Transfer Pricing Compliance in China: Key Obligations and Risk Areas

“Do I need transfer pricing documentation in China?”

If your company has related-party transactions in the Chinese Mainland, the answer is very likely yes, and getting it wrong can be costly.

China’s transfer pricing framework is one of the most detailed and strictly enforced globally. Thresholds are clearly defined, compliance expectations are high, and penalties for missteps are real. Understanding where you stand is not just a compliance exercise but a risk management priority.

Below is a clear, practical breakdown of what you need to do, when, and why it matters — based on current effective regulations.

The short answer

If your company has related-party transactions in China, there are three separate obligations to think about:

- Related-party reporting(which applies to virtually every company with intercompany transactions);

- Contemporaneous documentation(which kicks in once certain value thresholds are crossed); and

- Country-by-country (CbC) disclosure (where applicable).

Many companies assume documentation is only required in complex or large cases. In practice, reporting is nearly universal, and documentation requirements arise sooner than expected as operations scale.

Obligation 1: Annual related-party transaction report

If your entity has any related-party dealings, this is non-negotiable.

Any resident enterprise or non-resident enterprise with a permanent establishment in China must attach a set of related-party transaction schedules to its annual corporate income tax return. This is known colloquially as the “Form B” filing — formally the Annual Related-Party Transactions Reporting Package (2016 Edition), which consists of 22 individual schedules.

