China’s Tax Residency Certificate: Implications for DTA Benefits

(For our latest report on determining tax residency in China, dated October 1, 2018, click here.)

By Dezan Shira and Associates

Editors: Alan Hervé and Thibaut Minot

When transacting with China, a foreign company’s ability to benefit from Double Tax Agreements (DTAs) often depends on the cooperation and competency of the Chinese party to effectively complete Certificate of Tax Residency (CTR) application procedures.

Although the application process for obtaining a CTR is relatively straightforward, delays and setbacks are not uncommon. The application process is localized, yet it has cross-border implications that overseas investors should consider.

Using a concrete case study, this article demonstrates the importance of filing timely CTR applications in China and sheds light on the application process itself.

Case study

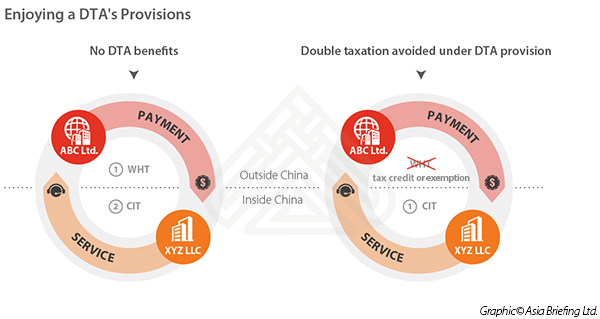

ABC Ltd. based outside of China receives consulting services from XYZ LLC based in China. According to the terms of the commercial agreement signed between the two parties, company XYZ LLC provides services in return for payment from ABC Ltd.

This cross-border transaction leads to a double taxation situation: a Withholding Tax (WHT) is levied in ABC Ltd.’s home country on the fee leaving the country, and Corporate Income Tax (CIT) has to be paid in China on the revenue generated there from the transaction.

A DTA has been signed between ABC Ltd.’s home country and China in order to avoid such double taxation situations.

According to this DTA, profits realized in China can only be taxed in China, except if the company situated in China has a permanent establishment (PE) in ABC Ltd.’s home country. If that were the case, the DTA states that the profits attributable to the PE should only be taxed in ABC Ltd.’s home country. Otherwise, when income is taxed in China, it should be exempt from tax in ABC Ltd.’s home country or a tax credit should be granted, hence effectively eliminating the double taxation.

In this scenario, assuming that XYZ LLC does not have a PE in ABC Ltd.’s home country, China should be the only contracting state able to tax the transaction. That means that ABC Ltd.’s home country should either (i) not withhold any sum; or (ii) grant a tax credit.

In practice, when a WHT is withdrawn, the taxpayer is often able to benefit from the exemption through a reimbursement if certain conditions are met. In order for ABC Ltd. to claim the tax credit (or exemption), it is required to prove to local tax authorities that relevant taxes have been paid in the other contracting state (China), hence the need to obtain a CTR from XYC LLC.

![]() RELATED: Capital Gain Tax Treatment: Taxation Under the China-Hong Kong DTA

RELATED: Capital Gain Tax Treatment: Taxation Under the China-Hong Kong DTA

Obtaining the CTR

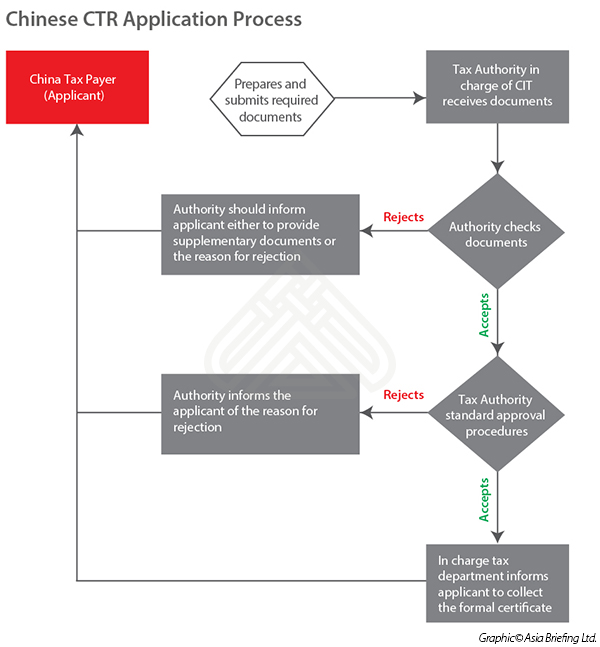

The State Administration of Taxation Circular 2016 No. 40 expressly states that a company can apply for a CTR to enjoy the benefits of a DTA, and explains the different steps of the process.

The application to obtain the CTR must be filed by the Chinese company or in its name. The application should be made directly to the ‘State tax bureau and local tax bureau of county level which govern [its] income tax for issuance’.

