Qualifying for DTA Benefits in China

By Eunice Ku, Zhou Qian and Matthew Zito

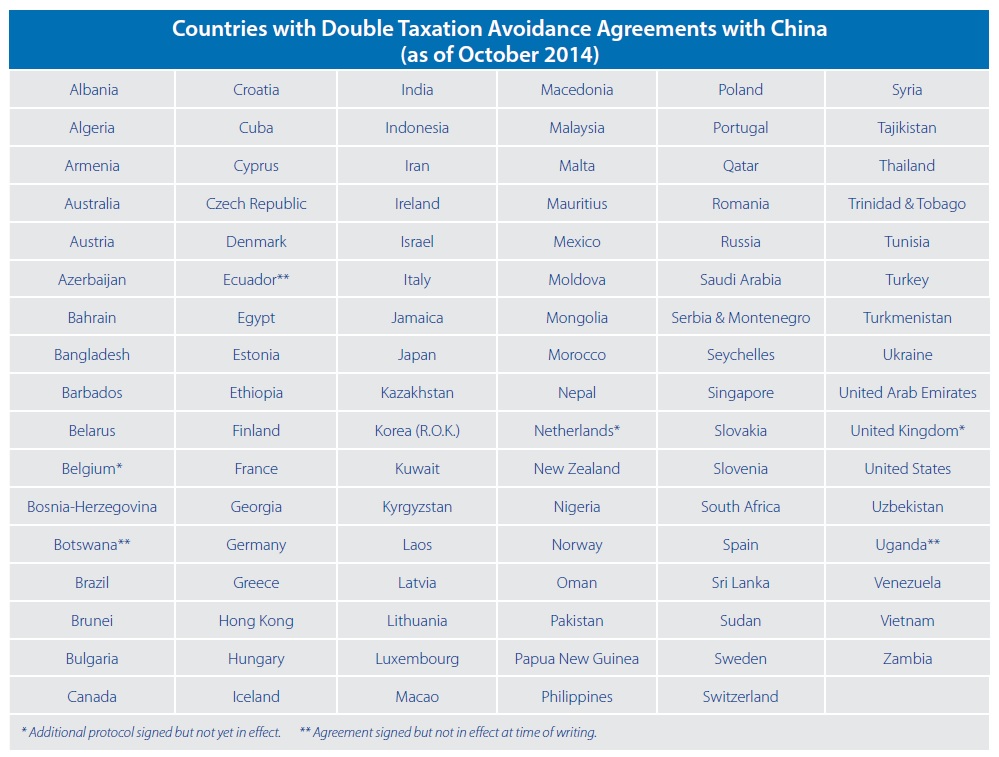

China has made great strides in the past five years in building up its regulation in the area of double taxation avoidance, as well as implementation assurance techniques, but qualifying for DTA benefits remains a complex procedure.The first step is to determine whether you are a tax resident of a country that has an effective DTA agreement with China (i.e. a non-resident with respect to China). For a list of relevant countries, see below.

Following this, the qualification requirements as set out in the specific DTA should be examined. These are typically organized in terms of the following:

Following this, the qualification requirements as set out in the specific DTA should be examined. These are typically organized in terms of the following:

- Persons covered;

- Taxes covered;

- Definitions of key terms (e.g. resident, permanent establishment);

- Taxation of income;

- Taxation of capital;

- Elimination of double taxation; and

- Exchange of information.

Accordingly, the DTA applicant must be a person covered by the DTA; the benefits to be claimed must be a tax exemption or reduction stipulated by the DTA; and other relative details in the DTA must be satisfied for a positive ruling to be issued on the application of treaty benefits. Among these criteria, permanent establishment and beneficial owner status are of critical importance for understanding the workings of DTAs and are treated at length below, accordingly.

Special Purpose Vehicles

Prior to 2008, a special purpose vehicle (SPV) was the most common structure used by foreign companies to hold investments in China. An SPV is a holding company set up by a foreign investor outside of China — usually in Hong Kong or other locations that boast notable tax advantages and favorable tax treaties with China — for the special purpose of holding equity interest in an onshore foreign-invested enterprise (FIE).

One of the advantages of using an SPV is that it may benefit from preferential withholding tax rates on dividends and other passive income under the tax treaties between China and the jurisdiction in which the SPV is located. For example, Hong Kong’s double tax agreement (DTA) with China reduces the withholding tax rate on dividends from 10 percent to five percent.

