The Path to Peak Emissions: Climate and Environmental Policy in China’s 15th Five-Year Plan

China’s clean energy transition will be central to the country’s economic development in the decades to come, driven by both a clear understanding of the threats of climate change and a desire to ensure energy security. The 15th Five-Year Plan outlines a blueprint for achieving the first of the country’s dual carbon target – reaching peak carbon emissions by 2030 – doubling down on renewables build-out and tightening environmental regulations. For foreign companies, these changes will mean both a stricter regulatory environment and myriad business opportunities, as the gargantuan task of greening China’s economy will require efforts and investments from all stakeholders.

The 15th Five-Year Plan (FYP) will shepherd China to reach the first of its two carbon targets: reaching peak carbon emissions by 2030. While the country appears to be on track to reach this milestone – the first of the “dual carbon” targets – sufficiently decarbonizing the economy to definitively cross this threshold will still take immense effort and investment from both policymakers and industries. Taking on this challenge, the 15th FYP outlines a range of measures and policy priorities to reduce carbon emissions across the economy, from heavy industry to consumer products, involving both the ramping up of renewables output and the tightening of environmental regulations and policy tools.

However, China’s ambitions to develop renewables and green industries in the 15th FYP go beyond meeting the peak emissions target; it is also a matter of national security. Ensuring energy security by diversifying energy sources will reduce the reliance on imported fossil fuels, while pushing for breakthroughs in renewables and climate technology will keep the country at the forefront of global technological innovation.

For businesses and investors, the 15th FYP signals both possible tightening of environmental standards and regulations, but also the expansion of a range of new opportunities across both “traditional” renewable supply chains and emerging carbon and energy technology.

| Climate and Low-Carbon Targets in the 15th Five-Year Plan | |||

| Indicator | 2025 | 14th FYP target (2025) | 15th FYP target (2030) |

| Reduction in CO2 emissions per unit of GDP (%) | 17.7 (cumulative over 5 years) | 18 (cumulative over 5 years) | 17 (cumulative over 5 years) |

| Proportion of non-fossil energy in total energy consumption (%) | 21.7 | NA | 25 |

| Reduction in energy consumption per unit of GDP (%) | 11.6* | 13.5 | 10 |

| PM2.5 concentration in cities at the prefecture-level and above (µg/m³) | 28 | NA | <27 |

| Proportion of excellent water bodies (%) | 80 | NA | 85 |

| Forest coverage rate (%) | 25.1 (2024) | 24.1 | 25.8 |

| * Data from 2024. |

|||

Reaching peak carbon emissions by 2030

Key targets:

China is on track to reach its peak carbon target by the 2030 deadline, provided the current pace of renewables build-out and decarbonization of heavy industries is maintained over the next five years. According to research from the Centre of Clean Air and Energy (CREA) for Carbon Brief, China’s emissions have been flat or falling over 21 months starting March 2024, with overall emissions dropping an estimated 0.3 percent in 2025. This is despite emissions from fossil fuels increasing 0.1 percent, with this uptick offset by decreases in heavy industries, in particular cement.

Nonetheless, the analysis suggests that China missed its target of reducing emissions intensity by 18 percent (CO2 emissions per unit of GDP) over the 14th FYP period (2021–2025), with actual emissions intensity falling just 12 percent between 2020 and 2025. China’s official data point for this indicator is a drop of 17.7 percent, also just below the target. This suggests significant efforts will still be needed to ensure momentum holds and a consistent decline in overall emissions can be sustained from 2030 onward.

To keep the country on this path, the plan calls for implementing a combination of “policy guidance and market incentives” to push for greening across the economy from heavy industry to consumer products. This indicates further incentives for key sectors, as well as tighter environmental regulations and emissions-reduction policy tools to compel industries to decarbonize.

There is a particular focus on decarbonizing heavy industries such as thermal power, steel, non-ferrous metals, petrochemicals, chemicals, and building materials.

The plan also pushes for substituting coal consumption, setting the goal of replacing 30 million tons of coal consumption annually, and directs the implementation of non-CO2 GHG control projects in coal mining, planting and breeding, waste treatment, and chemical production to achieve a 30 million-ton CO2 equivalent emissions reduction capacity.

