Expatriate Individual Income Tax in China