How to Conduct Business in China Without Paying Tax

Double tax treaties are a starting point for understanding your position

By Chris Devonshire-Ellis, Dezan Shira & Associates

Jul. 19 – Many international corporations successfully trade and effectively ‘do business’ with China without the need to establish a permanent presence in the country. However, there remains a number of issues to be aware of to make sure that firstly, you don’t cross the barrier into “illegally” operating, and secondly, when the right time arises to consider an investment into the country in terms of funding an office.

Jul. 19 – Many international corporations successfully trade and effectively ‘do business’ with China without the need to establish a permanent presence in the country. However, there remains a number of issues to be aware of to make sure that firstly, you don’t cross the barrier into “illegally” operating, and secondly, when the right time arises to consider an investment into the country in terms of funding an office.

One of the key aspects to be aware of is whether or not your home country has a double tax avoidance agreement (DTA or DTAA) with China. Much of the legalese concerning the treatment of conducting business with China, and the parameters that this includes, can be found within these documents. Key to these are the concepts of “Residency”, “Permanent Establishment” and “Business Profits,” and how such treaties determine these issues.

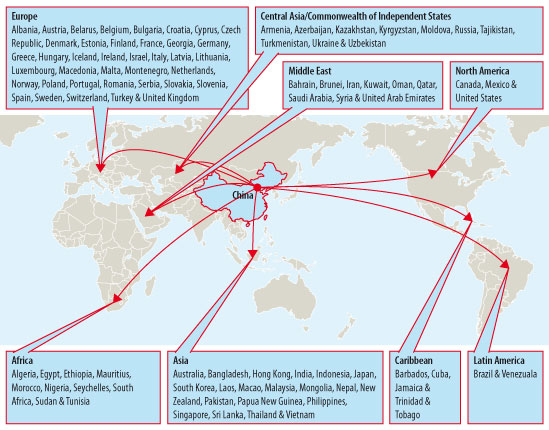

Firstly though, let’s examine the countries that currently have a DTA with China:

This is an impressive list. Tax treaties as documents are of a bilateral nature, and while DTA signing countries are not all members of the Organization for Economic Cooperation and Development (OECD), DTAs are mainly based upon the model conventions developed by this body. While about 75 percent of the actual text in any DTA is identical with the text in any other DTA, the applicability and specific provisions of each treaty can vary considerably. This is why, when conducting any business with China, it is a good idea to check out the bilateral provisions your country may enjoy with the PRC.

The Status of Hong Kong

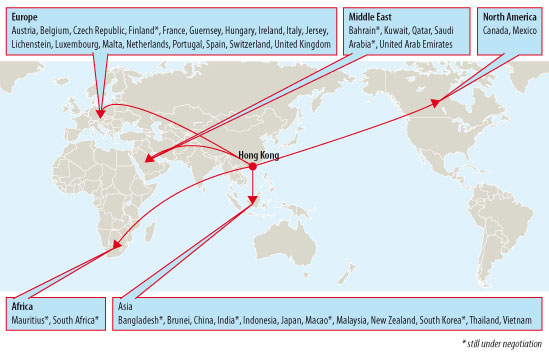

It should be noted that Hong Kong has also concluded tax treaties with other countries apart from Mainland China. Hong Kong adopts the territoriality basis of taxation, whereby only income/profit sourced in Hong Kong is subject to tax. Therefore, Hong Kong residents generally do not suffer from double taxation.

Many countries which tax their residents on a worldwide basis also provide their residents operating businesses in Hong Kong with unilateral tax credit relief for any Hong Kong tax paid on income/profit derived from Hong Kong. Hong Kong allows a deduction for foreign tax paid on turnover basis in respect of an income which is also subject to tax in Hong Kong. Businesses operating in Hong Kong therefore do not generally have problems with the double taxation of income.

Hong Kong’s relationship with Mainland China under the terms of the Hong Kong-China DTA provides tax relief, for example, on payment of dividends, which is usually subject to 10 percent remittance tax in China – this can be reduced to 5 percent if the recipient company is based in Hong Kong.

However, to promote trade with its traditional partners, Hong Kong has engaged in its own DTAs, almost all concentrating on the banking, logistics and aviation industries, as follows:

Understanding DTAs and Using Them To Evaluate Your Tax Position

To provide some guidelines on the subject, interested readers may view, as an example, the China-Luxembourg DTA here. Of particular note, typically included in all DTAs involving China, are articles four (Residency), five (Permanent Establishment) and seven (Business Profits).

