Comparison: Sourcing Model Options in China

Comparing the use of representative offices, service companies and trading companies to fit the needs of your China sourcing operations

By Rosario DiMaggio

Jun. 13 – Regardless of whether a foreign company is involved in manufacturing, assembling, purchasing, or designing products in China, each business will have to develop its own individual model for sourcing the necessary goods, component parts and raw materials that will determine their short or long-term success. Ultimately, businesses sourcing product from China successfully will reach a trigger point where they will need to establish a permanent entity or base full time employees in China to carry on work such as supplier searches, price negotiations, export formalities, quality control supervision, and so on. To do this, there are essentially three types of entities that foreign investors can utilize to create a sourcing platform in China:

Jun. 13 – Regardless of whether a foreign company is involved in manufacturing, assembling, purchasing, or designing products in China, each business will have to develop its own individual model for sourcing the necessary goods, component parts and raw materials that will determine their short or long-term success. Ultimately, businesses sourcing product from China successfully will reach a trigger point where they will need to establish a permanent entity or base full time employees in China to carry on work such as supplier searches, price negotiations, export formalities, quality control supervision, and so on. To do this, there are essentially three types of entities that foreign investors can utilize to create a sourcing platform in China:

- Representative Office

- Service Company

- Trading Company

Each of these sourcing platforms feature several defining characteristics that differentiate them from each other – the most suitable and cost efficient sourcing platform for an individual business will depend on its goals and scope of operations. We cover the defining characteristics of each of these sourcing platforms in the ensuing sections.

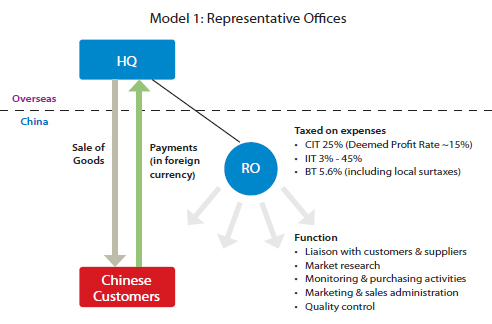

Representative Office

Representative offices (ROs) are inexpensive and easy to establish. Although China’s regulations governing such entities can seem opaque at times with regards to the permitted use of ROs, foreign headquarters typically employ them to:

- Search for new suppliers;

- Maintain relations with existing suppliers;

- Coordinate sourcing activities; and

- Help with quality control at the suppliers’ factories.

ROs have no legal status, but are an extended arm of overseas parent companies that can only interact with Chinese businesses indirectly. They do not require any capital injections, but are funded according to their needs and act as cost centers. ROs that are involved in supporting sourcing activities are usually taxed on gross expenses with the overall tax burden around 11.75 percent of total monthly expenses; however, these rates may be increased by the relevant tax bureau according to the industry. From 2010, companies that intend to register a RO must be at least two years old.

An RO will be allowed to hire only a maximum of four foreign employees. Foreign staff working for ROs should have an employment relationship with the parent company abroad, and any disputes should be settled under the laws of that country. Chinese staff working for an RO, although not limited in number, must be employed through a human resources agency that will sign a contract with the RO on the one hand and with the Chinese staff on the other to ensure social security and housing fund contributions are paid on a regular basis. The reason for restricting the right of an RO to employ staff directly is quite simple. An employee must have the right to claim against their employer, and employees cannot make claims against ROs since they are not considered capitalized legal entities in China. By forcing ROs to employ staff through agencies (which are capitalized legal entities in China), the interests of the employee are protected.

While an RO is relatively easy to establish and maintain, they often are fairly limited in terms of operational scope since they cannot actually issue invoices or sign contracts. More importantly, operating an RO can become often very costly, and that 11 percent to 12 percent tax on top of expenses can in some cases be significantly more than simply being taxed on profits as a limited liability company.

That being said, ROs are still very common for foreign companies interested in sourcing from China, and they only require a limited numbers of staff in the country to search for suppliers and conduct quality control assignments. As long as costs are kept low and the activities of the RO are within the scope of the HQ, there are probably no better alternatives to this type of entity, and many foreign businesses are using ROs to rent offices, hire local staff, and obtain working visas for their foreign employees.

