An Introduction to Double Taxation Avoidance in China

By Chris Devonshire-Ellis, Zhou Qian and Matthew Zito

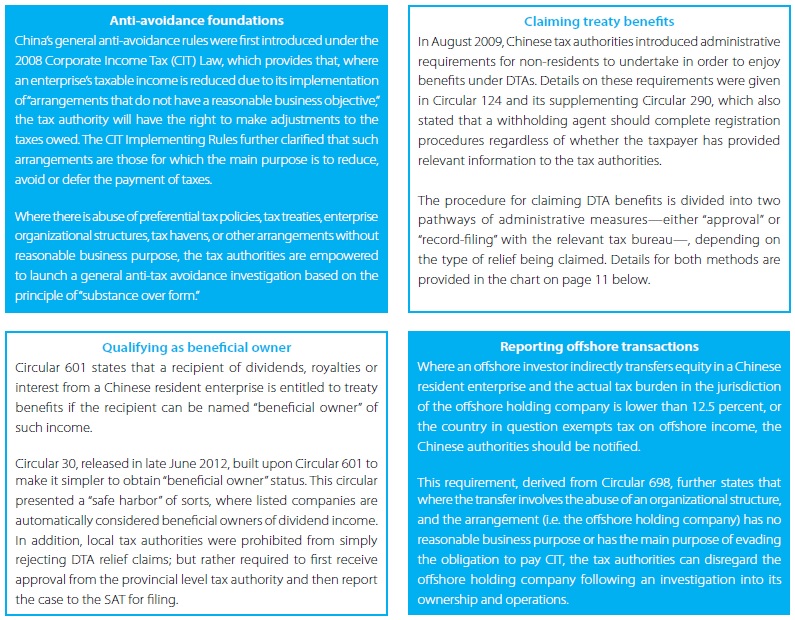

China has made significant strides in the past five years in building up its regulation in the area of double taxation avoidance, as well as implementation assurance techniques. Following the 2008 Corporate Income Tax Law, which laid the basis for anti-avoidance in China, the State Administration of Taxation (SAT) issued a flurry of related circulars stipulating reporting requirements for offshore transactions, describing qualification as a beneficial owner, and dictating protocol for claiming treaty benefits.

China has made significant strides in the past five years in building up its regulation in the area of double taxation avoidance, as well as implementation assurance techniques. Following the 2008 Corporate Income Tax Law, which laid the basis for anti-avoidance in China, the State Administration of Taxation (SAT) issued a flurry of related circulars stipulating reporting requirements for offshore transactions, describing qualification as a beneficial owner, and dictating protocol for claiming treaty benefits.

Before it will grant DTA relief from Withholding Tax on dividends, interest or royalties, the SAT must be satisfied that the applicant company in a DTA partner jurisdiction (for example, Hong Kong or Singapore) is indeed the “beneficial owner” of the Chinese subsidiary. The SAT bases its judgment on a principle of “substance over form” – that is, it is not enough that the applicant company is a tax resident in the DTA partner jurisdiction in question.

This can pose a significant problem, especially for companies that were established many years ago through a holding company in Hong Kong, and thus did not consider their future qualification as “beneficial owners.” Therefore, conducting a preliminary assessment of a company’s situation is typically the first step taken by Dezan Shira and Associates professionals to determine the likelihood of approval prior to submitting an application for DTA relief.

Based on the experience of Dezan Shira & Associates professionals, the most common difficulty that clients in Hong Kong face in securing treaty benefits under the DTA between China and Hong Kong is obtaining the tax residency certificate for their Hong Kong entity, especially when this acts solely as a holding company. In such cases, the China tax authority is likely to refuse to recognize these entities as a beneficial owner and deny the application for DTA benefits.

The development and current situation of DTAs in China can be summarized according to four legal frameworks:

Apart from their nominal function of protecting against double taxation, most DTAs also include “tax sweeteners” for savvy international businesses to take advantage of, such as the following:

Dividends Tax

China charges a 10 percent dividends tax on the overseas repatriation of profits, in addition to a 25 percent corporate income tax (CIT). However, many of China’s bilateral DTAs (such as that with Hong Kong) provide for a clause that reduces the dividends tax rate by 50 percent. This potential reduction, entailing considerable savings for enterprises, is not something that the taxation authorities will bring to the attention of taxpayers. In order to secure these savings, it is essential that investors plan far in advance, as applying for DTA benefits is just one step in the larger procedure of declaring and repatriating dividends (as shown).

