China FICE vs. Manufacturing WFOE

Op-Ed Commentary: Chris Devonshire-Ellis

May 11 – Foreign-invested commercial enterprises (FICE) are a relatively recent addition to the different types of legal structures available to foreign investors in China, essentially being drafted into law as a reaction to China’s joining the WTO 10 years ago. Prior to this, foreign investors had to use wholly foreign-owned enterprises (WFOEs) or joint ventures in order to trade in China – and even that sector was restricted at the time. The FICE structure enabled foreign investors to establish an entity that would provide both import and export licenses with minimal capitalization for the first time. They were introduced specifically to make it easier for foreign investors to both buy and export China-sourced products without the need for going through an agent, and in accordance with China’s WTO obligations, to allow foreign companies to develop their own sales structures and possess their own import licenses.

WFOEs – although similar legislative deregulation occurred at around the same time in terms of permitting them a more service-oriented role – have always been more suited to actual production and manufacturing. Curious as it may seem now, WFOEs were previously forbidden from comprising both production and service activities, and often two WFOEs had to be set up by one company to facilitate, for example, the manufacturing and then service maintenance of sold equipment. The introduction of FICE and the liberalization of WFOE law enabled foreign investors to gain access to import and export licenses under their own steam and to engage in the service and manufacturing industries with one business license for the first time.

Generally speaking, the type of legal structure required in China is largely dependent upon what it is you want to do, and this is easily determinable by asking just one simple question:

- Do you need to invoice clients or buyers in China in RMB?

Everything after that question is answered becomes a matter of business activities (regulatory) multiplied by financial and tax planning (tax) and knowledge of different areas of China, as these change depending upon location. For example, there are often valuable financial incentives on offer to attract foreign investment slightly more inland than exists for China’s coastal regions. These can involve preferential VAT treatment, lower capitalization costs and even tax holidays (if you want updates on the best locations, incentives and cost comparisons be sure to use a China-based, not overseas-based, consulting firm). After that, a business needs to cater for on-going operational compliance issues (accounting, audit and company secretarial work). The legal aspect of getting a company set up and operational in China is actually only a small component part compared with the overlapping issues.

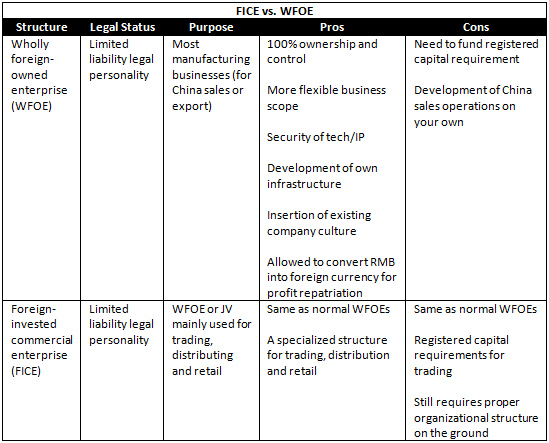

In this article we introduce and compare the manufacturing WFOE and FICE. Please note that FICE can be either in the form of a WFOE or a JV, but that in this article we will focus on FICE in the form of a wholly foreign owned structure.

As a FICE is also a type of WFOE, it is not surprising that both are somewhat similar in terms of legal status, structure, registration requirements and establishment procedures. The main differences between the two lie in their primary function – the manufacturing WFOE is obviously primarily used for manufacturing while FICE is primarily used for trading and distributing goods.

The table below shows the main characteristics defining the WFOE and FICE structures.

It is worth noting that a “cookie-cutter” approach to structuring such entities has recently become increasingly prevalent. However, in the rush to get into the China market, many consultants, investors and other so-called “experts” have been advising, or have been advised, in a poor and simplistic manner. Equally, international businessmen have still shown themselves to be occasionally rather naïve when it comes to dealing with business operations in China. We advise individuals and entities considering setting up in China to follow the following rules:

- Rule #1 –Don’t throw the rulebook away. Whatever made you have a successful business overseas, don’t abandon it just because this is China. Be diligent, and be smart.