The local tax bureau will generally request the following supporting documents (non-exhaustive list):

- Application form (multiple copies);

- Photocopy of tax registration certificates;

- Tax receipts of CIT paid in a year (or a formal clarification if no CIT paid during the year); and,

- Contract or board resolution or payment in relation to this application.

However, the exact documents required vary from one local tax bureau to another. As such, it is important to inquire directly with the local tax bureau to confirm the documents required. Any missing document could lead to a delay in granting the CTR.

It is fundamental for the foreign company to work closely with the Chinese party in order to ensure the effective collection of the documentation given that the company needing the CTR is located abroad and some documents can only be completed or provided by the Chinese company.

The application will then go through two sets of screening procedures.

First, the Tax Authority will check the documents and will either (i) reject the application and explain the reasons; (ii) ask for additional supporting documents; or (iii) accept the application.

Then, once the Tax Authority has accepted the request, the application will be subject to the standard Tax Authority approval procedures. At this stage, the Authority can decide to either grant the certificate or reject the application and explain the reasons for this rejection.

![]() RELATED: Audit and Financial Services from Dezan Shira & Associates

RELATED: Audit and Financial Services from Dezan Shira & Associates

Circular No. 40 states that an applicant may apply for a CTR “in any calendar year in which it qualifies as a Chines tax resident”, meaning that a certificate can only be granted for a specific year.

Obtaining the certificate officially takes around 20 working days. However, in practice the application timeline may be shorter if everything runs smoothly, or longer if the applicant does not provide all the documents required or if the Tax Authority requests additional material.

Optimizing DTA benefits

As the CTR is often a mandatory document when filing for WHT exemption, an overseas company making payments into China may be subject to double taxation until it has obtained the CTR. However, CTR application must be filed in the name of the Chinese party. If it is not inclined to cooperate or is otherwise unable to effectively handle the procedures, any delays or rejections that result could mean an effective double taxation.

The CTR application timeline might also impact the overseas company’s cash flow while it is waiting for the neutralization of the double taxation. Indeed, in some instances the company may have to settle the tax bill first and then, once in possession of the Chinese CTR, claim reimbursement. In this situation, and depending on the amounts involved, the temporary tax bill could be detrimental.

Most problematic, should the Chinese party fail to provide the CTR before the application submission deadline in the home country, the overseas company could lose the withheld tax amount.

Furthermore, the wait for the CTR can interfere with routine financial reporting and tax filing in the home country of the company needing the CTR. If the overseas company has to declare its taxable income before a certain date, it can be difficult to precisely determine this amount without assurance that the CTR and subsequent tax credit will be granted.

Working with a competent advisor in China can be the key to ensuring a smooth filing of the application and a timely issuance of the CTR. Dezan Shira & Associates can help clients to obtain a CTR by providing advice to the Chinese party, communicating with the local Tax Bureau at various steps of the application, and, if required, by filing the application on the Chinese party’s behalf.

|

China Briefing is published by Asia Briefing, a subsidiary of Dezan Shira & Associates. We produce material for foreign investors throughout Asia, including ASEAN, India, Indonesia, Russia, the Silk Road, and Vietnam. For editorial matters please contact us here, and for a complimentary subscription to our products, please click here. Dezan Shira & Associates is a full service practice in China, providing business intelligence, due diligence, legal, tax, IT, HR, payroll, and advisory services throughout the China and Asian region. For assistance with China business issues or investments into China, please contact us at china@dezshira.com or visit us at www.dezshira.com

|

Dezan Shira & Associates Brochure

Dezan Shira & Associates is a pan-Asia, multi-disciplinary professional services firm, providing legal, tax and operational advisory to international corporate investors. Operational throughout China, ASEAN and India, our mission is to guide foreign companies through Asia’s complex regulatory environment and assist them with all aspects of establishing, maintaining and growing their business operations in the region. This brochure provides an overview of the services and expertise Dezan Shira & Associates can provide.

An Introduction to Doing Business in China 2017

Dezan Shira & Associates´ Silk Road and OBOR investment brochure offers an introduction to the region and an overview of the services provided by the firm. It is Dezan Shira´s mission to guide investors through the Silk Road´s complex regulatory environment and assist with all aspects of establishing, maintaining and growing business operations in the region.

New Considerations when Establishing a China WFOE in 2017

In this edition of China Briefing, we guide readers through a range of topics, from the reasons behind foreign investors’ preference for the WFOE as an investment model, to managing China’s new regulations. We discuss how economic transformations have favored the WFOE, as well as the investment model’s utility, and detail key requirements that businesspeople need to examine before initiating the WFOE setup process. We then walk investors through the WFOE establishment process, and, finally, explain the new and idiosyncratic “Actual Controlling Person” regulation.

- Previous Article China’s FIE Registration and the New Actual Controlling Person Requirement

- Next Article Shanghai Becomes First City in Mainland China to Grant Foreign Domestic Workers Residency