Specific policy tools to improve the monitoring and assessment of emissions mentioned in the plan include implementing systems for local carbon assessment, industry carbon controls, company carbon management, project carbon evaluation, and product carbon footprint.

| Key Tasks for Achieving the Dual Carbon Goals in the 15th Five-Year Plan | |

| Goal | Tasks |

| Conserving energy and reducing carbon in key industries |

|

| Cleaner Substitution of Coal Consumption |

|

| Building zero-carbon industrial parks and transportation corridors

|

|

| Reducing CO2 with the circular economy |

|

| Reducing non-CO2 GHG emissions |

|

| Enhancing the basic capacity for reaching peak carbon and carbon neutrality |

|

The plan also signals that further regulations are on the horizon for product carbon tracking and labeling, calling for formulating product carbon footprint accounting rules and standards, publishing carbon emission limit standards for key products, and establishing a product carbon labeling certification system. It also calls for improving the energy efficiency diagnosis mechanism in key areas and further implementing the energy efficiency labeling and energy efficiency “leader” system, alongside deepening the construction of pilot zones for green, low-carbon, and high-quality development.

The plan also calls for expanding the coverage of the national carbon emission trading system (ETS) and accelerating the construction of a voluntary greenhouse gas emission reduction trading market.

China has already established a blueprint for improving the efficacy of its ETS, which has been largely voluntary since its launch, undermining its potential for changing industry behavior. A set of official opinions released in August 2025 set a directive to establish a total emissions cap for industries covered by the system, shifting the market away from its current intensity-based approach toward one that limits absolute emissions. The document also calls for setting a cap on the volume of carbon emissions allowances (CEAs) and gradually increasing the share of paid allowances relative to free ones, as well as expanding the system to cover all major carbon-emitting industrial sectors.

These changes will see more companies subject to mandatory participation, but also create significant potential for low-carbon industries to benefit from the sale of surplus allowances and participation in voluntary carbon markets.

An important strategy for decarbonizing heavy industries is relocating energy-intensive industries to areas of China that are rich in renewable resources, where possible. The plan calls for “promoting the transfer of qualified high-energy-consuming industries to areas rich in renewable energy resources.” Broadly, this means moving certain energy-intensive industrial sectors and manufacturing from China’s coastal regions inland to provinces that are rapidly expanding renewable output – in particular wind and solar – so that they can run more on green energy.

In a similar vein, the plan sets a target of building over 100 “national-level zero-carbon industrial parks”, so-called because they seek to reduce CO2 emissions from production and daily activities to a “near-zero” level through measures such as developing green power direct supply models, encouraging companies to build ultra-efficient and zero-carbon factories, and developing low-energy-consumption, low-pollution, and high-value-added emerging industries, among other measures.

The greening of the economy also plays an important role in two of China’s top policy priorities for the 15th FYP period: upgrading traditional industries and developing emerging and high-tech industries.

Within the realm of emerging industries, the plan highlights new energy, connected electric vehicles, new solar cells, and new energy storage, while “future industries” include hydrogen energy and nuclear fusion energy. It also calls for innovation in cutting-edge technologies such as CO2 capture and biological digestion, and supports the construction of carbon capture, utilization, and storage (CCUS) demonstration projects.

While the plan does not outline specific targets for battery storage, it encourages “advancing key technology innovations such as […] new solar cells and new energy storage”.

Expansion of renewable infrastructure

The scale of China’s energy infrastructure has expanded at a rapid rate over the last decade as the country has strived to keep up with growing energy needs, and the renewables sector has taken off.

By the end of 2025, China’s total installed power generation capacity reached 3,890 GW, according to the National Energy Administration (NEA), making it by far the largest electricity producer in the world. Of this, solar power installed capacity reached 1,200 GW, soaring 35.4 percent from the previous year, while wind power was 640 GW, up 22.9 percent from 2024. Thermal installed capacity still accounted for the largest share, at 1,539 GW.

Building on the huge expansion of renewable energy infrastructure over the last five years, the 15th FYP lays out ambitious goals to continue adding to the country’s renewable capacity, in particular wind and solar. The plan calls for “accelerating the construction of a clean, low-carbon, safe, and efficient new energy system” and replacing fossil fuels with non-fossil energy, including wind, solar, hydro, and nuclear power. It also explicitly states that China will “implement a 10-year action plan to double the amount of non-fossil fuel energy”.

