China’s Maternity and Baby Market (Part I): Demographics, Policy, and Market Structure

China’s maternity and baby market is being reshaped by a fundamental shift from volume to value: despite births falling to a record-low 7.92 million in 2025, per-child spending and premiumization are driving roughly seven percent annual growth. Part I of this two-part guide examines the demographic forces, policy landscape, and market structure that define the sector today — the essential context for any foreign brand or investor evaluating entry.

China’s maternity and baby market is being reshaped by a deepening demographic challenge. After a brief Year-of-the-Dragon rebound in 2024, births fell to a record-low 7.92 million in 2025, and the population declined for a fourth straight year. Yet the sector is far from contracting in step with the birth rate.

Instead, growth is increasingly driven by rising per-child spending, premiumization, and the rapid migration of sales online. Annual spending per child aged 0-3 reached around RMB 48,000 (US$7,103) in 2025, and a first-ever national childcare subsidy is now channeling cash directly to young families.

This article, the first in a two-part series, covers the structural forces shaping the market: the demographic transition, the evolving consumer profile, the policy environment, and the key market metrics such as size, category split, channel dynamics, and competitive landscape. Part II examines the specific product and service segments where foreign brands and investors are best positioned to compete, alongside the challenges and entry considerations that apply across the market.

China’s shifting demographics and the changing consumer

China’s long-term demographic trajectory is the single most important context for this market, but its implications are more nuanced than the headline birth numbers suggest.

From birth-rate decline to a value-driven market

According to China’s National Bureau of Statistics (NBS), the number of births fell to 7.92 million in 2025 (the lowest level since 1949), with the population declining for a fourth consecutive year and the total fertility rate hovering near 1.0, far below the 2.1 replacement level. The 9.54 million births recorded in 2024, which had followed seven straight years of decline, proved a temporary, auspicious-year outlier rather than a turning point.

Crucially, this has not translated into a shrinking market. With fewer children born, growth has shifted decisively from volume to value: annual spending per child aged 0–3 rose to around RMB 48,000 (US$7,103) in 2025 and is projected to reach RMB 72,000 (US$10,654) by 2030, a compound annual growth rate of 6–7 percent, according to data compiled by Moojing Market Intelligence. Parents are spending more (on premium, scientifically positioned products) per child than ever before.

Younger, science-minded parents

The market’s center of gravity is the post-1990 and post-1995 generation now entering parenthood. These consumers are more educated, more digitally native, and more research-driven than their predecessors: they consult online reviews and ingredient lists, value clinically validated claims, scan QR codes to verify provenance, and expect brands to engage them through content and community rather than advertising alone. They are also receptive to newer adjacencies, from AI-assisted parenting tools to personalized nutrition.

From “baby first” to “mother and baby”

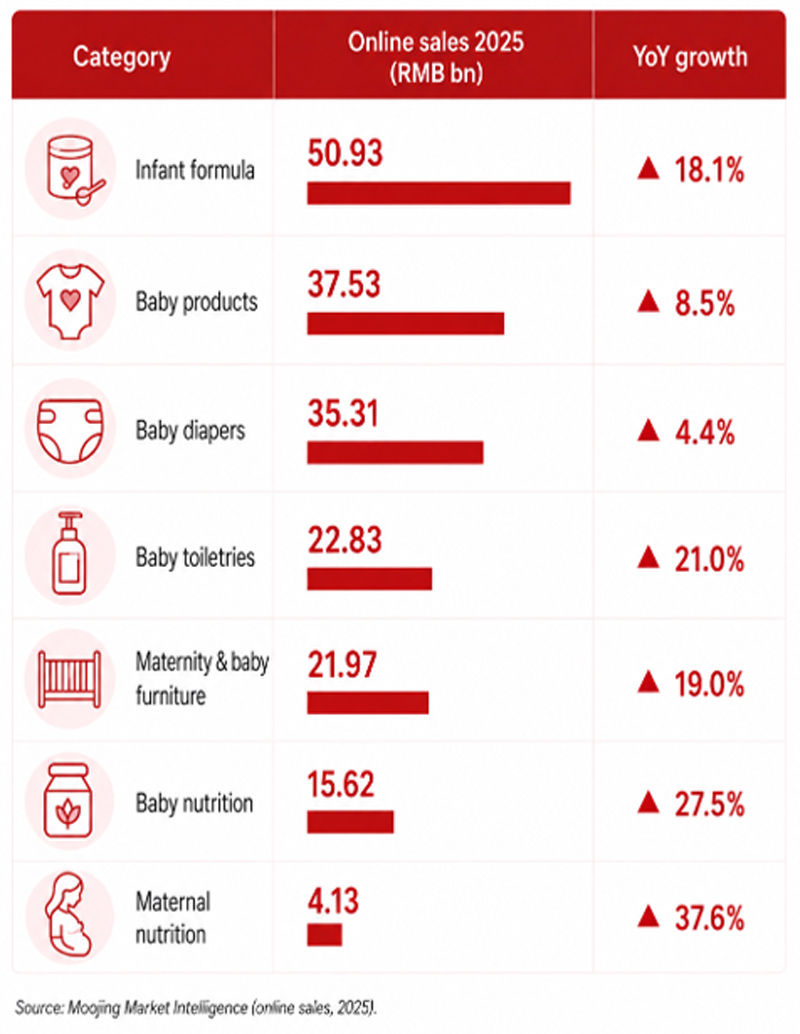

One of the most notable recent developments is the shift from a “baby first” to a “mother and baby equally important” mindset. Maternal nutrition was the fastest-growing major category online in 2025, up 37.6 percent year-on-year, and combined baby and maternal nutrition sales reached around RMB 19.75 billion (US$2.92 billion) online (up 29.5 percent), clear evidence of rising health-consciousness among young parents and a widening of the addressable market beyond the infant alone.