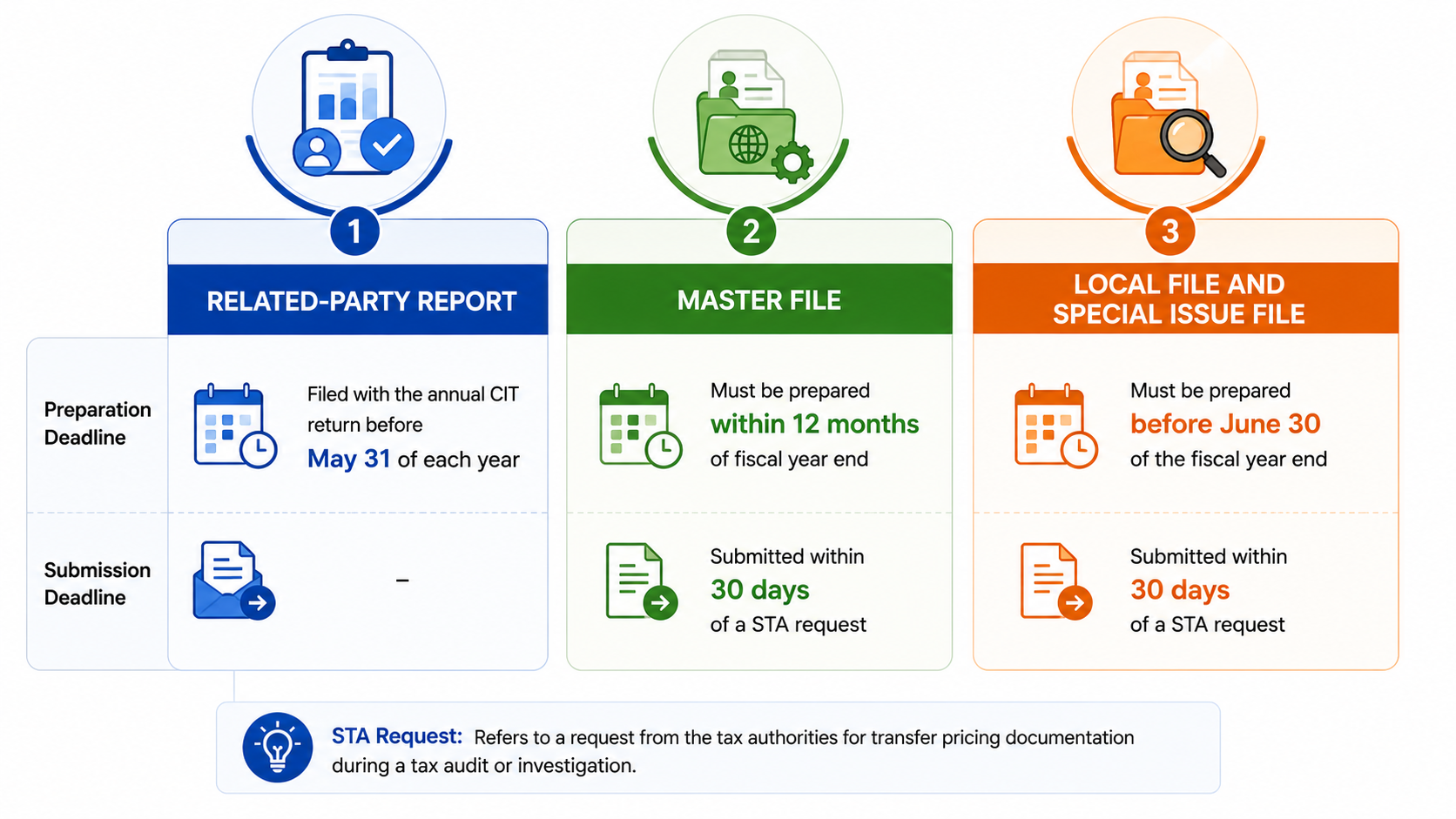

The related-party report must be filed at the same time as the annual CIT return – by May 31 for the previous tax year.

Three of the 22 schedules are mandatory for everyone:

- The reporting entity information table;

- The consolidated summary table; and

- The related-party relationship table.

The remaining 19 schedules are completed only where the relevant transaction types exist.

To be noted, related-party relationships in China are broad. They cover shareholding control (direct or indirect), debt arrangements where one party provides more than 75 percent of the other’s capital, licensing relationships, and even less formal dependencies such as the supply of exclusive raw materials or key management personnel.

Obligation 2: Contemporaneous documentation

Contemporaneous documentation is the more substantive transfer pricing file.

This is where scrutiny intensifies and what most people mean when they ask whether they need a transfer pricing study.