Residency

The Residency article in DTAs provide `tie-breaker’ rules for determining, for the purposes of the agreement, where an individual is resident in both countries under their respective domestic laws. The `tie-breaker’ rules consist of a series of tests to be applied successively until residence for the purposes of the agreement is allocated to one State or the other. In other words, once a test is conclusive it is unnecessary to apply subsequent tests. As with all double taxation matters, it is essential to look at the text of the particular agreement in point.

Generally the tests appear in the following order:

- Permanent home: An individual is a resident of the State in which they have a permanent home available to them (though not necessarily owned by them). If they have a permanent home available to them in both States it is necessary to look at the next test.

- Centre of vital interests: An individual is a resident of the State to which their ‘personal and economic relations’ (a wide expression intended to cover the full range of social, domestic, financial, political and cultural links and relationships) are closer. If it is not possible to determine this, or if they have no permanent home available in either State, then it is necessary to look at the next test.

- Habitual abode: An individual is a resident of the State in which they have their habitual abode. If they have a habitual abode in both States or in neither, then it is necessary to look at the final test.

- Nationality: An individual is a resident of the State of which they are a national.

Understanding this article is key when establishing whether or not your company is hiring personnel whose residency can be construed as being in China. If so, this can trigger permanent establishment (PE) status and exposure to income tax in China (even if your corporation is physically based externally from the country).

We discuss these HR issues and the hiring of “independent contractors” in China in the following article: “Independent Contractors in China and Available Alternative Options.” Under certain circumstances it is possible to engage staff in China without having them individually either on your books or as an employee.

Permanent Establishment

The article concerning PE is of the utmost importance when considering the tax implications of your business relationship with China. It is perhaps the most important application of a DTA relating to companies and other enterprises trading with China. Virtually all double taxation treaties cut down a country’s right to tax profits of a foreign company or enterprise by providing that the profits derived in one country will not be subject to tax in the other country unless the business is carried on through a PE.

Additionally, where business is carried on in the other contracting country through a PE, only business profits actually attributable to the PE may be taxed. This prevents the mere presence of a PE giving rise to tax liabilities on unrelated income.

A vital concern in this case is what is meant by a PE for the purposes of the treaty. This is normally defined in some detail in one of the articles of the treaty. The primary definition of a permanent establishment is typically a ‘fixed place of business through which the business of an enterprise is wholly or partly carried on.’ The definition will then normally go on specifically to include: a place of management; a branch; an office; a factory; a workshop; and a mine, oil or gas well, quarry or other place of extraction of natural resources.

Other activities specifically deemed to represent a PE are a building or construction site, or an installation project existing for more than twelve months, and a person who has and habitually exercises an authority to conclude contracts on behalf of the enterprise.

More importantly for a company seeking to avoid taxation in a foreign country, the definition of a PE usually excludes certain activities even if conducted through a fixed place of business. These often include facilities used by the enterprise solely for storage, display or delivery of goods, the maintenance of stocks for storage, display, delivery or for processing by another enterprise, or for purchasing an office.

A combination of the activities will similarly be excluded provided the overall activity is of a preparatory or auxiliary character. Another exclusion from the definition of a PE is a broker, general commission agent, or other independent agent acting in the ordinary course of their business. However, reference to the particular treaty in question should be taken.

Business Profits

Many tax systems provide for collection of tax from non-residents by requiring payers of certain types of income to withhold tax from the payment and to remit it to the government. This includes China, which has a fairly complex system of withholding tax rates depending upon the type of service. Such income often includes interest, dividends, royalties, and payments for technical assistance.

Most tax treaties reduce or eliminate the amount of tax required to be withheld with respect to residents of a treaty country, and this includes those with China. In this manner, business profits can be increased by invoking the relevant treaty clause and reducing the amount of withholding tax payable in China. This can have a significant impact on the total tax burden.

This is true, for example, in the UK-China DTA, amended in 2011, where the changes mean that withholding tax on repatriated dividends are cut in half from 10 percent to 5 percent in shareholdings of 25 percent or higher in a Chinese company (a definition that includes foreign-invested commercial enterprises, wholly foreign-owned enterprises and joint ventures). As profits in China are now significant for many multinational corporations, such treaty applications can mean potential savings of millions of RMB in profit that would otherwise be payable in tax.

Eliminating Import Duties

China has signed a free trade agreement (FTA) with ASEAN, which includes their next door neighbor Vietnam in addition to Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore and Thailand. This agreement covers thousands of products allowing for their importation from any of these countries into China at zero or substantially reduced rates. The full extent of these treaties, updated amendments and the products covered can be found on our ASEAN Briefing website here.

