China-Italy Double Tax Treaty 2026: Practical Tax Planning Guide for Italian Investors

The new China-Italy Double Tax Treaty has been applicable since January 1, 2026, replacing the 1986 agreement and reducing withholding tax on dividends, interest, and royalties for qualifying Italian investors. The new rates are conditional on shareholding, beneficial ownership, and documentation requirements that must be in place before the first 2026 payment is released.

The new Agreement between China and Italy for the Avoidance of Double Taxation (China-Italy DTA) entered into force on February 19, 2025, and applies from January 1, 2026, ushering in a long-awaited upgrade to the 1986 agreement. For qualifying Italian investors, the treaty offers reduced withholding tax rates on dividends, interest, and royalties but only where shareholding thresholds, beneficial ownership, and documentation requirements are met before the payment is made.

Beyond rate reductions, the revised China-Italy DTA introduces more sophisticated rules. It modernizes the taxation of dividends, interest, and royalties, refines the treatment of capital gains, and incorporates a Principal Purpose Test. For Italian companies engaged in cross-border investment, financing, licensing, or equipment supply, these changes can significantly lower tax exposure, provided treaty eligibility is carefully structured in advance.

This article breaks down the four payment flows where treaty benefits matter most, explains the Chinese-side procedural mechanics, analyzes the Article 23 credit limitation on the Italian side, and assesses the permanent establishment exposure for Italian service providers.

Take Action now to Ensure You Fully Benefit from the New China-Italy DTA

With lower withholding tax rates now available, prepare early to confirm treaty eligibility, reduce compliance risk, and strengthen your cross-border tax position from day one.

- Assess your eligibility for reduced withholding tax rates on dividends, interest, and royalties

- Review shareholding structures and confirm beneficial ownership status

- Prepare supporting documentation in line with Chinese tax authority requirements

- Evaluate permanent establishment risks and Italian-side tax credit limitations

Contact Dezan Shira & Associates at china@dezshira.com to discuss how the new treaty impacts your China-Italy operations and how to implement a compliant, tax-efficient structure.

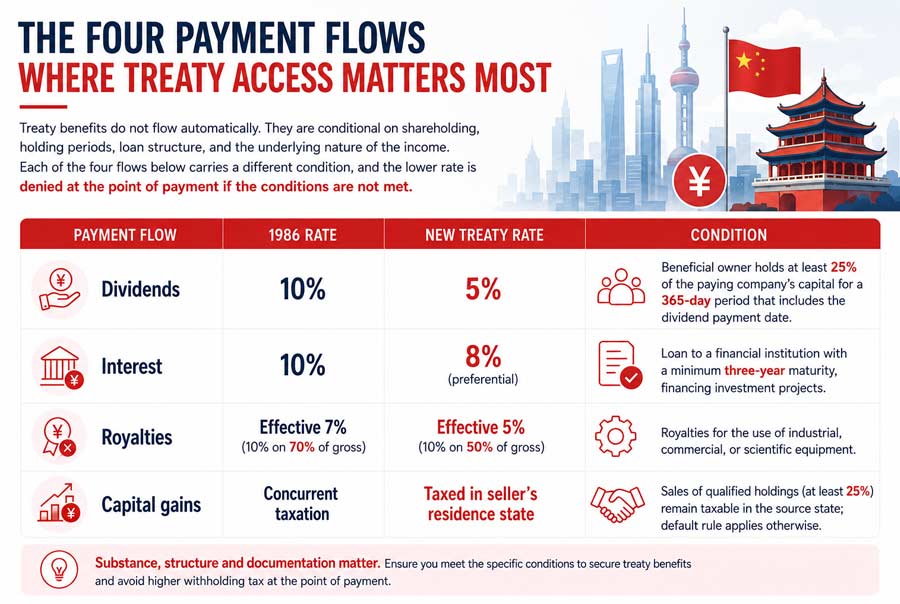

Dividends: A 5 percent rate for qualifying long-term holdings

Under the 1986 treaty, dividends paid by a company in one contracting state to a resident of the other were subject to a uniform withholding tax cap of 10 percent, regardless of the level or duration of shareholding.

The new treaty introduces a more differentiated approach. Where the beneficial owner is a company that has directly and continuously held at least 25 percent of the capital of the dividend-paying company for at least 365 days, including the payment date, the withholding tax rate is reduced to five percent. Dividends that do not meet this threshold remain subject to the 10 percent cap.

The reduced rate delivers tangible savings for long-term equity investors and encourages deeper, more stable strategic participation rather than short-term financial holdings.

