China’s Nuclear Fusion Sector: What the 15th FYP Means for Businesses and Investors

China’s nuclear fusion sector is rapidly taking shape as an emerging industrial market, with increasing investment and activity across reactor supply chains, advanced materials, and engineering systems. While commercial power generation remains a long-term goal for the 2030s–2040s, near-term business opportunities are already developing in component manufacturing, testing infrastructure, and technology partnerships.

China’s nuclear fusion push is creating early-stage commercial opportunities across high-value industrial segments, including advanced components, engineering systems, and specialized supply chains. While fusion power generation remains a long-term objective, current policy direction and investment flows are already driving demand for technologies that enable reactor development.

The outline of the 15th Five-Year Plan for Economic and Social Development (15th FYP), released in March 2026, identifies “hydrogen and nuclear fusion energy” as key future industries, alongside quantum technology, bio-manufacturing, brain-computer interfaces, embodied intelligence, and 6G.

This inclusion signals growing policy attention, but fusion remains an early-stage technology with long development timelines and significant technical uncertainty. While recent progress in research and engineering has been notable, large-scale commercial deployment is still likely to take decades.

Against this backdrop, China’s approach is best understood not only in terms of technological progress, but through the industrial and policy framework shaping market entry points. This article examines how nuclear fusion is being integrated into China’s industrial strategy, where near-term business opportunities are emerging, and what this means for industry participation.

Key takeaway for businesses

China’s nuclear fusion sector is not yet a market for energy production, but it is already generating demand across upstream industrial segments. The most immediate opportunities lie in supplying components, engineering capabilities, and enabling technologies that support reactor development and demonstration projects.

How China is structuring the fusion market: Policy, funding, and entry points

While the 15th FYP positions nuclear fusion as a future growth area, the more important development lies in how the sector is being structured and supported. Rather than establishing a standalone industry, policymakers are embedding fusion within a broader system of industrial policy, research coordination, and state-backed financing.

Where fusion fits in China’s industrial priorities

Fusion is incorporated into China’s “future industries” agenda and, more specifically, within the “future energy” category alongside nuclear, hydrogen, and biomass. This allows it to be developed as part of a wider portfolio of strategic technologies, rather than in isolation.

The approach reflects a shift in emphasis. Fusion is still treated as a long-term technology, but it is increasingly being linked to industrial planning and future economic growth objectives.

How investment and pilot programs are creating early demand

The 15th FYP introduces a set of mechanisms aimed at accelerating the transition from research to application. These include:

- Demonstration projects and pilot engineering programs;

- Proof-of-concept platforms and dedicated research institutes;

- Risk-sharing frameworks for high-cost, high-uncertainty technologies;

- Industrial pilot zones and testing environments; and

- Coordinated financing channels, including state funds, policy banks, and local government support.

At the same time, the plan targets annual growth in research and development spending of more than seven percent, reinforcing expectations of continued investment in frontier technologies.

Who drives China’s nuclear fusion secor: Key institutions and market actors

These measures build on earlier policy guidance, particularly the 2024 implementation opinion issued by multiple agencies, including the Ministry of Industry and Information Technology, the Ministry of Science and Technology, and the Chinese Academy of Sciences.

In practice, this creates a multi-layered system:

- Research institutions lead scientific development

- Central ministries define policy direction and funding priorities

- State-owned enterprises are increasingly involved in engineering and commercialization

- Regulatory bodies, such as the Ministry of Ecology and Environment, are beginning to establish licensing and safety frameworks

This marks a transition from fragmented research efforts to a more integrated development model.

How the sector is financed: Investment channels and capital flows

One notable feature is the lack of a clearly defined national fusion budget. Instead, funding is distributed across multiple channels:

- Central government R&D programs;

- State-owned enterprise investment;

- Local government funds; and

- Strategic capital and public-private financing.

While this limits visibility on total spending, it also indicates that support for fusion is embedded across several parts of the state system.

Industry takeaway

China is building the foundations of a fusion industry before it becomes commercially viable. In the near term, development is likely to be driven by policy-backed investment and coordinated planning rather than market demand.

For companies, this suggests that opportunities will emerge first in:

- Demonstration projects;

- Supply chains and component manufacturing; and

- Supporting technologies and engineering services.