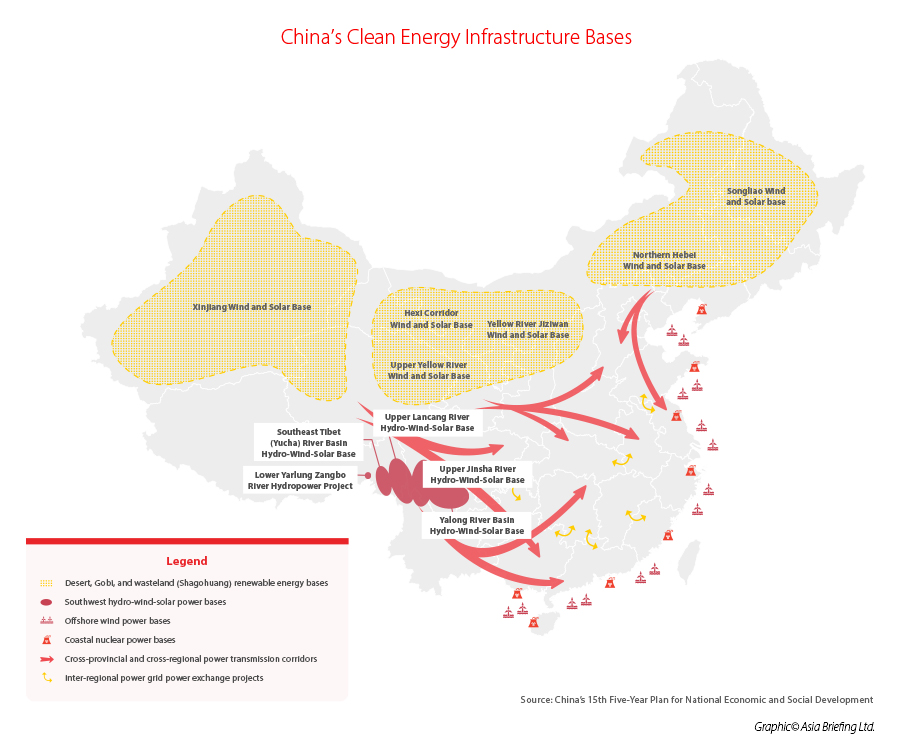

China’s renewable infrastructure build-out is focused heavily on the expansion of solar, wind, and hydropower. In the renewable infrastructure planning, integrated wind and solar projects are concentrated across the “Three North” regions – northwest, northern, and northeast China – while integrated wind, hydro, and solar power are clustered in southwest China, where there are significant hydropower resources, in particular in eastern Tibet, western Sichuan, and northwestern Yunnan. Coastal nuclear power and offshore wind power are planned along China’s eastern coastline.

Beyond expanding renewable generation capacity, an important aspect of China’s future renewable energy infrastructure will be the ability to transmit power from resource-rich regions – largely in inland China – to the power-hungry eastern regions where the majority of the population and industry reside. Over the 15th FYP period, China plans to expand west-to-east transmission capacity from clean energy bases in the “Three North” regions to over 420 GW, up from 340 GW in January 2026.

|

Planned Renewable Energy Projects in the 15th FYP |

||

| Project | Location | Target capacity |

| West-to-east power transmission lines | Transmission from clean energy bases in Inner Mongolia, Jilin, Heilongjiang, Gansu, Qinghai, Ningxia, Xinjiang, and Tibet | Transmission capacity of over 420 GW |

| Coastal nuclear power plants | Coastal provinces | Installed capacity of around 110 GW |

| Offshore wind power bases | Bohai Sea, Yellow Sea, East China Sea, and South China Sea | Installed capacity of over 100 GW |

| Pumped-storage power stations | Areas with good site resources and high load regulation needs | Adding around 100 GW of installed capacity |

Improving storage capability will also be crucial to enhancing the reliability and stability of renewable energy in the grid, as well as improving its utilization. From an infrastructure perspective, the plan focuses on the construction of pumped storage power stations, aiming to add around 100 GW of installed capacity over the next five years. China’s total operational pumped storage capacity stood at 62.4 GW as of August 2025, according to the NEA. The sector nonetheless remains significantly underdeveloped, with only around 4 percent of China’s estimated 1,600 GW of pumped storage resources having been exploited.

Strengthening environmental regulations

The 15th FYP outlines a range of regulatory mechanisms to improve environmental protection that will have a significant impact on industry and business in China.

The plan calls for “advancing the battle against pollution and improving the quality of the atmosphere, water, and soil”, with a particular focus on industrial areas including the Beijing-Tianjin-Hebei (Jing-Jin-Ji) region and surrounding areas, the Yangtze River Delta, the Fenwei Plain, and the Chengdu-Chongqing region. It outlines several mechanisms to improve air and water quality, including strengthening air pollution prevention and control systems and improving the governance and protection of important rivers, lakes, and reservoirs.

The plan sets a number of core pollution reduction targets, including reducing nitrogen oxide and volatile organic compound (VOC) emissions by more than 8 percent, respectively, and reducing chemical oxygen demand (COD) and total phosphorus emissions by 6 percent, respectively.

China will also seek to strengthen whole-process supervision of hazardous waste, focusing on controlling heavy metal pollution risks and conducting investigations and rectification of historical risks such as waste residue sites, mines, and tailings ponds.