Limited Liability Company

Unlike ROs, a foreign-invested limited liability company (LLC) can make profits and issue local invoices in RMB to its suppliers. Furthermore, the liabilities of the shareholders are limited by the assets they bring to the business. LLCs can also employ local staff directly, without any obligations to employ human resource services from employment agencies. Although there is no legal restriction on the number of foreigners LLCs can employ, in practice the authorities may challenge the number of foreign staff depending on the profile of the candidates, their job descriptions, and the amount of registered capital that the respective company injects.

When registering an LLC in China, a foreign investor will have to commit to invest a certain amount of capital (known as registered capital). Registered capital is the initial investment in a company that is required to fund its business operations until it is in a position to fund itself, with the absolute minimum capital requirements under Chinese law currently RMB30,000 for multiple shareholder companies and RMB100,000 for single shareholder companies. In practice, however, the official requirements for registered capital vary by industry and region, and even sometimes within districts of the same cities.

While the Chinese authorities use “minimum registered capital” as an entry barrier to ensure LLCs are of the relevant quality and financial strength, minimum registered capital is not intended to be a final ruling on how much a company needs to invest. There are financial requirements that are often overlooked when working out a company’s necessary capitalization, such as post-registration costs, customs duties (when importing), taxes, and any delays that may require additional financing. If a company runs out of cash, refinancing is a complicated procedure which, if not taken care of in the proper manner, may be regarded as taxable income.

Registered capital contributions can be made in cash or in kind, as a lump sum or in installments. The payment schedule of the registered capital needs to be specified in the company’s articles of association and feasibility study report, both of which are required documents for establishing an LLC.

For sourcing purposes, two types of LLCs are available in China:

- Service Company; and

- Trading Company.

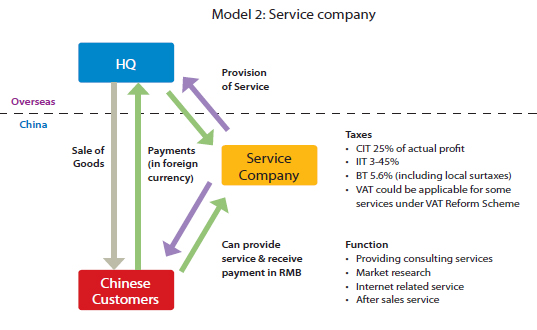

Service Company

A service company is a limited liability company that has as its core activity the provision of services to third parties. Foreign investors involved in sourcing activities use this type of company to provide market and supplier research, quality control, product development, design, and logistical support services, among others. A service company is the easiest type of limited liability company to establish, as it requires a shorter time frame to establish and a lower capital requirement compared to a trading or manufacturing company.

Foreign-invested service companies involved in sourcing activities often support their business by providing technical services and consulting services. An example would be a foreign company that provides molds and equipment to an original equipment manufacturer in China. The service company would then hire and maintain engineers, technicians, and quality control staff to assist with the technology transfer, technology consulting and technology development of related products. The service company would then be able to invoice in China or overseas for the services provided.

Please note that service companies are liable for business tax (BT) or value-added tax (VAT) depending on the service provided. In 2012, China launched a pilot program to merge BT with VAT, which is expected to be implemented nationwide starting August 1, 2013 in various service sectors, including R&D and technology services, IT services, cultural and creative services, logistics auxiliary services, and authentication and consulting services. In these sectors, 6 percent VAT is imposed in lieu of BT.

Service companies have proven to be great alternatives to ROs, especially when an RO’s operations start to grow and its costs begin to rise. Since ROs are taxed on expenses while service companies are taxed on profits, it is clear that ROs eventually reach a point where they are no longer the most cost effective option available to foreign investors. As China’s RO regulations have become stricter since 2010, many foreign companies have decided to upgrade from an RO into a service company. A basic review of expenses and available business model alternatives will highlight how this type of structural change may help reduce tax burdens, while also increasing the flexibility of its operations.