Direct participation in fusion power generation, however, remains a longer-term prospect.

Technology readiness: From research to engineering demand

China’s fusion programme is moving beyond isolated experimental breakthroughs and toward a more structured pathway that links research with engineering validation. While the technology remains pre-commercial, the current generation of facilities reflects a clearer progression toward reactor-relevant systems.

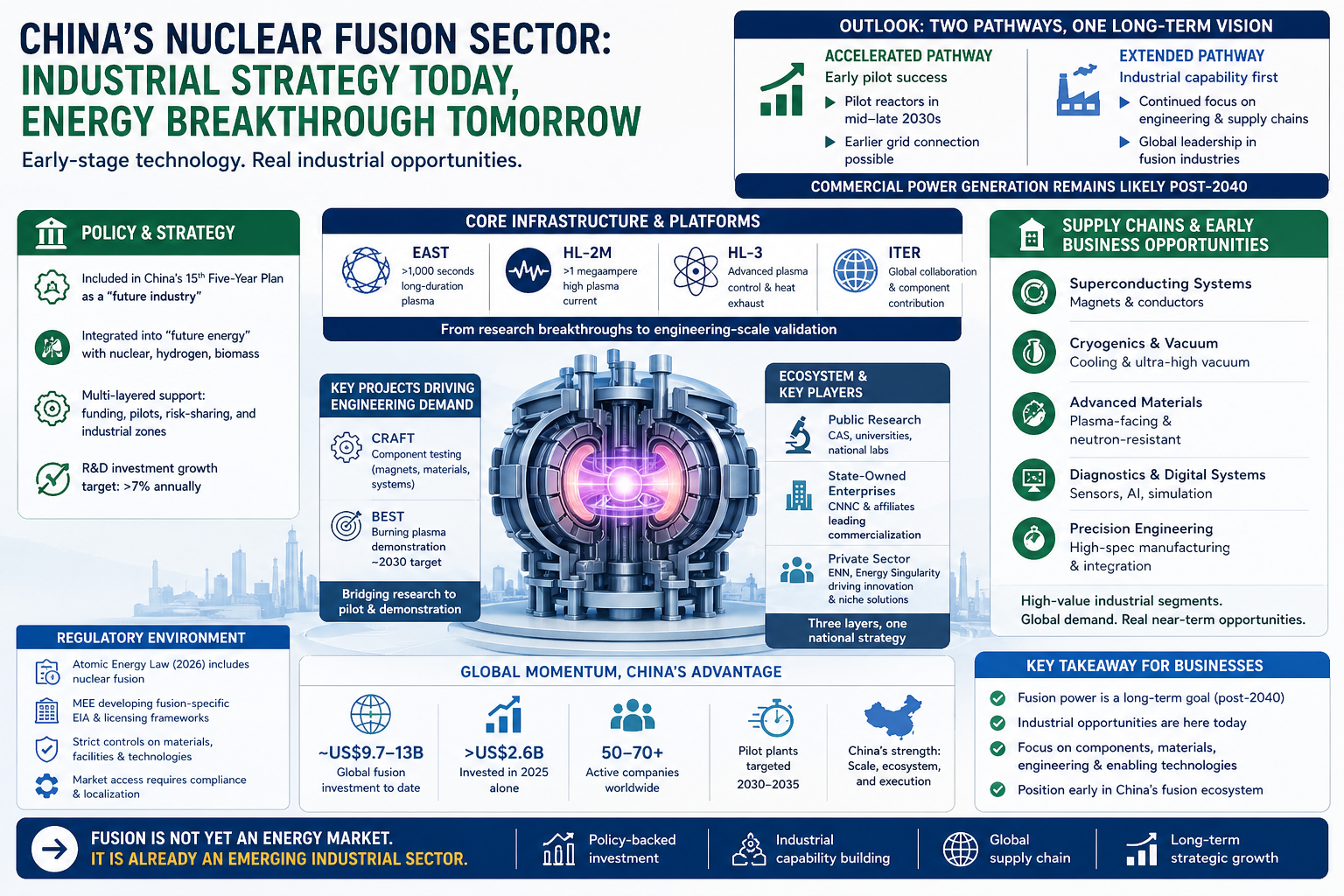

Core infrastructure: The platforms driving technology development

China’s fusion capabilities are anchored in a set of major research platforms that together support long-duration operation, plasma control, and system integration.