For the first time, the plan addresses “persistent organic pollutants, endocrine disruptors, antibiotics, and microplastics” by establishing a collaborative governance and risk management system, reflecting growing awareness of these pollutants and their potential harm to human health.

Companies operating in China have already had to comply with a range of environmental regulations, including mandatory environmental impact assessments, pollutant discharge permits, and approvals for the handling of hazardous waste. The 15th FYP’s emphasis on reducing pollutants and tightening environmental standards signals that compliance requirements are set to increase further over the plan period, with stricter thresholds and broader regulatory coverage likely across key industries.

Implications for businesses in China

The 15th FYP’s green agenda could mean new compliance challenges for businesses operating in China. The plan’s emphasis on issues such as pollution control and carbon tracking means companies can expect a more demanding regulatory environment across several fronts. The planned introduction of product carbon footprint accounting rules, carbon emission limit standards, and a product carbon labeling certification system will create new tracking and disclosure obligations for manufacturers.

Energy efficiency requirements are also set to tighten, with the plan calling for improvements to the energy efficiency diagnosis mechanism and further implementation of the energy efficiency labeling and “leader” system. Companies in energy-intensive industries can therefore anticipate more rigorous assessments and benchmarking against set standards.

The expansion of the national ETS will be among the most consequential developments for carbon-intensive industries. The shift from an intensity-based system to one with absolute emissions caps, combined with a gradual increase in the share of paid allowances, will raise the cost of carbon for covered industries and bring more sectors into mandatory participation. Companies that have not yet engaged seriously with their carbon exposure will face growing financial and regulatory pressure to do so.

For low-carbon and clean technology businesses, these changes also present new opportunities. The expansion of the ETS and the development of a voluntary carbon market create potential revenue streams from the sale of surplus allowances and carbon credits. Companies that invest early in decarbonization and clean production stand to benefit competitively as standards tighten and carbon costs rise across the economy.

Opportunities for foreign investors

While tightening environmental regulations will place higher compliance burdens on companies operating in China, the scale of investment going into China’s green transition also opens up a significant range of commercial opportunities.

Some renewables sectors, such as wind and solar manufacturing, are already dominated by Chinese companies, making entry for foreign companies difficult. However, the scale of investment needed to transition China’s economy off fossil fuels means there are still a wide range of opportunities across the value chain. The build-out of renewable energy infrastructure, zero-carbon industrial parks, and west-to-east transmission networks will drive sustained demand for specialist equipment, engineering services, and advanced materials, while in certain sectors, such as offshore wind and nuclear power, there is still demand for foreign expertise.

The push to develop new energy storage, hydrogen energy, CCUS, and next-generation nuclear technologies under the plan’s “future industries” agenda presents longer-term opportunities for foreign firms with capabilities in these areas, where China is actively seeking to accelerate innovation and international collaboration.

Foreign investors in these areas are also actively encouraged under China’s Catalog of Industries Encouraged for Foreign Investment, which includes a range of green and clean technology sectors. On the energy side, the catalog includes offshore wind and marine renewable energy equipment design and development, thin-film photovoltaic cells and building-integrated solar components, and fuel cell carbon carrier materials for the new energy sector. In manufacturing, encouraged activities include the production of equipment for CCS and CCUS projects, greenhouse gas monitoring and metering equipment, advanced air and water pollution control equipment, and solid waste treatment and disposal machinery. Waste heat recovery technology for energy-saving and carbon reduction in industrial processes is also listed, as are high-quality processing technologies for natural fibers meeting green and low-carbon standards.

There is also significant potential in the services sector. The evolution of the ETS from a largely voluntary, intensity-based system to one with an absolute emissions cap will create demand for carbon management, monitoring, and verification services, as well as low-carbon technology solutions across covered industries. Similar opportunities may also arise from the emerging regulatory framework around product carbon footprints, carbon labeling, and energy efficiency standards, with demands for certification, testing, and consultancy services, particularly as Chinese manufacturers face growing pressure from both domestic regulators and international trading partners to track the carbon footprints of exported goods.

Established companies require dependable solutions to ensure strong risk management and compliance. We help clients create sustainable value in Asia by better addressing their areas of operational, financial, and reputational risk. Our Compliance and Risk Management teams specialize in fraud prevention, financial statement audits, sustainability and ESG compliance, special purpose reviews, and risk adviory and fraud investigation.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Do I Need a License to Operate Online in China? A Guide for Foreign Companies

- Next Article Hong Kong’s Evolving Double Tax Agreement (DTA) Network 2026