China’s SAT Details VAT Reform Issues in Shanghai

Nov. 18 – The value-added tax (VAT) reform projected to take place in Shanghai next year will be China’s first step towards resolving the issue of duplicate taxation on goods and services. While in the existing Chinese taxation system, most types of services (with the exception of processing, repair and replacement services) are subject to business tax (BT), the coming reform will make a larger amount of services – mostly provided in Shanghai’s transport sector and several modern service sectors – become VATable rather than BTable. The implementation details on the reform were recently specified in a circular co-issued by the State Administration of Taxation (SAT) and the Ministry of Finance (MoF).

The “Circular on Commencing the VAT Reform (Replacing BT Imposition with VAT Imposition) in Shanghai’s Transport Industry and Several Modern Service Sectors (caishui [2011] No.111)” released on November 16, explains multiple issues including services that become VATable, VAT rates, as well as calculation methods, taxpayer status and favorable VAT treatment to specific services.

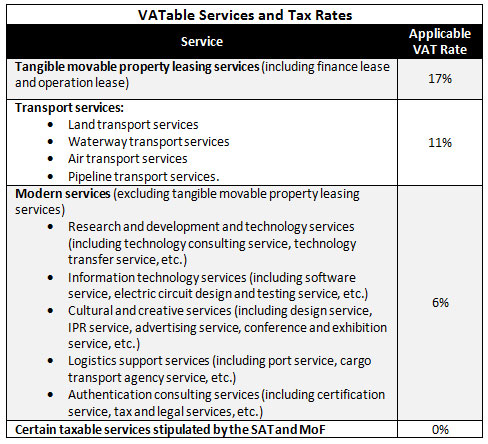

VATable services and VAT rates

Starting on January 1, 2012, transport services and six types of modern services will be subject to VAT payment.

VAT calculation

If a taxpayer engages in both the sale of goods and VATable services that are subject to different VAT rates, they shall calculate the sales value of goods/services separately; otherwise, the VAT shall be charged on the total sales value at the highest rate.

Similar to existing VAT payers, taxpayers engaging in the newly-included VATable services can also apply for the status of VAT General Taxpayer, as long as their annual sales value of VATable services reaches RMB5 million. Taxpayers providing road and inland waterway cargo transport services – if they currently have the right to issue invoices – can apply for the status of General Taxpayer as well, even if their annual sales value is below the RMB5 million-threshold.

General taxpayers can have input VAT deducted from their output VAT, therefore, they shall calculate their VAT liability following the formulas below:

- VAT liability = Output VAT during the term – input VAT during the term

- Output VAT = Sales value × Corresponding VAT rate

For taxpayers that have included the output VAT they are charged into the pricing of goods/services, sales value shall be calculated as such:

- Sales value = VAT-included sales value ÷ (1 + corresponding VAT rate)

When existing general taxpayers buy the newly-announced VATable services provided by other general taxpayers, the input VAT they are charged – as long as it is specified on the VAT invoices – can also be deducted from their output VAT later.

Small-scale taxpayers will not be able to offset their input VAT, so they shall calculate their VAT liability following the formula below:

- VAT liability = Sales value × VAT rate for small-scale taxpayers

General taxpayers that provide public transport services can also choose to use this formula to calculate their VAT liability.

Favorable VAT treatment

The following services will be exempt from VAT payment:

- Individual transfers of copyright

- VATable services provided by disabled individuals

- Pesticide-sowing services provided by airlines

- Technology transfers, development, consulting and services provided by taxpayers engaging in the newly-included VATable services (pilot VAT payers)

- VATable services included in the contracted energy management projects, provided by eligible energy-saving service companies

- VATable services provided by Shanghai-registered offshore outsourcing enterprises (the VAT exemption will be effective between January 1, 2012 and December 31, 2013)

- Transport revenue obtained in Mainland China by Taiwanese transport companies that engage in cross-strait direct shipping businesses

- Vessel inspection services provided by the American Bureau of Shipping (ABS) within China (the VAT exemption will be effective only when the ABS stays as a non-profit organization in China and the China Classification Society enjoys the same tax-free treatment in the United States)

- VATable services provided by enterprises set up to mainly employ army dependents / demobilized soldiers / urban retired soldiers / the unemployed, or by army dependents / demobilized soldiers / urban retired soldiers / the unemployed who own individual businesses (the VAT exemption will be effective for the first three years on the entities’ establishment)

The following services will enjoy VAT refund (or partial VAT refund) upon collection:

- Domestic cargo transport, warehousing and handling services provided by Yangshan Bonded Port Zone-registered pilot VAT payers

- VATable services provided by entities that settle the disabled

- Pipeline transport services provided by pilot VAT payers

- Tangible personal property leasing services provided by the pilot VAT payers that engage in the pilot financial leasing businesses approved by People’s Bank of China, China Banking Regulatory Commission and Ministry of Commerce

Dezan Shira & Associates is a boutique professional services firm providing foreign direct investment business advisory, tax, accounting, payroll and due diligence services for multinational clients in China. The firm specializes in assisting foreign enterprises with their tax obligations. For further advice and specifics relating to these recent measures, please email china@dezshira.com, visit www.dezshira.com, or download the firm’s brochure here.

This article is also available on Dezan Shira & Associates’ online business resource library. To view the article, and other regulatory updates, please click here.

Related Reading

The China Tax Guide (Fifth Edition)

The China Tax Guide (Fifth Edition)

This popular book, fully updated with all recent tax changes and amendments, details all taxes in China affecting businesses and individuals, how to calculate the amounts due, tax registration and filing procedures, tax minimization techniques, and claiming VAT rebates. It also details good financial management techniques, handling negotiations with the tax bureau and annual audit and compliance procedures.

The Yangtze River Delta: Business Guide to the Shanghai Region (Fourth Edition)

The Yangtze River Delta: Business Guide to the Shanghai Region (Fourth Edition)

This guide takes a practical, city-focused approach, walking you through the economy of important cities in the region with a level of specificity available through few other English sources. Its pages overview the region from a business standpoint, examine the economy of the region’s provinces and prominent cities in depth, and introduce the basics of establishing a business in the region.

Shanghai City Guide

Shanghai City Guide

Asia Briefing’s City Guide on Shanghai is designed for the investor seeking a general overview on China’s most comprehensive industrial and commercial city. Due to its rapid economic growth in recent years, Shanghai is perhaps China’s most globalized city and, in addition to its role as Mainland China’s premier financial center, it is boasts an abundance of arts, culture, and cutting-edge technology.

China’s Software Developers Can Enjoy VAT Refunds

China to Commence Pilot Project for VAT Reform in Shanghai

- Previous Article China to Exempt Small Businesses From 22 Fees

- Next Article China’s Wine Market Shows Great Potential