For example, a WFOE with an accumulated profit of RMB200,000 in 2014, after placing a mandatory 10 percent (i.e. RMB20,000) into its reserve funds and paying 10 percent withholding CIT (RMB18,000) on the remainder, will only be able to repatriate RMB162,000 for the year. But under the DTA reduced rate of 5 percent CIT, this amount increases to RMB171,000.

![]() RELATED: How to Remit Profits as Dividends

RELATED: How to Remit Profits as Dividends

Withholding Tax

Withholding Tax (WT) is charged on an array of service fees billed by a company in its home jurisdiction to a company (either a client or subsidiary) in China for services provided by the former to the latter. As CIT cannot be charged to a company that is non-resident, WT takes its place. The levied rate of WT varies considerably depending upon the service provided.

Foreign investors are advised to consult with professionals as to the applicable WT rates per type of service. However, as a rule of thumb, this is generally between 10-20 percent of the total invoice value. In many cases, the DTA mechanism can halve this amount. Service fees charged by a parent company for the use of trademarks by its subsidiaries, for example, may be remitted to the parent at a rate lower than the standard 10 percent Withholding Tax levied in China.

While foreign-invested entities (FIEs) in China are permitted to sign a variety of service agreements with foreign companies, including with their headquarters (HQ), these agreements can sometimes be looked upon with suspicion as “constructed channels” for funneling money between the HQ and its overseas subsidiaries.

![]() RELATED: Remitting Royalties from China: Procedures and Requirements

RELATED: Remitting Royalties from China: Procedures and Requirements

It is important to bring one’s intent to invoke DTA benefits to the attention of the local tax office in China, together with copies of the DTA (in Chinese), and the company’s articles of association and business license. Permission is required by tax officials in China to reduce the amount of taxes due from a company and they must be able to provide an explanation to their own superiors.

Accordingly, a well presented case must be made by the applicant, for which it is advisable to contract the assistance of a professional firm such as Dezan Shira & Associates. The tax savings thus obtained typically outweigh any service fees incurred even in year-one of operations under the protection of a DTA.

This article is an excerpt from the October issue of China Briefing Magazine, titled “Double Taxation Avoidance in China: A Business Intelligence Primer.” In our twenty-two years of experience in facilitating foreign investment into Asia, Dezan Shira & Associates has witnessed first-hand the development of China’s double taxation avoidance mechanism and established an extensive library of resources for helping foreign investors obtain DTA benefits. In this issue of China Briefing Magazine, we are proud to present the distillation of this knowledge in the form of a business intelligence primer to DTAs in China. |

![]()

Strategies for Repatriating Profits from China

Strategies for Repatriating Profits from China

In this issue of China Briefing, we guide you through the different channels for repatriating profits, including via intercompany expenses (i.e., charging service fees and royalties to the Chinese subsidiary) and loans. We also cover the requirements and procedures for repatriating dividends, as well as how to take advantage of lowered tax rates under double tax avoidance treaties.

Annual Audit and Compliance in China

Annual Audit and Compliance in China

In this issue of China Briefing, we discuss annual compliance requirements for foreign-invested enterprises, including wholly-foreign owned enterprises, joint ventures and foreign-invested commercial enterprises, as well as the less demanding requirements for representative offices. We also highlight the most recent tax and legal changes that will significantly influence the way companies do business in China in 2014.

Adapting Your China WFOE to Service China’s Consumers

Adapting Your China WFOE to Service China’s Consumers

In this issue of China Briefing Magazine, we look at the challenges posed to manufacturers amidst China’s rising labor costs and stricter environmental regulations. Manufacturing WFOEs in China should adapt by expanding their business scope to include distribution and determine suitable supply chain solutions. In this regard, we will take a look at the opportunities in China’s domestic consumer market and forecast the sectors that are set to boom in the coming years.

- Previous Article China Regulatory Brief: Injury Insurance in Guangzhou, Annual Inspections in Dongguan and Container Export Refunds

- Next Article China erweitert Pilotprogramm zur Ausfuhrsteuerrückerstattung