How to Close a Wholly Foreign-Owned Enterprise in China

We discuss the step-by-step procedure involved in closing a wholly foreign-owned enterprise in China, which may be subject to more compliance considerations than other business setups.

A wholly foreign-owned enterprise (WFOE) is a common investment vehicle for foreign investors wishing to operate in China’s manufacturing, trading, or service sector. This corporate structure offers foreign investors full ownership and the autonomy to own property, form legally binding contracts, recruit local staff, and invoice in RMB.

While the challenges to setting up a WFOE are well-known and discussed, what often comes as a surprise to many investors, is that a WFOE deregistration can be a much more arduous process, typically taking 12 to 14 months to complete, in contrast to three to six months needed for a WFOE setup.

This extended period of time accounts for the time that the government bureaus require to ensure that all obligations are met prior to the dissolution of the company, which includes but is not limited to the repayment of debts, payment of employee wages, and clearing outstanding tax liabilities.

A WFOE company structure will usually be subject to special attention during its closure procedure, involving more steps and authority involvement than that of its representative office and Chinese company counterparts.

For this reason, it is important for a business that has adopted such a structure to ensure the correct procedure is followed and to work closely with authorities throughout.

Still, the procedures for deregistration have been simplified considerably over the last few years. Both the Ministry of Commerce (MOFCOM) and the State Administration for Market Regulation (SAMR) have streamlined their deregistration procedures to improve the ease of doing business in China.

For example, the stringent MOFCOM approval requirements have also been replaced with a simpler record filing system and a more flexible SAMR deregistration process now exists for WFOEs who have been in operation for a short amount of time. In addition to this, businesses are now encouraged to submit information online before proceeding to the on-site submission.

While the deregistration process can vary somewhat depending on the nature of the WFOE (manufacturing, trading, or service WFOE), its associated business scope, the size and health of the company, and the duration of company operations – there are some general steps that each WFOE must follow.

For ease of understanding, the following steps offer a rough guideline to the deregistration procedure for a WFOE. For any queries related to doing business in China, please reach us at china@dezshira.com.

Closing a wholly-foreign owned enterprise in China: Step-by-step

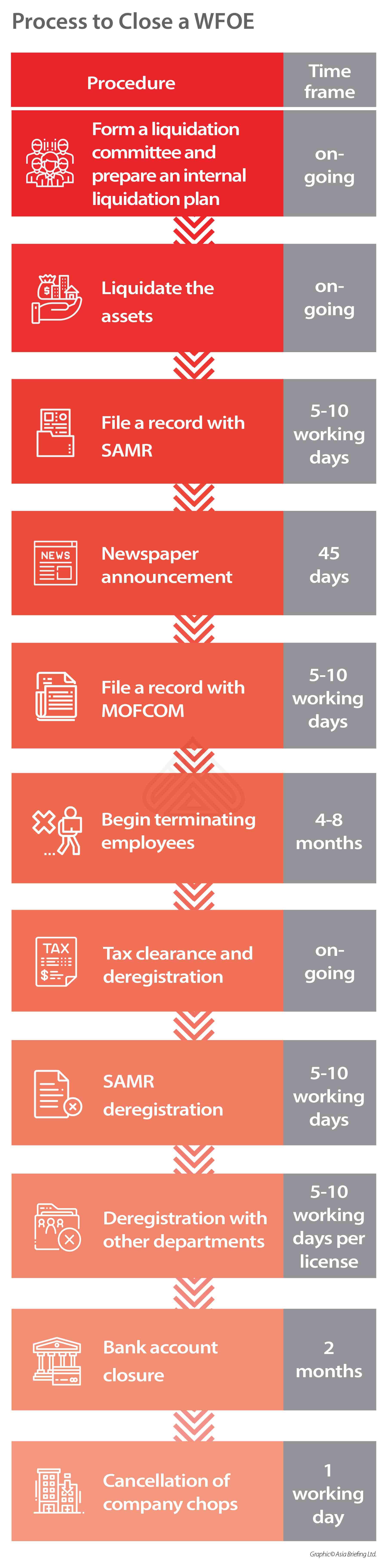

1) Form a liquidation committee and prepare an internal plan

The first step to closing the WFOE is to form a liquidation committee. By law, the liquidation committee should comprise of a legal representative, representative for the company’s creditors, government representative, as well as certified public accountants and lawyers. In practice, however, the liquidation committee generally consists of any three or more people designated by the shareholders.

