Reduce U.S. Federal Income Taxes on Export Profits with IC-DISC

By Paul Oliveira, CPA at KLR

Feb. 28 – The recently-enacted American Taxpayer Relief Act of 2012 permanently assigned a preferential tax rate to qualified dividends, albeit at a somewhat higher 23.8 percent in many cases. This permanent preferential tax rate for dividends makes IC-DISC an effective tax planning strategy for many companies who deliver their products for use outside of the United States.

Many privately-held companies that are manufacturing product in the United States and delivering it to customers outside of the country, including Canada and Mexico, can significantly reduce their federal income taxes related to those export profits.

The IC-DISC is the last surviving federal income tax incentive for U.S. companies that export products to foreign countries. The IC-DISC is a separate legal entity and S-Corporations, individuals and partnerships are eligible to be shareholders.

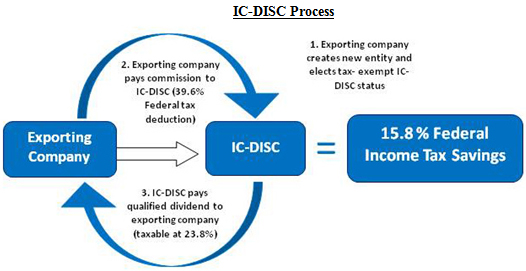

The IC-DISC provides a permanent federal income tax reduction to the shareholders of the IC-DISC. This permanent tax savings is realized when the exporting company deducts the commission it pays to the IC-DISC from its ordinary income. This commission would typically be deductible at 39.6 percent. IC-DISC is a tax-exempt entity, and a 23.8 percent tax is paid on qualified dividends to the shareholders of the IC-DISC. Thus, a reduction in federal income taxes from 39.6 percent to 23.8 percent on qualified export sales is realized.

IC-DISC Benefits:

- Permanent tax savings on qualified export sales.

- Increased liquidity for shareholders that is available throughout the year.

- Higher return on investment with no change to normal operations.

- Possible wealth shifting opportunities for estate planning purposes.

The diagram below provides a useful illustration of how the process works (from the client’s perspective).

If you are a privately-held business who is generating at least US$2 million in export sales, and whose overall operations are profitable enough to obtain the maximum benefits outlined above, IC-DISC could significantly reduce the federal income taxes related to those export profits. To qualify, it is essential that the products are substantially manufactured in the United States.

KLR is a New England-based provider of international tax services to middle market companies and works with both foreign-based companies moving to the U.S. market as well as domestic companies that do business around the world. For more information relating to the IC-DISC process, strategy, implementation, tax filings, ongoing maintenance, and IRS representation, please contact Paul Oliveira, CPA or any member of the KLR International Tax Services Team. KLR is also a member of the Leading Edge Alliance and a key U.S. partner for Dezan Shira & Associates.

Dezan Shira & Associates is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in emerging Asia. For further details or to contact the firm, please email asia@dezshira.com or visit www.dezshira.com.

- Previous Article The Annual Compliance Process for China FIEs

- Next Article Hong Kong Introduces Fund Management Tax Incentives