China’s Biggest, Sustainable 2022 Consumer Trends

We look at some of the prominent consumer trends in China and spending patterns among its mid- to high-income groups and highlight sectors with potential for consumption growth. Meanwhile, Chinese brands are themselves making aggressive moves in western markets via online commerce channels and by localizing their brand identities to better reach their target audience.

In recent years there has been much discussion on an academic and public level of when the Chinese economy will overtake the United States’ and render China officially the wealthiest, and by consequence, the most powerful country in the world.

The “when” here is consciously used instead of “if”, because going by China’s economic track record in the past four decades, its surpassing the US economy is no longer considered a hypothetical scenario. Most experts find it to be inevitable sooner than later.

However, the COVID-19 pandemic has introduced a level of unpredictability in this straightforward reasoning as China’s strict zero-COVID policy has put it in more of an isolated spot than ever imagined by those experts and commentators.

Let’s look at the facts. China currently has the toughest COVID-19 policy in the world, and its strict epidemic prevention measures make it nearly impossible to visit the country. In addition to this, China is also looking at a demographic crisis with more and more people marrying late or not at all and therefore delaying or not having children. Finally, current tensions with the US and western countries have normalized mentions of ‘decoupling’ in global trade and business lexicon, with consequences for the reorganization of supply chains, technology competition, etc. In fact, all of this was better said in an article by Bloomberg where it was stated that: “ debt crisis, demographic drag, and international isolation could all keep China stuck in perpetual second place”.

All of the above is very interesting, and I am sure being debated in meeting rooms, auditoriums, cafes, and even bars across the world. However, this is not an article about China’s economy. Simply put, whether China stays in second, first, or third place – it does not really matter. The reality is that the Chinese economy with all its 1.4 billion consumers is the market to watch now, and the trends and decisions made by these consumers on what, when, how, where, and why to buy will especially impact countries whose economies depend on how much the Chinese “buy from them”. Something natural when you are the world’s second biggest importer.

So, what are the biggest consumer trends for China in 2022?

China’s still growing consumer class is the engine for global growth

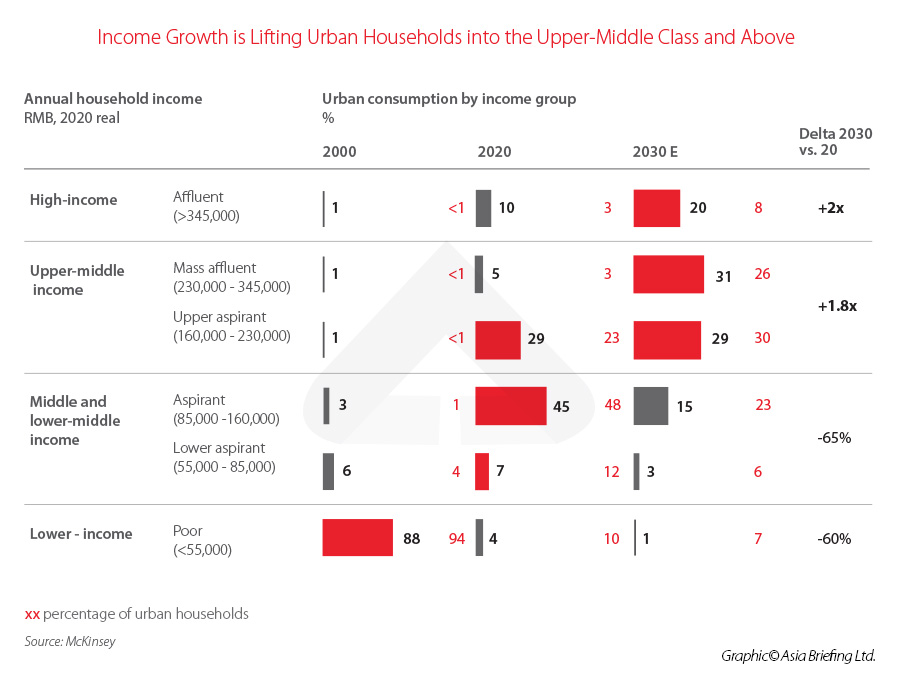

The growth of China’s middle class is well known; while this is slowing down – it is still relevant. In 2000, around 1.2 billion Chinese people did not have sufficient income to spend US$11 a day. That is considered the point by economists when people are members of the consuming class as they are able to afford some discretionary goods and services on top of basic necessities. By 2030, it is expected that about the same number of people will join the consuming class and climb up the income pyramid within it, as per data analyses by McKinsey & Company.