China’s current fusion capabilities can be understood through the following core platforms:

| Platform | Lead institution | Key focus | Recent milestone | Role in development pathway |

|---|---|---|---|---|

| EAST | Chinese Academy of Sciences (ASIPP) | Long-duration plasma confinement | Sustained high-confinement plasma for over 1,000 seconds | Validates steady-state operation for future reactors |

| HL-2M | Southwestern Institute of Physics | High plasma current regimes | Achieved operation above 1 megaampere | Transitional experimental platform |

| HL-3 | SWIP / ITER-linked research | Advanced plasma control and heat exhaust | High-temperature plasma and ITER-aligned campaigns | Next-generation research system |

| ITER participation | International collaboration | Large-scale system integration | Ongoing contribution to components and research | Access to global knowledge and supply chain |

Taken together, these platforms show that China is developing a layered research system rather than relying on a single flagship project. This approach supports both domestic capability building and integration into international fusion efforts.

From labs to systems: Where engineering demand is increasing

The most important shift is the move from experimental physics to engineering-scale validation. China is increasingly investing in facilities designed to test components, systems, and reactor-relevant conditions.

This transition is illustrated by the following projects:

| Project | Type | Function | Strategic role |

|---|---|---|---|

| CRAFT | Research infrastructure | Testing and validation of key components, including superconducting magnets and materials | Supports development of reactor-grade systems |

| BEST | Experimental reactor | Designed to achieve burning plasma conditions and test energy gain | Bridge toward pilot and demonstration reactors |

These projects indicate that China is not only advancing scientific understanding, but also building the engineering capabilities required for future reactor deployment.

Key technical constraints shaping timelines and investment risk

Despite recent progress, several core challenges remain unresolved and continue to define the timeline for fusion commercialization:

- Plasma stability and control: Maintaining stable plasma over long durations remains a central challenge for continuous operation

- Materials and heat management: Reactor components must withstand extreme temperatures and neutron exposure, requiring advanced materials

- Tritium fuel cycle: Sustainable fuel production and handling systems are essential for long-term operation

These constraints are common across all major fusion programmes globally and remain critical bottlenecks.

Market structure: Who is building China’s nuclear fusion industry

China’s fusion push is not limited to research institutions. A broader industrial ecosystem is taking shape, combining public laboratories, state-owned enterprises (SOEs), and an emerging private sector. This layered structure is one of the defining features of China’s approach and underpins its ability to move from research toward industrial capability.

Ecosystem structure: Public, state, and private layers

China’s fusion industry is developing across three interconnected layers:

| Layer | Key actors | Role | Strategic function |

|---|---|---|---|

| Public research | Chinese Academy of Sciences, universities, national labs | Fundamental research and experimental platforms | Scientific foundation and talent development |

| State-owned enterprises | China National Nuclear Corporation and affiliated entities | Engineering, system integration, commercialization | Scaling and infrastructure development |

| Private sector | ENN Science and Technology Development Co., Ltd., Energy Singularity | Technology development and niche innovation | Flexibility, cost efficiency, and new approaches |

This structure allows China to combine long-term research with industrial execution capacity, reducing the gap between laboratory results and deployable systems.

SOEs and commercialization: Who will control large-scale deployment

A key feature of China’s model is the early involvement of state-owned enterprises. Rather than waiting for technological maturity, SOEs are already being positioned to lead future commercialization.

The establishment of China Fusion Energy Co. by China National Nuclear Corporation reflects this approach. Backed by a mix of state capital and strategic investors, the entity is designed to:

- Aggregate engineering and project development capabilities;

- Serve as a platform for future reactor deployment; and

- Channel investment into large-scale fusion infrastructure.

This early institutional setup reduces uncertainty around future ownership and operational models.

Private sector role: Where innovation and niche opportunities are emerging

China’s private fusion ecosystem remains relatively small compared to that of the United States, but it is gaining traction.

Key players include:

- ENN Science and Technology Development Co., Ltd.: Participates in international fusion research collaborations, and its focus is on experimental systems and physics research.

- Energy Singularity: Develops high-temperature superconducting tokamaks. Emphasizes cost reduction and domestic supply chains

While the number of companies is limited, funding is relatively concentrated, often supported by state-linked capital. This results in a smaller but more capital-intensive ecosystem.