- Rule #2 – Setting up a business in China requires China tax and China legal knowledge. Not one or the other, but both. You need to have professional advice in both these disciplines to get the most out of your business – before you start to invest. Setting up a business in China is actually more of a financial administration and tax question than it is a legal one.

- Rule #3 – Cheap advice is dangerous. Everyone is an expert on China these days. Cheap advice is just that – cheap. Do your research. Professional firms are there for a reason – depth of knowledge and understanding of China business and operational quirks and idiosyncrasies. Investing in China requires a great deal of attention to detail. Your manufacturing WFOE or FICE needs customizing to make it as cost-efficient as possible.

Foreign-Invested Commercial Enterprises

As part of its WTO accession process, China ratified regulations that permit foreign companies to establish fully operational WFOE retail and trading companies that can buy and sell in China. These rules became effective from June 1, 2004.

What does the law say?

The Measures for the Administration of Foreign Investment in the Commercial Sector liberalized China’s distribution and retail sector. Foreign companies are allowed to establish:

- Majority joint venture trading companies

- WFOE trading companies

In detail, the new regulations apply to the following five activities:

- Retailing – i.e. selling goods and related services to individual persons from a fixed location, as well as through TV, telephone, mail order, internet, and vending machines

- Wholesaling – i.e. selling goods and related services to companies and customers from the industry, trade or other organizations

- Representative transactions on the basis of provisions (agent, broker)

- Franchising

- Import/export, distribution and retailing by existing manufacturing companies

Note that all geographical restrictions for retailing enterprises have been removed, and foreign investors can establish retail stores anywhere in China. Limitations do, however, apply to some specific products. Namely, if a foreign investor in China has more than 30 retail stores that distribute products such as books, periodicals, processed oils from different brands or suppliers, the foreign investor’s share in the retail enterprise is limited to 49 percent. Retailing enterprises which do not distribute the limited products are not restricted on the number of stores in China.

Set-up requirements

Foreign investors will enjoy national treatment in setting up trading companies with minimum registered capital in accordance with the Company Law of China:

- For wholesale and retail enterprises (single shareholder): RMB100,000

Business duration is limited to 30 years for foreign trading companies set up in the developed coastal areas. Companies established in West China are allowed business duration of 40 years. Foreign companies shall “possess a sound reputation and comply with Chinese law.”

Manufacturing WFOEs

There are several major, inter-related issues to address if you intend to set up a manufacturing WFOE in China. We cover some of the key points below.

Business scope

Having set up a limited company does not necessarily mean you can engage in any kind of business activity, as is the case in some Western countries. WFOEs can only operate within the business scope approved by the authorities. Other activities are subject to further approval. So it is vital to determine what you want to do right from the start.

Registered capital requirements

One of the most common, and most serious, problems with WFOE applications, especially for small businesses, is the issue over registered capital. This is a much misunderstood area. Confusion exists, and many ill-advised investments are made dueto misinterpretation of the local government’s term “minimum registered capital.” It is not supposed to be a ruling on how much you need to invest. Registered capital is the initial investment in the company that is immediately used in its operation – part of the “working capital” if you like. Get this wrong and it is financially painful to change it.

These may vary depending on the industry and the location. It is also absolutely critical that you do not simply put in the minimum because the regulations say you can – you may find the business is under-capitalized if you do so. This is an operational judgment for you, not the bureaucrats.

So how much do you have to pay? Under the Company Law, which came into force on January 1, 2006, absolute minimum capital requirements are:

- For multiple shareholder companies: RMB30,000 (Article 26)

- For single shareholder companies: RMB100,000 (Article 59)

Registered capital can be contributed in cash or in kind, the latter normally being imported equipment or perhaps intellectual property rights (although in kind contributions cannot exceed 70 percent of the registered capital). Note that it can be time-consuming to inject equipment as a registered capital, rather than buying it using the registered capital cash. Locally obtained RMB cannot be injected as registered capital – it must be sent in from the overseas investor.

Operational issues and tax liabilities

Different types of WFOE operations require different kinds of structuring. How to go about it depends on what you want to achieve.