Consumers in the upper-middle brackets are likely to drive the biggest share of growth in China over the next decade. By 2030, 60 percent of urban consumption is projected to be driven by upper- middle-income consumers (with annual household incomes ranging from RMB 160,000/US$25,200 to RMB 345,000/ US$54,400 in real 2020 terms), compared with 35 percent today.

Another 20 percent of consumption could come from the segment above them, as the “high-income consumers” (with annual household incomes of RMB 345,000/ US$54,400 or more) double their current 10 percent share.

Also, as we have been witnessing for the past decade, China is the market for categories geared toward consumers with higher incomes. And by 2030, it may be home to about 400 million households with upper-middle and higher incomes – roughly as many as in Europe and the US combined.

In addition to the above, over the next five years, it is estimated that the number of millionaires in China may double, from around five million today to 10 million in 2025. As of 2022, China is responsible for about 17 percent of global GDP; however, the country accounts for a bigger percentage of consumption in diverse sectors.

This can be seen in the picture below.

Consumer trends in China – prominent spending patterns

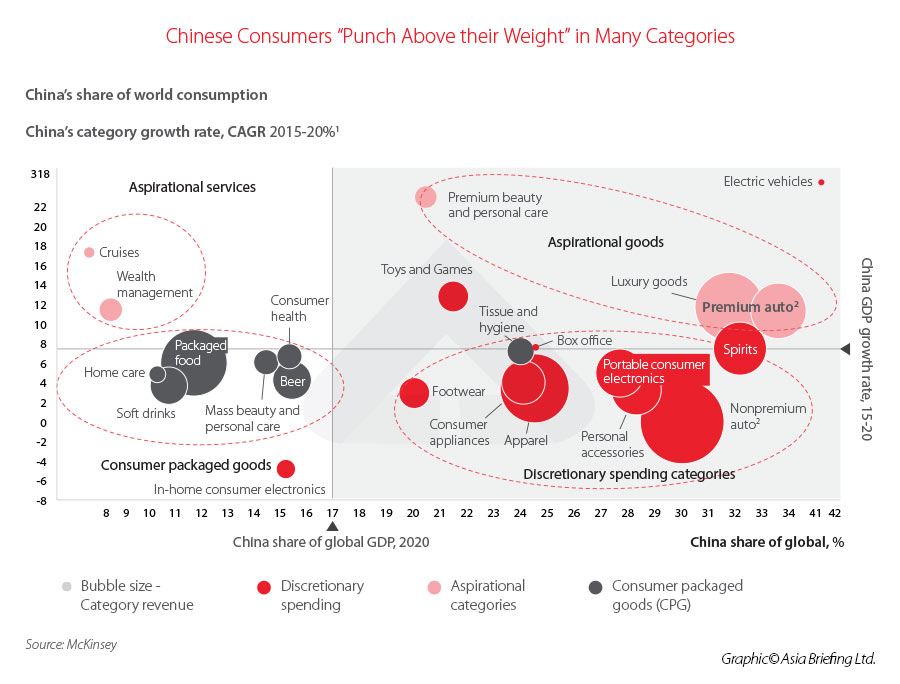

- China displays a high consumption pattern in areas such as fashion, accessories, consumer electronics, and electric vehicles (EV), in proportion to its share of national GDP. Special attention is given to EVs, which is in part due to governmental support of the purchase of said vehicles through the granting of subsidies, payment plans, etc. China represents 40 percent of world spending on EVs, and the investment in these products continues to grow at a rate of more than 7 times faster than the average global rate. It is the undisputed leader in EV purchase.

- China is a main market for other products geared towards consumers with medium to high income and luxurious lifestyle – for example, luxury goods, premium beauty and personal care products, and high-end cars. Curiously enough, other value-added or high-end services are yet to be demanded by this category of Chinese consumers, such as wealth management and cruise services – China buys less than the global average and its sector share of global GDP accounts for less 10 percent of said average. This means that there is a potential market growth opportunity to be explored. Some of that potential is starting to be realized in the case of wealth management and financial services in recent years. This category has been growing at nine percent per year in China, three times faster than globally, and financial services has been referred by the Chinese central and local governments as one of the priority industries for the country’s development.