At the early stages of the liquidation, the committee should formulate and implement an internal liquidation plan, which makes a note of how the termination of employees, liquidation of assets, payment to creditors, and conclusion of lease will be handled.

Throughout the liquidation process, the committee will be responsible for several matters directly concerning the deregistration process, including – notifying the creditors of the business closure, preparing the liquidation report to submit to authorities, as well as more administrative tasks, such as preparing the balance sheet and recording a detailed list of all assets and evaluating properties.

2) Liquidate the assets

At this stage, the liquidation committee should also begin liquidating the company’s assets and allocate the returns from the sale in the following order:

- Liquidation expenses;

- Outstanding employee salary or social security payments;

- Outstanding tax liabilities, and;

- Any other outstanding debts owed by the WFOE.

The company should refrain from settling creditors’ claims until the liquidation plan in step one has been made and approved by the board of shareholders. After the debts have been discharged, the liquidation committee can distribute the remaining returns among the shareholders. If the company’s assets are unable to settle the debts, it will file a bankruptcy declaration with the court.

3) File a record with SAMR

After the liquidation committee is formed, the WFOE must file a record with the SAMR notifying them of their intent to close the WFOE. This can be completed by submitting a shareholder resolution, which reflects the shareholder(s)’ decision to close the business and announces the names of the members that have been appointed to form the liquidation committee.

4) Newspaper announcement

Once the SAMR record has been filed, an announcement can be submitted in the newspaper to inform creditors of the business closure and to ask them to declare their claim. Although some cities have removed the requirement to submit a newspaper announcement for easy deregistration, proof of this announcement is still required by various authorities throughout the deregistration process, such as by MOFCOM, SAMR, and at the bank.

The announcement must be made in the provincial- or state-level newspaper and include basic details, such as the WFOE’s name, and in some provinces, committee member names. Following the announcement, a minimum of 45 days is then required before proceeding to the next step. This is to ensure adequate notice and time has been given to creditors to handle unresolved obligations and unpaid accounts.

5) File a record with MOFCOM

A shareholder resolution, which states the shareholder’s intent to close a business, also needs to be submitted to the MOFCOM. Previously, WFOES needed to obtain approval from MOFCOM before closing the entity, but now a simplified record filing system exists.

6) Begin terminating employees

Businesses are advised to begin terminating employees as early as possible as many adjoining issues may arise once this process is initiated. The WFOE should also make an assessment on their employee’s legal contracts to determine if and how much of a termination fee is owed and identify staff that need special treatment during this stage, as is the case for pregnant women, employees with work-related injury, and others. In theory, all employees can be terminated if the company decides to shut down; however, local bureaus may at times impose their own labor restrictions on companies.

Where employees are eligible for workplace injury compensation, the business will be required to wait for all the injury assessments to have been completed by the HR bureau before closing down. This may take a long time because the assessment needs to be completed after the injury has been stabilized in order to exact the compensation amount owed to the employee. The company should also ensure that employees in key positions return property, such as company chops, financial statements, financial books, key passwords, and working computers before they depart.

7) Tax clearance and deregistration

A simplified tax deregistration now exists for eligible taxpayers. However, a general tax deregistration process will usually take around four to eight months. During this process, the tax authority will collect a series of relevant documents including, but not limited to, the signed board resolution, evidence of lease termination, and tax filing records for the previous three years. At this point, all outstanding tax liabilities will be identified and required to be settled before deregistering the business from its value-added tax (VAT) corporate income tax, individual income tax and stamp duty obligations.

Businesses that have been operating for more than one year will then be required to complete an audit with a local certified public accountant (CPA) firm to obtain a liquidation report. This liquidation report, along with the unissued invoices, VAT invoices, and equipment, can then be brought to the tax bureau for review. In some instances, the tax bureau may visit the office in person to learn more of the company’s intentions and reasons.

If the review is successful, the tax clearance certificate will be issued, in which case the business will have successfully deregistered from all its tax obligations. It is important to note that the business will incur ongoing tax liabilities throughout the business closure process.