This FTA now means that the cheaper labor rates in some of the ASEAN nations can justify the basing of production facilities in countries such as Vietnam to be used as a supply base for the China market. This is highly pertinent given that China’s labor costs are significantly increasing. The ASEAN-China FTA is having the effect of pushing labor intensive manufacturing to ASEAN nations, while at the same time avoiding any duty penalty in doing so.

In addition to the ASEAN FTA, China is also in negotiations with Australia, India, Japan and New Zealand (together with ASEAN) over forming a free trade area known as the Regional Comprehensive Economic Partnership (RCEP). This agreement is still being brokered, however, it was endorsed by ASEAN eight months ago. When enacted, it will reduce or eliminate import duties into China once again on thousands of products from each of these countries. As a result, intra-Asian trade flows are expected to double by 2020 and underpin what will be the world’s fastest growing trade and economic bloc – Asia, including China and India.

Beyond DTAs and Towards Free Trade

Of note is that China is currently going through a process of upgrading many of its DTAs – both the Netherlands and Qatar have expanded their treaties with China and Hong Kong recently, while Switzerland has recently signed a memorandum of understanding concerning a complete FTA with China – the first country in the European Union to do so. If ratified, the FTA will reduce tariffs to zero on 84.2 percent of imports from Switzerland and, in return, Switzerland will offer zero tariffs for 99.7 percent of China’s exports.

This path appears to be the way forward for China in dealing with a slowing global economy – trade boosts will come from its DTAs with other nations, and it will pay to keep track of these developments as they arise. We feature updates on China’s DTA and their associated developments regularly on China Briefing. A complimentary subscription to these updates can be obtained by completing our subscriber form here.

Summary

While one may not completely alleviate the necessity of paying tax in China, it can certainly be minimized. Double taxation treaties create the opportunity for companies to trade abroad without incurring foreign taxation if they can carefully structure their activities in China such that they do not represent a permanent establishment in accordance with the terms of the applicable DTA. Under certain conditions, DTAs can allow business to be conducted with China, including that of permanent trade, without the need to pay tax, yet armed with the benefits of both on-the-ground personnel and an office.

Many companies whose home nations are signatories to DTAs that China has in place are unaware of the benefits they can bring. They are also non-specific – meaning DTAs apply to small and medium-sized enterprises as well as multinational corporations. It is time to evaluate your DTA with China, be aware of its contents, and to utilize it in a way in which they were intended – to boost trade with China by reducing or eliminating tax.

Chris Devonshire-Ellis is the Founding Partner of Dezan Shira & Associates. The firm was established in China in 1992 and has now developed into a national practice with twelve offices throughout the country, advising international corporations on business advisory services, legal establishment issues, tax liabilities, in addition to corporate structuring, compliance and on-going accounting, payroll and related matters. To contact the firm, please email china@dezshira.com or visit www.dezshira.com.

The practice also has offices in Hong Kong, India, Singapore and Vietnam. Please email asia@dezshira.com for assistance in these markets.

You can stay up to date with the latest business and investment trends across China by subscribing to Asia Briefing’s complimentary update service featuring news, commentary, guides, and multimedia resources.

Related Reading

The China Tax Guide: Tax, Accounting and Audit (Sixth Edition)

The China Tax Guide: Tax, Accounting and Audit (Sixth Edition)

This edition of the China Tax Guide, updated for 2013, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in China, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in China in order to effectively manage and strategically plan their China operations.

Understanding Permanent Establishments in China

Understanding Permanent Establishments in China

This issue of China Briefing Magazine casts some light on permanent establishment status in China by discussing the circumstances triggering a PE in China, focusing on Service PEs. We also discuss the tax implications for a non-resident enterprise where its activities in China constitute a Service PE in the country, and address the taxation of representative offices.

Trading With China

Trading With China

This issue of China Briefing Magazine focuses on the minutiae of trading with China – regardless of whether your business has a presence in the country or not. Of special interest to the global small and medium-sized enterprises, this issue explains in detail the myriad regulations concerning trading with the most populous nation on Earth – plus the inevitable tax, customs and administrative matters that go with this.

Independent Contractors in China and Available Alternative Options

Double Taxation Agreements and Your China Investment Strategy

- Previous Article PBOC Simplifies Cross-Border RMB Transactions

- Next Article China Liberalizes Bank Lending Rates