Policy and financial support for China’s maternity and baby market

Faced with persistently low fertility, policymakers have moved from removing birth restrictions to actively subsidizing families. In late July 2025, the State Council announced a nationwide childcare subsidy of RMB 3,600 (US$532) per year for every child under the age of three.

This move sits within a broader pro-natalist framework that includes the three-child policy, extended maternity and parental leave, family-related individual income tax deductions, and a growing list of provincial and municipal birth incentives. Because these measures lift household purchasing power most in lower-tier cities and rural areas, their relative effect on consumption is greatest precisely where future premiumization has the most room to run.

Policy support extends into reproductive health. Assisted reproductive technology (ART) services are now covered by public medical insurance in 27 provinces, benefiting more than one million patients by early 2024, with additional regional subsidies for in vitro fertilization (IVF). These measures directly expand demand for fertility-related products and services.

At the same time, the sector is becoming more tightly regulated, and compliance is now a competitive variable. Infant formula recipes must be registered with regulators, and the updated infant-formula national standards that took effect in 2023 forced widespread reformulation and re-registration, pressure that dented sales even for category leaders.

Looking ahead, the new general food-labeling standards GB 7718-2025 and GB 28050-2025 take effect on March 16, 2027, after a two-year transition, prompting manufacturers and importers to prepare relabeling, allergen declarations, and repackaging now. Authorities have also moved toward continuous, data-driven enforcement of infant-food safety. For agile, compliant, and transparent brands, this tightening can function as a competitive moat rather than merely a hurdle.

China’s maternity and baby market overview

China’s overall baby-care and maternity market was estimated at around RMB 4.63 trillion (US$645 billion) in 2025, growing at roughly seven percent annually. Even after the 2025 birth decline, China still records more than twice as many births a year as the United States, keeping the sector a strategic priority for global consumer brands.

The clearest momentum, however, is online: the maternity and baby online market value reached RMB 223.78 billion (US$33.11 billion) in 2025, up 12.6 percent year-on-year, nearly triple the pace of the overall market.

Category segmentation

The market follows a two-track pattern:

- Established categories: Such as infant formula, baby products, and diapers, provide scale and together account for more than half of the market’s online revenue; and

- Nutrition and lifestyle categories: Deliver the fastest growth.

The infographic below shows the leading categories by online sales in 2025.

Online sales as the preferred channel

The migration to e-commerce is the defining structural change in this market. Online channels’ share of maternity and baby sales rose from 35.1 percent in 2023 to 46.1 percent in 2025, an 11-percentage-point gain in two years that puts e-commerce on track to overtake offline retail within the next two to three years.

Three forces drive the shift:

- Digital-native millennial and Gen Z parents who default to online research and purchasing;

- Subscription-friendly categories such as formula, diapers, and supplements that suit auto-replenishment; and

- The rise of social commerce, where Xiaohongshu and Douyin have become primary trust-building channels.

Specialty mother-and-baby retail chains nonetheless remain an important offline backbone, valued for in-store advice and services, so an omnichannel presence, not a purely online one, remains essential.

Competitive landscape

Key takeaway

China’s maternity and baby market is no longer a demographic-growth story; it is a premiumization, trust, regulation, and lifecycle-consumption story. As birth volumes shrink, the winners are increasingly those who capture a larger share of wallet from a generation of younger, wealthier, and more science-minded parents.

The market structure — the demographics, the policy environment, and the shift to online and omnichannel retail — sets the stage. But understanding where foreign brands and investors can most effectively compete requires a closer look at the individual segments. Part II of this series examines infant formula, maternal and infant nutrition, diapers and baby care, postpartum and childcare services, and assisted reproduction in turn, alongside the key challenges and the entry approaches best suited to each.

How Dezan Shira & Associates can help

Entering China’s maternity and baby market requires more than identifying demand—it demands careful navigation of regulatory requirements, channel strategies, localization, and long-term operational planning. Dezan Shira & Associates supports foreign brands and investors at every stage of market entry and expansion.

We advise on optimal entry strategies—ranging from cross-border e-commerce to local entity setup or joint ventures—tailored to different product and service segments. Our teams assist with regulatory requirements, including infant formula registration, health supplements, and medical device approvals, helping businesses stay compliant in a shifting policy environment.

We also support market validation and go-to-market strategies, including platform selection, distribution planning, and localization. For long-term operations, we provide supply chain advisory, partner identification, and full corporate services covering accounting, tax, and HR, enabling companies to scale efficiently in China.

Whether launching, restructuring, or expanding, we ensure our clients benefit from coordinated input across legal, HR, tax, and financial teams. From startup to exit, our advisory scales with your business—designed to meet both immediate needs and long-term goals.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article 《国务院关于对外投资的规定》对跨国企业的意义

- Next Article China’s Maternity and Baby Market (Part II): Key Segments and Opportunities for Foreign Brands