8) SAMR deregistration

Once the official tax clearance certificate has been obtained, the SAMR deregistration processes can begin. To do this, the liquidation committee must submit the liquidation report, signed by the committee members, as well as a shareholder’s resolution report, which needs to confirm the following – the amount of money that is left in the company, the completion of tax clearances, the termination of all employees, and that all creditor claims have been settled.

Once this step has been completed and the SAMR deregistration notice has been obtained, the WFOE will be deemed to be legally deregistered and will no longer exist as a legal entity.

9) Deregister with other departments

At the same time, the business must deregister at the following departments (where relevant):

- State Administration of Foreign Exchange (SAFE): This needs to be completed through the bank rather than SAFE. The entity must make an application at the bank in which their RMB basic account was opened.

- Social Insurance Bureau: The SAMR deregistration notice needs to be brought to the HR bureau for deregistration.

- Customs Bureau: An application letter signed by the legal representative and stamped by the company, along with other original certificates needs to be submitted to the customs bureau for deregistration.

- Other licenses: Production licenses, food distribution licenses, and systems, applications and products (SAP) deregistration (for trading companies with their own website), and others need to be deregistered with the relevant authorities.

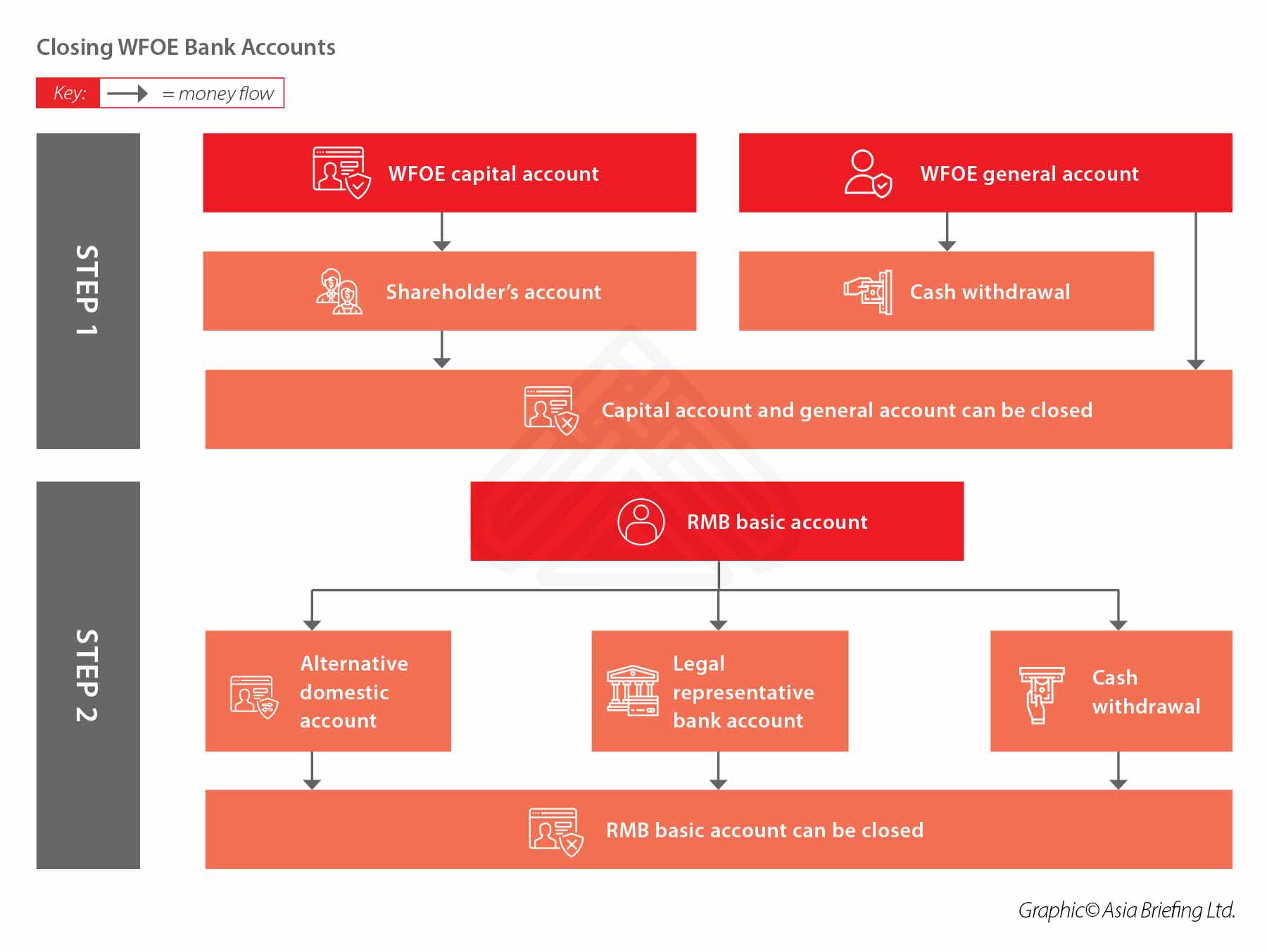

10) Bank account closure

Most WFOES will have at least three different company bank accounts, each of which must be closed before the account can be properly shut down. The capital and general account will typically be the first accounts to be closed. The remaining balance of the capital account can be transferred directly to the shareholder’s bank account, whereas the remaining balance of the general account can be transferred to the RMB basic account or the cash amount can be withdrawn.

The RMB basic account must always be the final account to close as it is the WFOE’s primary account and is most closely monitored by China. Here, there are several options – the balance can be directly transferred to a legal representative, directly transferred to another domestic account, or the cash amount can be withdrawn.

However, these rules may be subject to changes since the new Foreign Investment Law has come into effect. And, individual bank branches may have their own policies.

11) Cancel company chops

Once all the other steps are completed, the company can cancel the company chops with the public security bureau, if needed. This must be the very last process as many of the previous deregistration steps will require the company chops.

Practical advice for closing a WFOE

Practical advice for closing a WFOE