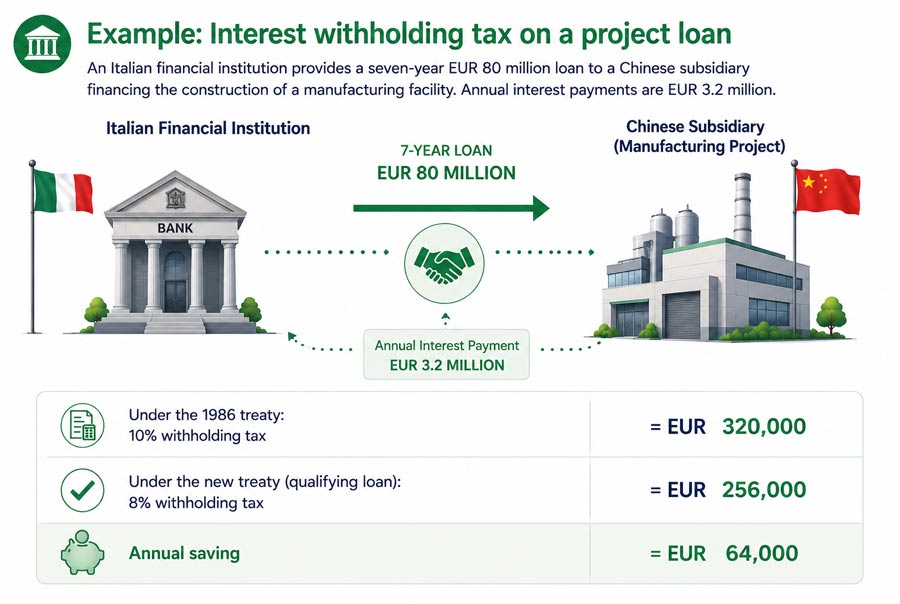

Interest: Preferential treatment for project financing and public lenders

The new treaty replaces the former single-rate approach with a three-tier structure that reflects the lender’s profile, the loan purpose, and its duration.

Interest paid to the government, central bank, or a wholly owned public institution of the other contracting state (or interest on loans guaranteed or insured by such institutions) is fully exempt from withholding tax. Interest paid to a financial institution for loans of three years or longer that are used for investment projects qualifies for a reduced eight percent rate. Other interest payments remain subject to the 10 percent cap.

The structure lowers financing costs for qualifying long-term projects and supports large-scale Sino-Italian cooperation, particularly in infrastructure, manufacturing, and capital-intensive industrial sectors.

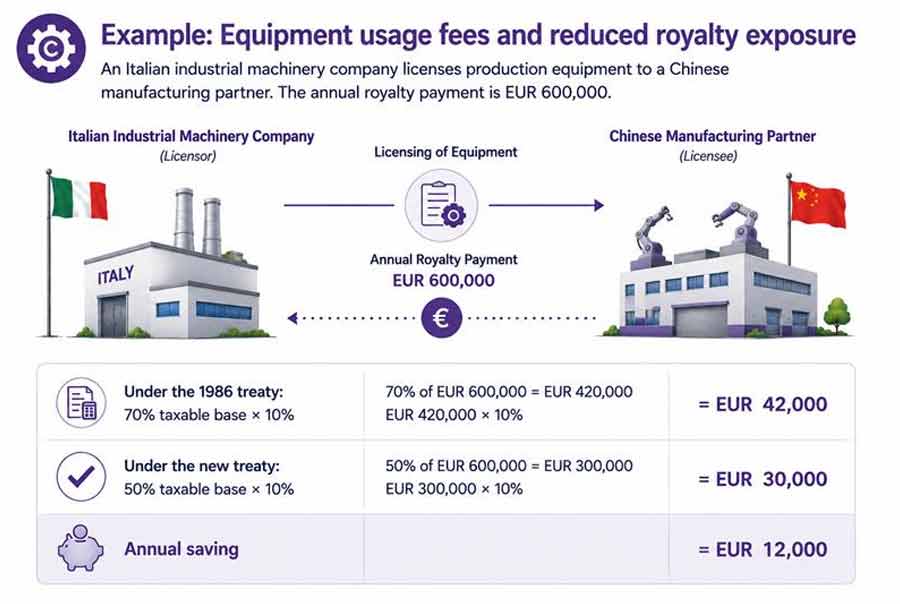

Royalties: A reduced effective rate on equipment and scientific usage

The new treaty maintains the 10 percent cap on the general royalty rate, while offering enhanced terms for specific categories. Previously, royalties for the use of industrial, commercial, or scientific equipment were taxed at 10 percent on 70 percent of the gross payment, producing an effective rate of seven percent. Under the new treaty, only 50 percent of the gross amount is subject to taxation, lowering the effective rate to five percent.