Where the real opportunities are: Fusion supply chains and enabling industries

Beyond reactors themselves, a broader supply chain is beginning to form. This includes capabilities in:

| Segment | Key capabilities | Industrial relevance |

|---|---|---|

| Superconducting systems | Magnets and related components | Core to plasma confinement |

| Cryogenics | Cooling systems for superconducting materials | Enables reactor operation |

| Advanced materials | Plasma-facing and neutron-resistant materials | Determines durability and cost |

| Vacuum and precision engineering | High-spec manufacturing and assembly | Required for reactor construction |

| Digital and control systems | Diagnostics, simulation, AI-based control | Improves efficiency and stability |

Many of these capabilities have applications beyond fusion, including in aerospace, conventional nuclear, and advanced manufacturing. This creates spillover benefits that justify continued investment.

- Key projects:

- BEST (burning plasma demonstration)

- Future pilot systems (CFETR/CFEDR pathway)

- Likely business model:

- SOE-led demonstration plants

- Public-private co-financing

- Cluster-based deployment

- Timeline outlook:

- Pilot systems: mid–late 2030s (conditional)

- Commercial deployment: post-2040

- Industry implication:

- Near-term returns unlikely from electricity generation

Key supply chain segments with commercial potential

While fusion power generation remains a long-term objective, the most immediate commercial opportunities are emerging in enabling technologies and industrial supply chains. As fusion systems move from experimental validation toward engineering-scale deployment, demand is increasing for specialized components, high-performance materials, and system integration capabilities.

This shift is already visible at the global level. The fusion sector has attracted approximately US$9.7–13 billion in cumulative investment, with more than 50–70 companies active worldwide, and annual funding exceeding US$2.6 billion in 2025 alone.

This rapid capital inflow is not yet generating electricity, but it is already driving industrial demand across upstream segments.

Core supply chain segments

The fusion value chain is taking shape across several critical industrial areas:

| Segment | Key capabilities | Industrial relevance |

|---|---|---|

| Superconducting systems | High-performance magnets and conductors | Core to plasma confinement systems |

| Cryogenics and vacuum systems | Cooling and ultra-high vacuum environments | Enables stable reactor operation |

| Advanced materials | Plasma-facing and neutron-resistant materials | Determines durability and lifecycle costs |

| Diagnostics and digital systems | Sensors, simulation, AI-based control | Improves plasma stability and system performance |

| Power and precision engineering | High-spec manufacturing and integration | Required for reactor construction and scaling |

These segments are already seeing increased demand as fusion programmes expand globally. Importantly, many of them are not fusion-specific industries. They overlap with established sectors such as nuclear energy, aerospace, semiconductors, and advanced manufacturing, allowing companies to leverage existing capabilities.

Industrial spillovers and early-stage market formation

Even without commercial reactors, the fusion ecosystem is generating measurable industrial activity:

- The number of fusion companies has more than doubled since 2021, reflecting rapid ecosystem expansion.

- Supply chain employment linked to fusion is projected to reach tens of thousands of jobs globally in the coming decade.

- Large-scale projects (for instance, ITER and national programmes) are already creating demand for high-precision manufacturing, advanced materials, and complex system integration.

In China’s case, this dynamic is amplified by strong domestic manufacturing capacity and state coordination, which allow fusion-related supply chains to scale more quickly than in more fragmented ecosystems.

Regulatory environment and market access

China’s regulatory framework for fusion is evolving alongside its technological progress, with increasing efforts to establish a formal legal and licensing system.

Legal foundation: Atomic Energy Law

The most important development is the implementation of the Atomic Energy Law, which came into force in January 2026 and which provides a comprehensive legal framework covering:

- Nuclear research, development, and utilization;

- Safety supervision and licensing;

- Nuclear fuel cycle and materials control; and

- Security, export controls, and liability.

Importantly, it explicitly includes nuclear fusion within its scope, placing it under the same national regulatory architecture as other nuclear technologies.

The law also mandates strict control over nuclear materials and facilities, including licensing requirements and security measures, reflecting the dual-use nature of fusion-related technologies.

