Using Your Excess China Funds to Make Small Low Risk Financial Trades and Increase Profitability

By Cathy Gong, Internal Treasurer, Dezan Shira & Associates

Do companies you operate In China have some cash sitting idle in the corporate accounts? This money may be the profit accumulation in recent months, or may be prepared in advance for large costs needing to be paid off in the coming months etc. When the idle money looks like it is becoming excessive and you don’t have a plan to use the funds in the short term, do you feel that it is also a kind of loss or waste as inflation erodes the real value of this money?

One obvious option available to companies is to simply repatriate the excess funds as dividends back to HQ. The funds can then be redeployed elsewhere. But what about if there is no urgent need for redeployment of those funds? Is your China operation among the most likely candidates for future investment in the future? If so, repatriation of funds overseas as dividends may not make sense, particularly when you consider the tax on dividend repatriation that will be incurred (10% of repatriated amount in the case of repatriation to most countries). CFOs will also be aware that the interest rate on excess deposits is ultra-low at the moment, and even negative in some countries. Even in China, the rate offered by banks on deposits in current accounts is only around 0.3%. Are any other options available?

One option available to better utilize some excess funds is to make small low-risk financial investments and increase your profitability within China. Based on the period of availability of the excess funds and your company’s investment risk appetite, there are a variety of investment products available in the market. Dezan Shira would like to share our experience of making small low risk financial investments in this article, focusing on buying short-term duration financial products issued by Chinese banks.

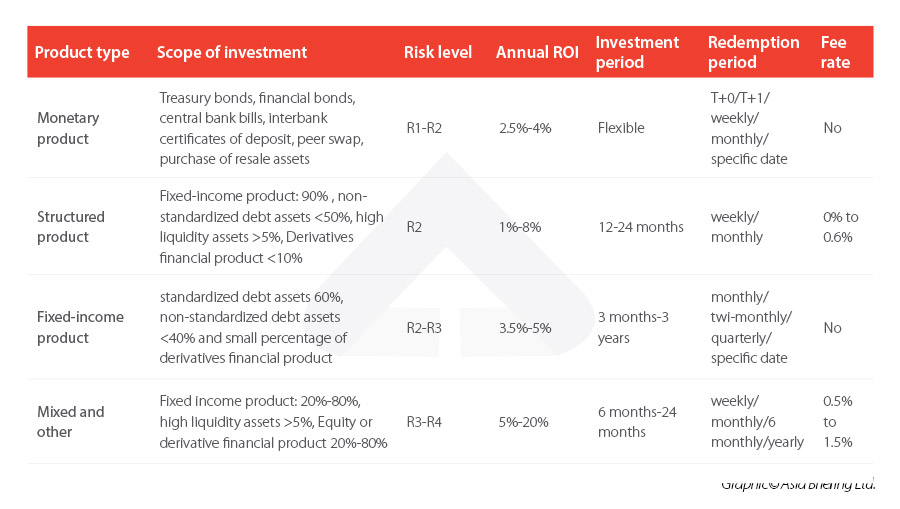

In China, the financial products sold by most of the state-owned banks to individuals or companies usually fall into the categories introduced in the following chart. Conservative Chinese investors usually make an appropriate allocation between these financial products, for the purpose of earning higher returns than the fixed term deposits while still maintaining flexibility to redeem the investment at short notice. Of course, they also try to limit the risk associated with their investments.. Among the 4 major financial products, monetary products are the most popular type among risk-averse investors. In many cases, some popular products will be snapped up within an hour after the release.

Monetary financial products have the lowest risk with the most flexibility in terms of redemption among all bank financial products, although banks do not secure the safety of principal for most of these monetary products. In practice, at least over the past several years there have rarely been cases of significant losses. In many cases, the actual ROI ends up to be slightly higher than the predicted ROI that was specified by the statement issued by the bank selling the financial products. Therefore, in the eyes of Chinese investors, monetary financial products are one of the safest ways to invest. The following are some cases from DSA own experience for your reference:

In most cases, the annual ROI of monetary financial products is about 3%, which tend to be higher than the ROI of similar financial products that are released by international banks based in Hong Kong or Singapore, for instance.

