Exporting to China: Import Tax Slashed in Cross-Border E-Commerce Zones

By Dezan Shira & Associates

Editor: Rainy Yao

China’s 2015 total trade volume decreased by seven percent from the previous year – its first drop since 2010, according to China’s customs authorities. Imports to the country fell 13.2 percent to RMB 10.45 trillion. Boosting foreign trade has therefore become a top priority for the Chinese government in 2016. However, the Middle Kingdom also has its trump card – e-commerce. Exporters trying to sell to the lucrative Chinese market, with or without a physical presence in the country, will inevitably have heard of its booming cross-border e-commerce industry, which grew over 30 percent in 2015 despite the slowing international trade. It is predicted that trade via cross-border e-commerce alone will exceed RMB 6.5 trillion in 2016, accounting for 20 percent of total trade volume.

So how does the cross-border e-commerce model work, and what makes it different from imports under general trade? In this article, we take a closer look at China’s cross-border e-commerce industry and compare two of the most common sales approaches used by foreign merchants engaged in the industry.

![]() RELATED: Business Advisory Services from Dezan Shira & Associates

RELATED: Business Advisory Services from Dezan Shira & Associates

Cross-Border E-Commerce Comprehensive Pilot Zones

On January 15, the State Council decided to set up a new batch of cross-border e-commerce zones in 12 Chinese cities: Shanghai, Guangzhou, Tianjin, Chongqing, Hefei, Zhengzhou, Chengdu, Dalian, Ningbo, Qingdao, Shenzhen and Suzhou. The first comprehensive e-commerce pilot zone of its kind was established in Hangzhou, home to the e-commerce giant Alibaba. These zones are designated exclusively for the development of cross-border e-commerce industry, featuring a slew of preferential tax policies and streamlined customs clearance procedures. Each of these zones has an online e-commerce platform operated by state-backed or licensed companies, where Chinese customers can view and purchase foreign goods (e.g., kuajingtong in the Shanghai Free Trade Zone).

Goods sold via the online trading platforms launched by these e-commerce zones are subject to the so-called “parcel tax,” which is much lower than the normal custom duties (i.e., import tariffs, value-added tax and consumption tax if applicable). Foreign merchants operating businesses with/in the zones may choose one of the following two approaches when selling directly to Chinese consumers:

- Direct Shipping Model

Under the direct sale model, foreign manufacturers maintain warehouses in their home countries and send goods to customers after they have made orders online. Under this model, it becomes easier for the manufacturers to oversee the storage process and provide customers with a variety of products. However, it usually takes longer before the customers receive the goods as it involves a relatively more complicated customs clearance procedure.

- Bonded Warehouse Model

Under the bonded warehouse model, investors may set up a warehouse within their respective E-commerce zone. Goods will then be transported and stored temporarily within the warehouse under the Customs supervision before they are delivered to domestic customers. In this case, exporters need to determine if the quantity of their products sent to China is reasonable and can be sold within a given period.

A comparison of the two models can be found below:

Parcel Tax versus Customs Duties

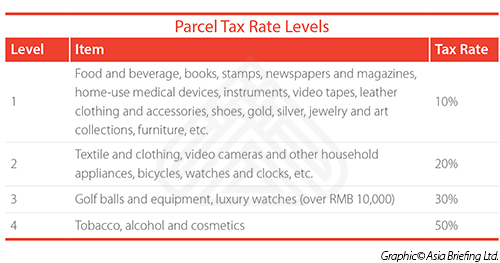

As previously mentioned, the special parcel tax implemented within pilot zones is one of the most attractive draws for investors. According to Customs Announcement [2012] No.15, the parcel tax rate can be classed into four levels depending on the categories of goods in question. It should be noted that customers don’t have to pay parcel tax when the tax amount is under RMB 50.

Calculation Method:

Tax payable= Goods price*×parcel tax rate

*Note that the China Custom released a detailed price directory for imported goods in 2012. The price of the goods that are not listed in the directory should be determined by their most recent retail price. In the case where the goods original price is twice as high as (or much lower than) it is in the directory, the exporters should provide the invoice and receipt as a proof.

Compared to the general customs duties levied on imported goods, goods imported via e-commerce zones offer an obvious price advantage as a result of tax reductions. For example, exporting UHT/fresh milk to China under the general trade model is subject to an import tariff of 15 percent and a value-added tax of 17 percent; whilst under the cross-border e-commerce model, customers will only pay 10 percent parcel tax on the imported milk. This enables foreign merchants to sell imported goods at a lower price, and thus makes their products more competitive.

24 Hours Customs Clearance

Starting May 15, 2015, China has also launched the “all year round 24 hours customs clearance” scheme for goods imported under the cross-border e-commerce model. This means the Customs clearance procedures will be finished within 24 hours once goods enter local Customs.

Development Trends

In addition to the development of China’s cross-border e-commerce industry, cooperation with local online trading platforms such as Tmall Global is no longer the only choice for foreign investors. While the combination of increased incentives and a growing number online trading platforms offers many opportunities for investment, it is important to note that China’s e-commerce sector is still at an early stage of development. This exposes potential importers to vague quality standards as well as shifting entry requirements for a number of imported products.

The current parcel tax has also led to an unfair tax burden for goods imported under the general trade model and places increasing pressure on local customs in the pilot zones. As a result, the country is now looking to raise parcel tax rates by 30 to 50 percent by this year and to expand these tax policies nationwide.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email china@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Selling, Sourcing and E-Commerce in China 2016 (First Edition)

Selling, Sourcing and E-Commerce in China 2016 (First Edition)

This guide, produced in collaboration with the experts at Dezan Shira & Associates, provides a comprehensive analysis of all these aspects of commerce in China. It discusses how foreign companies can best go about sourcing products from China; how foreign retailers can set up operations on the ground to sell directly to the country’s massive consumer class; and finally details how foreign enterprises can access China’s lucrative yet ostensibly complex e-commerce market.

Importing and Exporting in China: a Guide for Trading Companies

In this issue of China Briefing, we discuss the latest import and export trends in China, and analyze the ways in which a foreign company in China can properly prepare for the import/export process. With import taxes and duties adding a significant cost burden, we explain how this system works in China, and highlight some of the tax incentives that the Chinese government has put in place to help stimulate trade.

A Guide to China’s Free Trade Zones

A Guide to China’s Free Trade Zones

In this issue of China Briefing magazine, we examine China’s four Free Trade Zones and discuss the differences and strongpoints that exist in each of them. We begin by providing an introduction to the FTZs, and then take an in-depth look at the market access conditions, registration procedures and tax environments of each. Finally, we highlight some of the key considerations that foreign companies should be aware of when choosing an FTZ to invest in.

- Previous Article China Outbound: E-Commerce and Start-up Landscape in ASEAN and India

- Next Article Outlook on Light Manufacturing in China: February 2016