Fusion-specific regulatory development

Beyond the legal framework, regulators are beginning to define more targeted rules for fusion. The Ministry of Ecology and Environment (MEE) is developing:

- Environmental Impact Assessment Guidelines for Fusion Devices; and

- Licensing Frameworks Tailored to Fusion-Specific Risks.

These efforts reflect an important transition: fusion is no longer treated as purely experimental, but as a technology that will require standardized approval pathways for future deployment.

At present, fusion facilities are regulated under existing radiation and environmental frameworks, while a more dedicated regime is still under development.

Market access constraints

Despite increasing regulatory clarity, access remains tightly controlled:

- Export controls on nuclear and dual-use technologies;

- Intellectual property localization requirements; and

- National security oversight on sensitive systems.

These constraints are reinforced by the Atomic Energy Law, which strengthens control over nuclear materials, facilities, and related technologies.

Outlook: Industrial strategy first, energy breakthrough later

China’s fusion programme should be understood primarily as an industrial strategy rather than an imminent energy solution. While the long-term objective remains grid-scale fusion power, current developments suggest that the near- to medium-term impact will be felt more strongly in industrial capability, supply chains, and engineering systems.

Fusion in the global timeline: Converging expectations, uncertain delivery

Globally, fusion is entering a transitional phase. Investment and activity have accelerated significantly, with total funding exceeding US$10 billion and more than 160 fusion devices under development worldwide.

Industry projections are increasingly converging around the early 2030s for pilot-scale deployment:

- Most companies target pilot plants between 2030 and 2035;

- Only a small number expect commercial operation before 2030; and

- Full-scale deployment remains more likely post-2040.

China’s own targets, such as the BEST project aiming for demonstration of net energy gain around 2030, are broadly aligned with these global timelines, though often more ambitious in execution.

At the same time, recent industry data shows that the bottleneck is shifting. Fusion is no longer constrained purely by physics, but increasingly by engineering, materials, and system integration challenges.

Two scenarios: Early commercialization vs long-term industrial growth

Given these conditions, China’s fusion trajectory can be understood through two parallel scenarios:

1. Accelerated pathway: Early pilot success

- Successful demonstration of burning plasma and net energy gain;

- Transition to pilot reactors in the mid-to-late 2030s; and

- Earlier-than-expected move toward grid-connected systems.

2. Extended pathway: Industrial capability first

- Delays in achieving reactor-level performance;

- Continued focus on component development and engineering systems; and

- Emergence of China as a leading supplier in the global fusion value chain.

In practice, the second scenario is not a failure case. Even without near-term commercialization, fusion-related industries (such as superconducting systems, advanced materials, and high-precision manufacturing) are already generating economic and technological spillovers.

Key risks: What could delay or accelerate commercialization

Despite strong momentum, several variables will determine how quickly fusion transitions from experimental to commercial:

- Technical milestones: Achieving stable, continuous operation and net energy gain remains unresolved globally.

- Regulatory evolution: Licensing frameworks for fusion facilities are still being defined, particularly for tritium-based systems

- Capital requirements: The sector remains highly capital-intensive, with individual projects potentially requiring billions in investment and continued public support.

- System integration challenges: Moving from experimental devices to reliable, grid-connected systems remains a major engineering hurdle.

These factors suggest that while progress is accelerating, timelines remain uncertain and subject to technological risk.

Industry takeaway

China’s fusion programme is unlikely to create a near-term market for electricity generation. However, it is already shaping a new industrial landscape.

- Fusion is not yet an energy market; and

- It is already an emerging industrial sector.

For businesses, this distinction is critical. The most immediate opportunities lie in:

- Advanced manufacturing and materials;

- Engineering systems and infrastructure; and

- Supply chains linked to fusion development.

Over time, if technical milestones are achieved, these capabilities may position China not only as a fusion energy producer, but as a dominant player in the global fusion industry.

Final takeaway

China’s fusion strategy is less about short-term energy production and more about long-term industrial positioning.

The key question is no longer whether fusion will be developed, but who will control the technologies, supply chains, and systems that make it possible.

Whether launching, restructuring, or expanding, we ensure our clients benefit from coordinated input across legal, HR, tax, and financial teams. From startup to exit, our advisory scales with your business—designed to meet both immediate needs and long-term goals.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article China Cybersecurity Label Explained: Why ‘Optional’ Doesn’t Mean Irrelevant

- Next Article