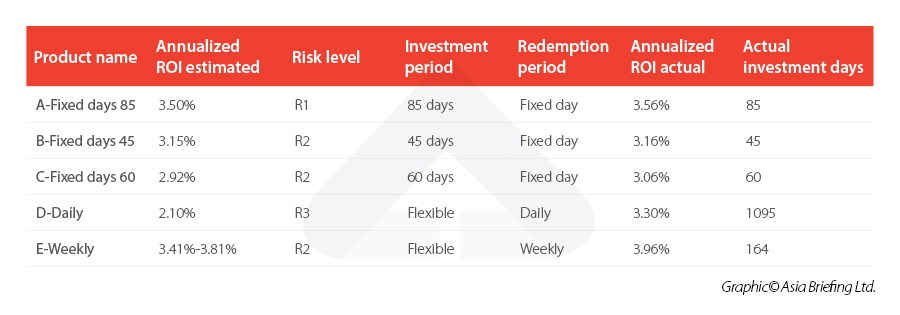

When you have some excess funds that you feel are unlikely to be utilized in the following weeks or months, you may consider to buy financial products in the “fixed-day” category (like product A, B, and C mentioned above),. Longer fixed-day products are also available, like 90 days, 120 days, 180 days and so on, or you can also select a relatively short-term product and activate the automatic repurchase option (including or excluding the profit component). These products differ from fixed-term deposit accounts in the sense that they represent financial products and carry slightly higher risk. Of course, the return available is also higher accordingly. Please note that if you do want to exit such a fixed-term investment early, there will be some penalty to be paid and you should understand the terms and conditions well before purchasing.

In situations when you are not sure exactly when you may need to use the excess funds for your core business purposes, you may select a financial product with a relatively flexible period, like the daily or weekly redemption products (product D and product E). There are also monthly and quarterly redemption products available for such financial products, the longer the investment term the higher the ROI which can be expected. If you allow your funds to accumulate in this way because you don’t really need use them in the short-term, such products can become a kind of longer-term investment with a higher ROI. Product D in the table above is a good example. Dezan Shira previously wanted to maintain flexible cashflow and bought this daily redemption product. Ultimately the money stayed in this product for 3 years and returned an annualized 3.3% ROI..

Many corporate investors prefer to buy financial products within the risk rate of R3. To ensure safety and mobility, Dezan Shira generally tends to allocate most of its investments to financial products with a risk rate of R2, and allocate a small portion under R1 and R3. Of course we make sure we also maintain healthy cash balances, as we know that investing is not even close to our core operation.

As I write this article, I am aware that many readers will be aware of the financial turbulence engulfing Evergrande, a major player in the Chinese real estate industry and therefore a big client of the Chinese banks. There is no doubt that within these banks’ financial products, some exposure to the Chinese real estate industry and even to Evergrande directly will exist. As with any investment, this risk must be factored into your considerations. It is a fact that the real estate sector has been a big driver of the Chinese economy over the past couple of decades, and it is one reason why interest rates on bank deposits and investment returns on financial product investments are higher in China than in many other countries. If the real estate sector shrinks in the future, the return which can be expected on these products may indeed fall. We certainly would not suggest investment of excess corporate funds into speculative products with high-risk profiles. At the same time, leaving all your excess cash in low-interest bank accounts is probably not optimal either. The examples provided above represent a balance between an ultra-safe approach and a speculative approach, and utilized only for funds we know won’t be used in the short-term by our China business.

This article is for information only. Dezan Shira & Associates do not provide financial investment advisory services and are not licensed to do so. We do not accept any responsibility or liability for any transactions made following information provided in this article. Please contact your licensed financial services provider or banker to inquire about such services.

Related Reading

China Briefing is written and produced by Dezan Shira & Associates. The practice assists foreign investors into China and has done so since 1992 through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Dongguan, Zhongshan, Shenzhen, and Hong Kong. Please contact the firm for assistance in China at china@dezshira.com.

Dezan Shira & Associates has offices in Vietnam, Indonesia, Singapore, United States, Germany, Italy, India, and Russia, in addition to our trade research facilities along the Belt & Road Initiative. We also have partner firms assisting foreign investors in The Philippines, Malaysia, Thailand, Bangladesh.

- Previous Article Wie EU-Unternehmen den 21 Billionen Euro schweren RCEP-Freihandelsmarkt über bestehende Abkommen erschließen können

- Next Article China’s Stock Markets – An Introductory Guide for Foreign Investors