The change reduces the tax barrier for cross-border technology cooperation, particularly for high-end equipment leasing, production line transfer, and equipment-based licensing arrangements between Italian and Chinese parties.

Capital gains and the Principal Purpose Test

The new treaty changes the treatment of capital gains and introduces a Principal Purpose Test (PPT).

Capital gains are now taxed only in the seller’s state of residence, replacing the prior concurrent taxation regime. The exception is sales of qualifying holdings of at least 25 percent, held at any point in the 12 months before the sale, which remain taxable in the source state.

The PPT under Article 24 allows either authority to deny treaty benefits where one of the principal purposes of an arrangement was to obtain a tax advantage. It applies to every treaty claim. Italian holding and licensing entities with limited operational substance are the most exposed.

Treaty access: Chinese-side mechanics

China uses a self-assessment framework. The Italian payee or Chinese withholding agent applies the treaty rate at payment and retains documents for inspection. No prior approval is required.

Core documents:

- A Chinese-language tax residency certificate from the Italian Revenue Agency;

- Beneficial ownership evidence;

- Shareholding and holding-period proof for dividends;

- Loan and use-of-proceeds documentation for interest; and

- Licensing agreements for royalties.

Beneficial ownership is where Italian structures most often fail. The Chinese authorities apply a substance test based on activities, headcount, decision-making, and onward income flows. Conduit structures fail and trigger retroactive assessment at the 10 percent domestic rate.

Article 23: Italian-side credit limitation

Notably, Article 23 limits the creditability of Chinese taxes against Italian taxes where the underlying income is subject to substitute or final withholding tax in Italy.

The main impact is on Italian individuals receiving Chinese-source dividends under the 26 percent Italian substitute tax regime. They can no longer credit the Chinese withholding tax against their Italian liability. Corporate exposure is narrower but should be reviewed case by case.

Permanent establishment risk for Italian service providers

A service permanent establishment (PE) arises in China where an Italian enterprise provides services through personnel for the same or a connected project for more than 183 days in any 12-month period.

Exposure is highest in fashion, machinery, and luxury supply chains, where technical assistance, installation, secondment, and quality control routinely cross the threshold.

A service PE triggers corporate tax filing, profit attribution, and individual income tax for the seconded personnel. Remediation at audit costs significantly more than planning ahead. Italian companies should map current and forecast service contracts against the 183-day threshold now.

What to prepare before the first 2026 payment

Italian companies with material payment flows to or from China should work through the following items before the first post-January 2026 transaction settles:

- Shareholding verification. Confirm that any Italian shareholder claiming the five percent dividend rate has held at least 25 percent of the Chinese paying entity’s capital for a continuous 365-day period covering the planned payment date.

- Beneficial ownership documentation. Refresh the substance file for any Italian holding, financing, or licensing entity receiving China-source income, with current evidence on employees, premises, decision-making, and onward income flows.

- Loan documentation. For interest payments at the eight percent preferential rate, verify maturity terms and produce use-of-proceeds documentation linking the financing to the qualifying investment project.

- Tax residency certificates. Obtain Italian tax residency certificates in Chinese-language format from the Italian Revenue Agency for any treaty claim, valid for the payment year.

- PPT review. Document the commercial purpose of any holding, licensing, or financing arrangement that could be challenged under Article 24 as motivated by tax considerations.

- Service contract day-counts. Map current and forecast Chinese service deployments against the 183-day rolling threshold and adjust contractual structures or rotation patterns where exposure approaches the trigger.

The new DTA is materially more favourable than the 1986 framework, but the benefits are conditional. Italian companies that have completed the documentation, substance, and structural work before payments are released will be in a position to use the new rates. Those reconstructing the file under audit pressure will face a more expensive path. For a practical breakdown of common implementation issues, subscribe us here to see our coming article addressing frequently asked questions on the new China-Italy DTA.

How Dezan Shira & Associates can help

Dezan Shira & Associates supports Italian companies operating in China across the full lifecycle of cross-border tax planning under the new DTA, including treaty eligibility assessment, beneficial ownership and substance review, withholding tax planning, permanent establishment risk assessment, and coordination of payment execution with Chinese banks and tax authorities.

Contact our tax advisory team to review your 2026 payment flows.

With rapid reforms and inconsistent enforcement across the region, companies face challenges at every stage of their lifecycle. Dezan Shira & Associates’ tax advisory teams include experienced tax accountants, lawyers, and former tax officials who help clients navigate these complexities, reduce risk, and optimize tax outcomes—providing clients with comprehensive advisory and compliance support tailored to regional requirements.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article La supremazia delle infrastrutture cinesi traina il settore manifatturiero asiatico

- Next Article