![]() RELATED: An Introduction to Double Taxation Avoidance in China

RELATED: An Introduction to Double Taxation Avoidance in China

Permanent Establishment

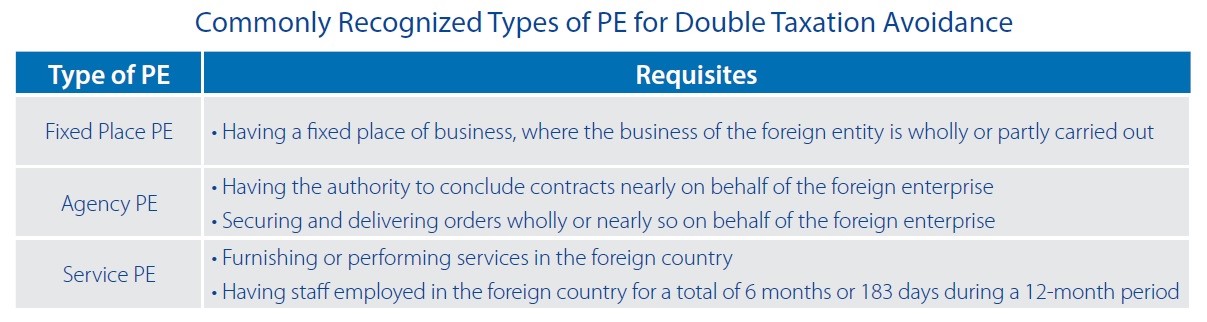

Permanent establishment (“PE”) – defined as a fixed place at which the business of an enterprise is carried out in a given country – is a key concept for the applicability of DTAs. If a non-resident enterprise (in terms of China) is a tax resident of a jurisdiction that has a DTA in place with China, it may be able to claim exemption from CIT if its establishment or venue in China does not constitute a “PE” pursuant to the “PE” article under the relevant DTA.

However, where a resident of a country which has a DTA with China carries on business in China through a PE, the profits derived by the PE will be subject to taxes in China. Simply put, foreign companies can be deemed to have a PE in China, if:

- It has an establishment or a place of business in China (Fixed place PE);

- It has a building site, a construction, assembly or installation project or related supervisory activities that last for a certain period of time (Construction PE);

- It appoints an agent in China to conclude contracts or accept orders in China (Agent PE);

- It has employees working in China for a certain period of time (Service PE).

Besides the qualification requirements contained in DTA agreements, there are also requirements stipulated by Chinese laws and regulations, clarifying whether a specific type of business can enjoy DTA benefits or not, such as “beneficial owner” status regulated by Circular 601 and Circular 30.

Beneficial Ownership

Circular 601 states that a recipient of dividends, royalties and interest from a Chinese resident enterprise is entitled to treaty benefits if the recipient can be named “beneficial owner” of such income. A “beneficial owner” refers to an individual, a company or any other group having the ownership and right of control over the income or the right or property derived from the income. In determining whether the non-resident company is indeed the beneficial owner of the royalties, the tax authorities will apply a “substance over form” principle. A “beneficial owner” should be engaged in actual operating activities. An agent or a conduit company does not constitute a “beneficial owner”.

In general, the following seven factors are disfavorable to an applicant’s determination as beneficial owner:

- The applicant is obligated to pay or distribute all or the majority of its income (e.g., 60 percent and above) to residents of a third country (region) within a stipulated period (e.g., within 12 months from receipt of income);

- Except for holding properties or rights from which income is derived, the applicant has little or no other business activities;

- Where the applicant is a corporation, its assets, scale of operations, and staffing are relatively small (or few) and not commensurate with the amount of income;

- The applicant has little or no control or right of disposal over income or properties or rights from which income is derived, and bears little or no risk;

- The counterparty country (region) of the tax agreement does not levy tax or exempts tax on the relevant income, or the actual levy rate is very low;

- Aside from loan contracts upon which interest is derived and paid, there exist other loan or deposit contracts between the creditor and a third party which are similar in terms of amount, interest rate and date of execution, etc.;

- Aside from contracts for the transfer of copyrights, patents, proprietary technologies and other use rights based upon which royalties are derived and paid, there exist contracts between the applicant and a third party pertaining to the transfer of copyrights, patents, proprietary technologies and other usage rights or ownership.)

This article is an excerpt from the October issue of China Briefing Magazine, titled “Double Taxation Avoidance in China: A Business Intelligence Primer.” In our twenty-two years of experience in facilitating foreign investment into Asia, Dezan Shira & Associates has witnessed first-hand the development of China’s double taxation avoidance mechanism and established an extensive library of resources for helping foreign investors obtain DTA benefits. In this issue of China Briefing Magazine, we are proud to present the distillation of this knowledge in the form of a business intelligence primer to DTAs in China. |

![]()

Strategies for Repatriating Profits from China

Strategies for Repatriating Profits from China

In this issue of China Briefing, we guide you through the different channels for repatriating profits, including via intercompany expenses (i.e., charging service fees and royalties to the Chinese subsidiary) and loans. We also cover the requirements and procedures for repatriating dividends, as well as how to take advantage of lowered tax rates under double tax avoidance treaties.

Annual Audit and Compliance in China

Annual Audit and Compliance in China

In this issue of China Briefing, we discuss annual compliance requirements for foreign-invested enterprises, including wholly-foreign owned enterprises, joint ventures and foreign-invested commercial enterprises, as well as the less demanding requirements for representative offices. We also highlight the most recent tax and legal changes that will significantly influence the way companies do business in China in 2014.

Adapting Your China WFOE to Service China’s Consumers

Adapting Your China WFOE to Service China’s Consumers

In this issue of China Briefing Magazine, we look at the challenges posed to manufacturers amidst China’s rising labor costs and stricter environmental regulations. Manufacturing WFOEs in China should adapt by expanding their business scope to include distribution and determine suitable supply chain solutions. In this regard, we will take a look at the opportunities in China’s domestic consumer market and forecast the sectors that are set to boom in the coming years.

- Previous Article Breaking Up is Hard To Do: Terminating an Employee in China (Part 2)

- Next Article With Revised Guidance Catalogue, China Introduces Sweeping FDI Reforms