- Even as more of China’s population moves rapidly into higher-income brackets, consumption in some categories of “mass” consumer packaged goods (CPG) remains underweighted relative to China’s share of global GDP. As an example, this country’s GDP represents between 10 to 15 percent of total consumption of packaged food, home care products, as well as mass beauty, personal care, and other health products. Despite this, many of these categories are growing substantially faster in China than in the rest of the world, so China continues to be an important engine of global growth.

The future of Chinese brands

Another thing that should also be mentioned is how Chinese brands are becoming more present in international markets and are fighting toe-to-toe (and sometimes even winning) against foreign brands.

As a matter of fact, during 2021, the most popular brand in sales in the US with 28 percent market share in fast fashion sales was surprisingly not H&M, Zara, or other well-known international fast fashion brands. It was Shein, a Chinese e-commerce company founded in 2008. In 2020, Shein completed its series E financing with a US$15 billion company valuation and has nearly 300 million fans across various social media platforms.

Another trend for Chinese brands is the growing tendency for branding localization. On December 1, 2021, The Chinese Brands Overseas Summit Forum was hosted online and localization was one of the main themes of the summit. It was discussed and agreed at the forum that the key to Chinese brands’ success in overseas markets is a strategy that defines the brand image and localizes products, to align them with the specific target audience.

Also, by using its familiarity with the online commerce business model, Chinese brands are opening a new market with their localization. One of the brands with the most traditional Chinese style is Florasis, a Chinese cosmetics company and brand that initiated operations in 2017 and quickly became a global brand, very popular in markets in North America, Europe, Russia, and Oceania. In 2020, Florasis planned to launch a new product line overseas. To localize its products, Florasis used the power of social media and marketing influencers. Before the launch, it targeted a micro-TikTok influencer with 200k followers, to do a makeup tutorial video with Florasis products. The first posted video became viral very quickly and reached an audience of over 5 million people. The influencer went viral with the products and has now reached over 14 million followers. The global fame of Florasis and other now well-known Chinese brands show how local Chinese brands can have a significant presence in the US market in a relatively quick timespan despite tensions between China and the US.

Consumption continues to rise

China now has the tools and infrastructure to not only be a consumer of foreign goods, but to also be a promoter and seller of its own goods, something that is achievable with its e-commerce, logistics, and marketing capabilities, all of which now surpass those of the west.

On a more macroeconomic level, despite China’s already large contribution to global consumption, there is still further room to grow.

The household consumption rate is a great way of understanding consumer spending; in China household consumption is roughly 38 percent of the nation’s GDP, which is lower than the 50 percent for the entirety of the Asia–Pacific region, 52 percent in the European Union, and finally 68 percent in the United States. This gap is explained by a higher savings rate in China than those countries, something seen as traditional in Chinese culture, and even associated with spending in real estate by many households. This state of affairs may change in the foreseeable future, as the financial system becomes more sophisticated and new policy directions steer consumers toward alternative investment options and consumption.

Finally, should the predictions of the World Economic Forum be accurate and China overtakes the US as the world’s biggest economy in 2028 and if the commitments of the Chinese Communist Party on more equality in distribution of income follow through, then the Chinese consumer class will undoubtedly continue to rise.

About Us

China Briefing is written and produced by Dezan Shira & Associates. The practice assists foreign investors into China and has done so since 1992 through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Dongguan, Zhongshan, Shenzhen, and Hong Kong. Please contact the firm for assistance in China at china@dezshira.com.

Dezan Shira & Associates has offices in Vietnam, Indonesia, Singapore, United States, Germany, Italy, India, and Russia, in addition to our trade research facilities along the Belt & Road Initiative. We also have partner firms assisting foreign investors in The Philippines, Malaysia, Thailand, Bangladesh.

- Previous Article China ESG Reporting – New Measures on Disclosure of Enterprise Environmental Information

- Next Article Opportunities for Australian Businesses in China in 2022