Manufacturing, processing and assembly, 100 percent for export

The Chinese love this type of operation and will reward you with some incentives and tax breaks. If you are sited in a free trade zone or export processing zone, you may not even have any import-export duties to worry about.

Basic tax breaks are against corporate income tax (CIT), which is 25 percent nationally. Certain sectors, such as agriculture and high-tech, can offer some tax deductions. If you export 100 percent of your production, then more incentives may kick in. For more on these issues, take professional advice.

Manufacturing, processing and assembly, part or all domestic sales

The domestic sales aspect fundamentally changes the tax structure of the WFOE, as it is then subject to import duties on any imported components and VAT at 17 percent on sales (import duties will vary depending on product, location and final customer).

Under recent changes, WFOEs can now sell the majority, if not all, of their production domestically, thus tapping into the increasingly attractive local market. It is still wise, however, when structuring your WFOE to include a provision allowing you to sell your product on the domestic market “according to China’s WTO agreements,” thus permitting you to upgrade your domestic sales quota automatically without having to go through a constant process of updating your business license whenever a change occurs. You still get the tax breaks, but won’t qualify for rebates on CIT or other taxes as these only apply to WFOEs exporting 100 percent of production.

Trading via WFOEs

If you are a manufacturing business, you may still import and distribute products not manufactured in China under an amended manufacturing WFOE license – provided the amount does not “in general” exceed 30-50 percent of total revenues, depending on the region. This means that manufacturing WFOEs can still trade as mentioned above, as long as the trading portion remains the minority part of the business. This is worth considering as a structure if your business model requires both, for example if your clients may occasionally require additional spare parts (import and trading service) or other maintenance issues. Note that approval needs to be obtained for this, including tax bureau permission. Your books also need to be accurate, well-organized and will be subject to scrutiny by the tax bureau to ensure you are in compliance.

Summary

As we have determined above, the question of FICE vs. WFOE largely depends upon what you want to do. For buying from China, either a representative office or a FICE may suffice (we covered RO vs FICE earlier in the week here). For selling to China, a FICE would normally be the choice, as it would for both buying and exporting from China, and importing and selling into China. FICE, therefore, are extremely useful entities. WFOEs, on the other hand, can be used in the service industry, but are more commonly deployed when there is a processing, added-value or manufacturing component aspect to your business in China.

Chris Devonshire-Ellis is the founding partner of Dezan Shira & Associates – a boutique professional services firm providing foreign direct investment business advisory, tax, accounting, payroll and due diligence services for multinational clients in China, Hong Kong, India, Singapore and Vietnam. The firm specializes in assisting foreign enterprises establish and operate legal entities in China such as WFOEs and FICE. For advice, please email china@dezshira.com, visit www.dezshira.com, or download the firm’s brochure here.

Related Reading

Trading and Establishing FICE in China

Trading and Establishing FICE in China

In this issue of China Briefing Magazine, we evaluate the suitability of ROs, walk you through the details of FICE (including establishment procedures), discuss franchising in China for foreign companies, and put in a few words about the Chinese consumer from a macroeconomic perspective.

Setting Up Wholly Foreign Owned Enterprises in China (Third Edition)

Setting Up Wholly Foreign Owned Enterprises in China (Third Edition)

This guide provides a practical overview for any business-minded individual to understand the rules, regulations and management issues regarding establishing and running a WFOE in China.

Hong Kong and Singapore Holding Companies

Hong Kong and Singapore Holding Companies

In this issue of China Briefing Magazine, we take a closer look at the benefits of both Hong Kong and Singapore holding companies, how to establish and maintain a company in each of these jurisdictions, and the relevant double tax agreements.

FICE Franchising in China: A Flourishing Business Model

VAT General Taxpayer Status Important for FICE

China WFOEs: It’s Not Standard Law, It’s Getting the Finance and Tax Right

China Incorporations. Let’s Get Real, They’re a Tax, Not Legal, Structure

- Previous Article Regulations Affecting Foreign-Funded International Freight Transportation Agencies in China

- Next Article China’s PBC to Cut Reserve Rate Requirement by 0.5 Percentage Points