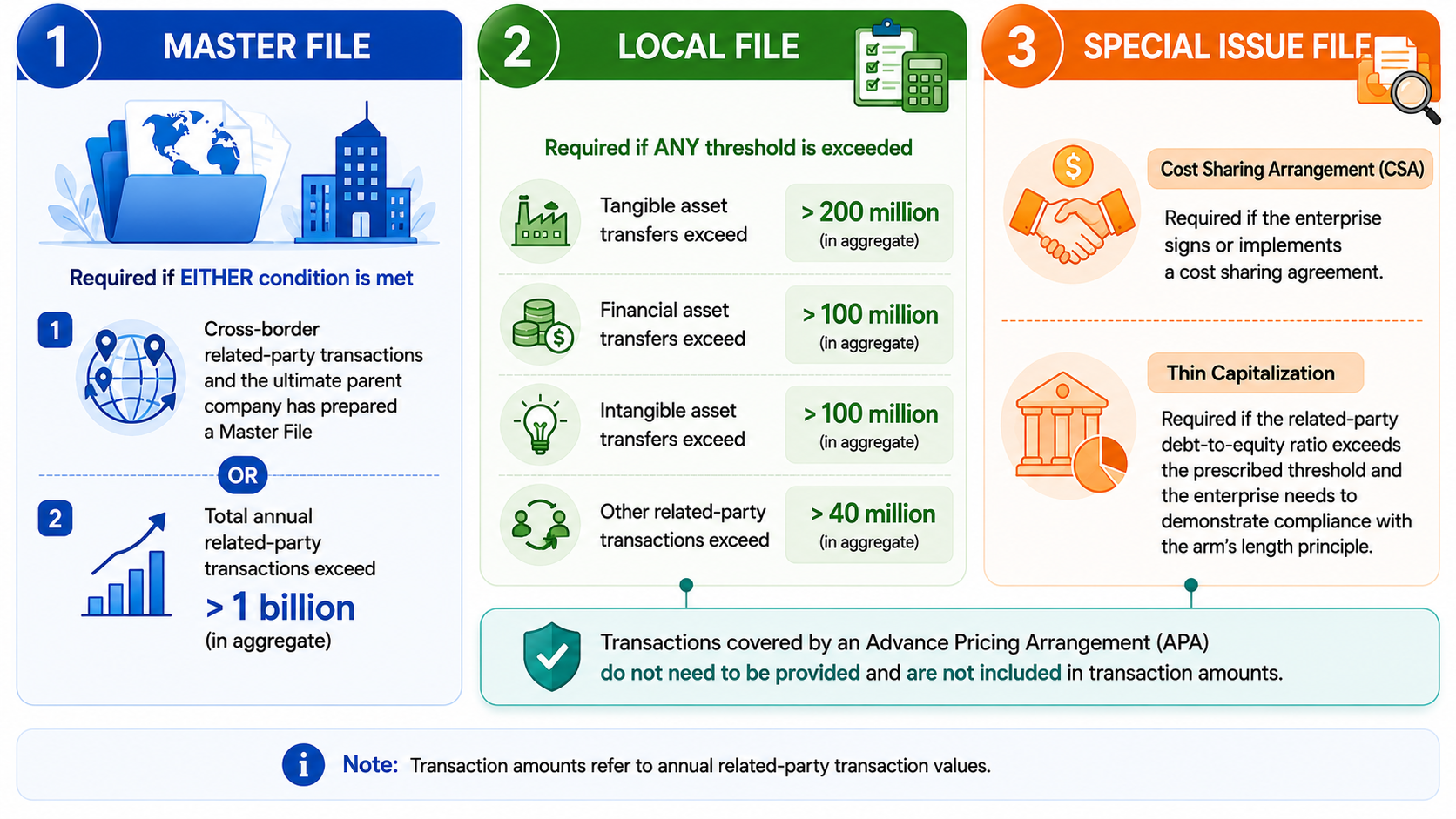

China adopts a tiered documentation system – master file, local file, special issue file, with thresholds that trigger progressively more detailed requirements:

Transfer pricing documentation must be prepared in Chinese and retained for 10 years. Enterprises that engage exclusively in related-party transactions with domestic counterparties in the Chinese Mainland are exempt from preparing the master file, local file, and special issues file.

Loss-Making Manufacturers and Distributors: No Threshold Exemption for Local Files

If your company performs toll manufacturing, contract manufacturing, distribution, or contract R&D exclusively for a foreign related party and records a loss in any year, a local file must be prepared for that loss year, regardless of whether the transaction values cross the thresholds above.

Country-by-country report (group level disclosure)

This is a separate obligation, not part of contemporaneous documentation. CbC reports are used for high-level risk assessment, while contemporaneous documentation is used for detailed audits.

CbC reporting applies to multinational groups at the top of the ownership chain, providing tax authorities with a global snapshot of revenue, profits, tax paid, employees, and asset allocation.

A Chinese resident entity must file a country-by-country report if it is the ultimate parent of a multinational group and the group’s consolidated revenues across all jurisdictions exceeded RMB 5.5 billion in the prior fiscal year.

A Chinese entity can also be designated as the surrogate filer for the group.

Key deadlines at a glance

Key transaction categories in scope

China’s transfer pricing rules cover a wide range of intercompany activities:

- Transfers of tangible assets (goods, products, property, equipment)

- Transfers of financial assets (receivables, equity, debt, derivatives)

- Transfers of intangibles (patents, trademarks, know-how, customer lists, distribution channels)

- Financing (intercompany loans, cash pooling, guarantees, deferred payments)

- Services (management fees, IT services, marketing, R&D, procurement, legal, HR, and similar)

What happens if you don’t comply?

Failure to file the related-party report on time can attract a fine of up to RMB 10,000.

More significantly, if the STA makes a transfer pricing adjustment against a company that did not prepare contemporaneous documentation, interest on any back-taxes runs at the PBOC benchmark lending rate plus five percentage points, considerably higher than the rate applied to compliant taxpayers.

Practical takeaways

China’s tax authorities are increasingly data-driven, using cross-referenced filings (including CbC data) to identify audit targets. A proactive approach not only ensures compliance, but also strengthens your position in the event of scrutiny.

Companies are advised to:

- Assume reporting applies if you have intercompany transactions;

- Map transaction values early against thresholds;

- Pay close attention to limited risk and loss-making entities; and

- Ensure documentation is prepared, not reactive.

The last point is of special importance because proper transfer pricing documentation requires:

- Functional interviews;

- Benchmark studies; and

- Financial segmentation.

If done late, internal data may no longer be available, personnel may have changed, and you may need to rely on estimate rather than evidence. This can weaken the documentation’s credibility, limit available support, and expose the company to higher penalties.

Conversely, having documentation ready allows you to:

- Respond quickly;

- Control the narrative; and

- Demonstrate compliance from the outset.

Dezan Shira & Associates, an Ascentium Company, supports businesses in navigating China and Asia’s complex transfer pricing landscape with practical, end-to-end solutions. We help companies develop compliant transfer pricing policies, prepare robust documentation, and meet local reporting requirements, while proactively managing audit risks. With deep regional expertise, our team delivers tailored strategies, from benchmarking and planning to audit defense and APA support, ensuring your transfer pricing positions are both defensible and aligned with evolving regulatory expectations across multiple jurisdictions. For more details of our service scope, please visit our website here.

Also Read:

- Transfer Pricing Documentation in China: Common Pitfalls and Best Practices

- China Transfer Pricing Documentation Deadline: Prepare Local File and Special Issue File by June 30

- Annual CIT Reconciliation in 2026: Key Areas to Focus

Transfer pricing is a critical area of tax compliance and risk management. Our transfer pricing experts help align your intercompany transactions with the arm’s length principle and local regulations.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article China’s New Infant Food Safety Campaign Signals a Shift Toward Continuous Compliance

- Next Article