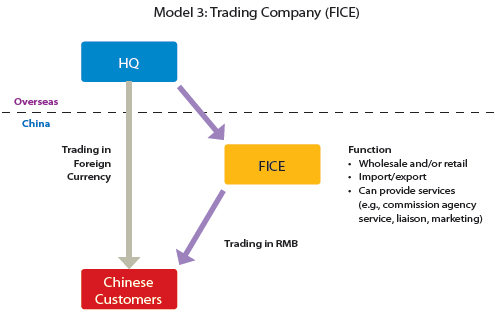

Trading Company

To engage in import and export activities as well as domestic distribution (i.e., retail, wholesale and franchising trade activities) in China, a trading company – also known as a foreign-invested commercial enterprise (FICE) – may be established. Generally, a FICE is inexpensive to establish and can be of great assistance to foreign investors by combining both sourcing and quality control activities with purchasing and export facilities, thus providing more control and quicker reaction times compared to sourcing purely while based overseas.

FICE are also the ideal choice for foreign companies that need to source in China in order to resell in China. Without a Chinese trading company, the alternative would be to buy from overseas, and have the goods shipped out of China before then reselling them back to China (which would mean additional logistical costs, customs duties and VAT).

Portions of this article came from the June 2013 issue of China Briefing Magazine titled, “Sourcing from China,” which is available as a complimentary PDF download on the Asia Briefing Bookstore until the end of this month. In this issue of China Briefing Magazine, we outline the various sourcing models available for foreign investors and discuss how to decide which structure best suits the sourcing needs of your business. Perhaps the most important factors to consider when choosing a sourcing structure are your staffing requirements, your need for operational flexibility, and which option offers the greatest cost efficiencies. We compare how each of these factors match up with the available sourcing platforms in order to help foreign businesses find the best option for their specific sourcing needs.

Portions of this article came from the June 2013 issue of China Briefing Magazine titled, “Sourcing from China,” which is available as a complimentary PDF download on the Asia Briefing Bookstore until the end of this month. In this issue of China Briefing Magazine, we outline the various sourcing models available for foreign investors and discuss how to decide which structure best suits the sourcing needs of your business. Perhaps the most important factors to consider when choosing a sourcing structure are your staffing requirements, your need for operational flexibility, and which option offers the greatest cost efficiencies. We compare how each of these factors match up with the available sourcing platforms in order to help foreign businesses find the best option for their specific sourcing needs.

Dezan Shira & Associates is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in emerging Asia. Since its establishment in 1992, the firm has grown into one of Asia’s most versatile full-service consultancies with operational offices across China, Hong Kong, India, Singapore and Vietnam as well as liaison offices in Italy and the United States.

For further details or to contact the firm, please email china@dezshira.com, visit www.dezshira.com, or download the company brochure.

You can stay up to date with the latest business and investment trends across Asia by subscribing to Asia Briefing’s complimentary update service featuring news, commentary, guides, and multimedia resources.

Related Reading

Trading With China

Trading With China

This issue of China Briefing Magazine focuses on the minutiae of trading with China – regardless of whether your business has a presence in the country or not. Of special interest to the global small and medium-sized enterprises, this issue explains in detail the myriad regulations concerning trading with the most populous nation on Earth – plus the inevitable tax, customs and administrative matters that go with this.

An Introduction to Development Zones Across Asia

An Introduction to Development Zones Across Asia

In this issue of Asia Briefing Magazine, we break down the various types of development zones available in China, India and Vietnam specifically, as well as their key characteristics and leading advantages.

Understanding Permanent Establishments in China

Understanding Permanent Establishments in China

This issue of China Briefing Magazine casts some light on permanent establishment status in China by discussing the circumstances triggering a PE in China, focusing on Service PEs. We also discuss the tax implications for a non-resident enterprise where its activities in China constitute a Service PE in the country, and address the taxation of representative offices.

Expanding Your China Business to India and Vietnam

Expanding Your China Business to India and Vietnam

This issue of Asia Briefing Magazine discusses why China is no longer the only solution for export driven businesses, and how the evolution of trade in Asia is determining that locations such as Vietnam and India represent competitive alternatives. With that in mind, we examine the common purposes as well as the pros and cons of the various market entry vehicles available for foreign investors interested in Vietnam and India.

- Previous Article China Clarifies VAT General Taxpayer Recognition Under Nationwide Reform

- Next Article China to Allow Foreign Investors to Set Up Mainland Senior Care Institutions