Closing a business requires a holistic view of every aspect of the business – whether it be HR, tax, legal, accounting, IT, logistics, or stock and inventory. Many of these issues are intensified when a company is inactive or there has been insufficient preparation. As Betty Zhang, Senior Associate at Dezan Shira & Associates, explained, “some of the most complicated WFOE closure cases involves companies that have been placed on the SAMR abnormal list for non-activity.”

According to Zhang, “appearing on such a list not only significantly delays the closure process (as the business will need to apply to be removed from the abnormal list) but will also mean that the WFOE is ineligible for the simplified deregistration process.”

A considerable amount of time can also be expendable on reissuing company chops, reactivating businesses licenses, ensuring the authorizing legal representative is still available, and resetting passwords and bank signatures, where necessary. “This is not to mention the problems that come with unfulfilled financial reporting and tax declaration obligations,” Zhang added.

However, even for active and healthy companies, certain procedure likes capital remittance will be a complicated procedure, requiring special planning at an early stage. Zhang advises shareholders of a company to make a money transfer plan as the liquidation committee forms, or even before. Further to this, the bulk of the transferring should be completed before the SAMR deregistration step, which dissolves the legal entity, and will make capital remittance significantly harder to do.

Therefore, when an investor decides to close a WFOE, making a plan is essential to staying ahead at each stage of the closure process, and can mean avoiding lengthy delays, added costs, and serious consequences. Businesses should ensure they retain an experienced local advisor to avoid some of these common challenges and pitfalls.

This article has been adapted from the December 2019 China Briefing Magazine issue, titled “How to Close a Business in China“. For any queries related to doing business in China, please reach us at china@dezshira.com.

About Us

China Briefing is written and produced by Dezan Shira & Associates. The practice assists foreign investors into China and has done so since 1992 through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Dongguan, Zhongshan, Shenzhen, and Hong Kong. Please contact the firm for assistance in China at china@dezshira.com.

We also maintain offices assisting foreign investors in Vietnam, Indonesia, Singapore, The Philippines, Malaysia, Thailand, United States, and Italy, in addition to our practices in India and Russia and our trade research facilities along the Belt & Road Initiative.

- Previous Article How to Close a Business in China: Common Questions Asked

- Next Article An Introduction to China’s Cross-Border E-Commerce Pilot Zones and Pilot Cities