China-Australia Trade Reset: What It Means for Investors in 2026

China-Australia economic ties in 2026 are defined by resilient trade, selective investment, and expanding policy frameworks, shifting the relationship from disruption to structured engagement. For investors, the opportunity lies in navigating regulation, diversifying exposure, and leveraging growth in services, clean energy, and strategic sectors.

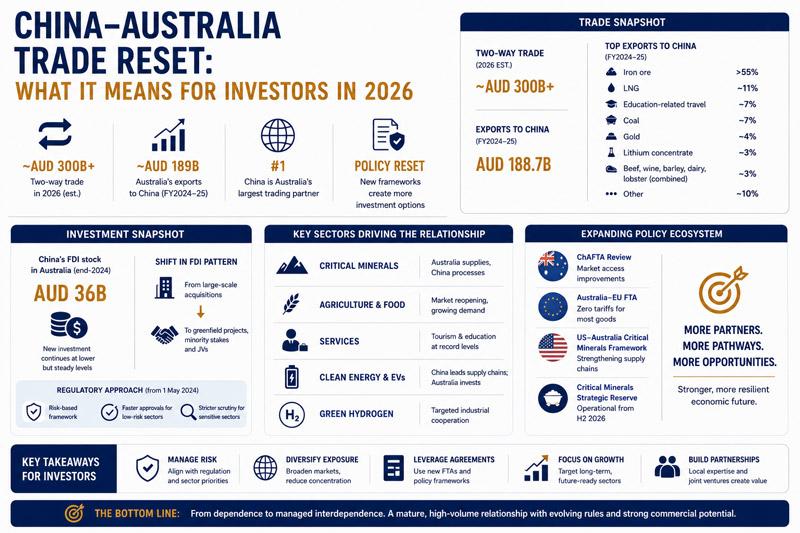

The China-Australia economic relationship is entering 2026 on a more stable and commercially viable footing than in previous years. While tensions between 2020 and 2022 disrupted trade flows, recent developments point to a recalibrated engagement model characterized by resilient trade volumes, selective investment, and diversified policy frameworks.

Two-way trade remains above AUD 300 billion (US$213.45 billion), services exports have recovered strongly, and new bilateral and multilateral policy tools are expanding investor options. For businesses, the key takeaway is a shift away from a “restriction narrative” toward managed interdependence with broader strategic flexibility.

How Can We Help

Navigating the evolving China-Australia economic relationship requires a clear understanding of bilateral trade frameworks, foreign investment regulations, and sector-specific compliance requirements across both jurisdictions.

We support foreign businesses by:

- Advising on ChAFTA utilization and tariff optimization for cross-border trade

- Conducting market entry and site selection analysis across critical minerals, agriculture, services, and clean energy sectors

- Supporting due diligence, joint ventures, and M&A transactions

- Advising on supply chain diversification and risk mitigation amid shifting policy landscapes

For support with China-Australia trade, investment structuring, or regulatory compliance, visit our website here or contact our specialists directly at australia@dezshira.com to discuss your business needs.

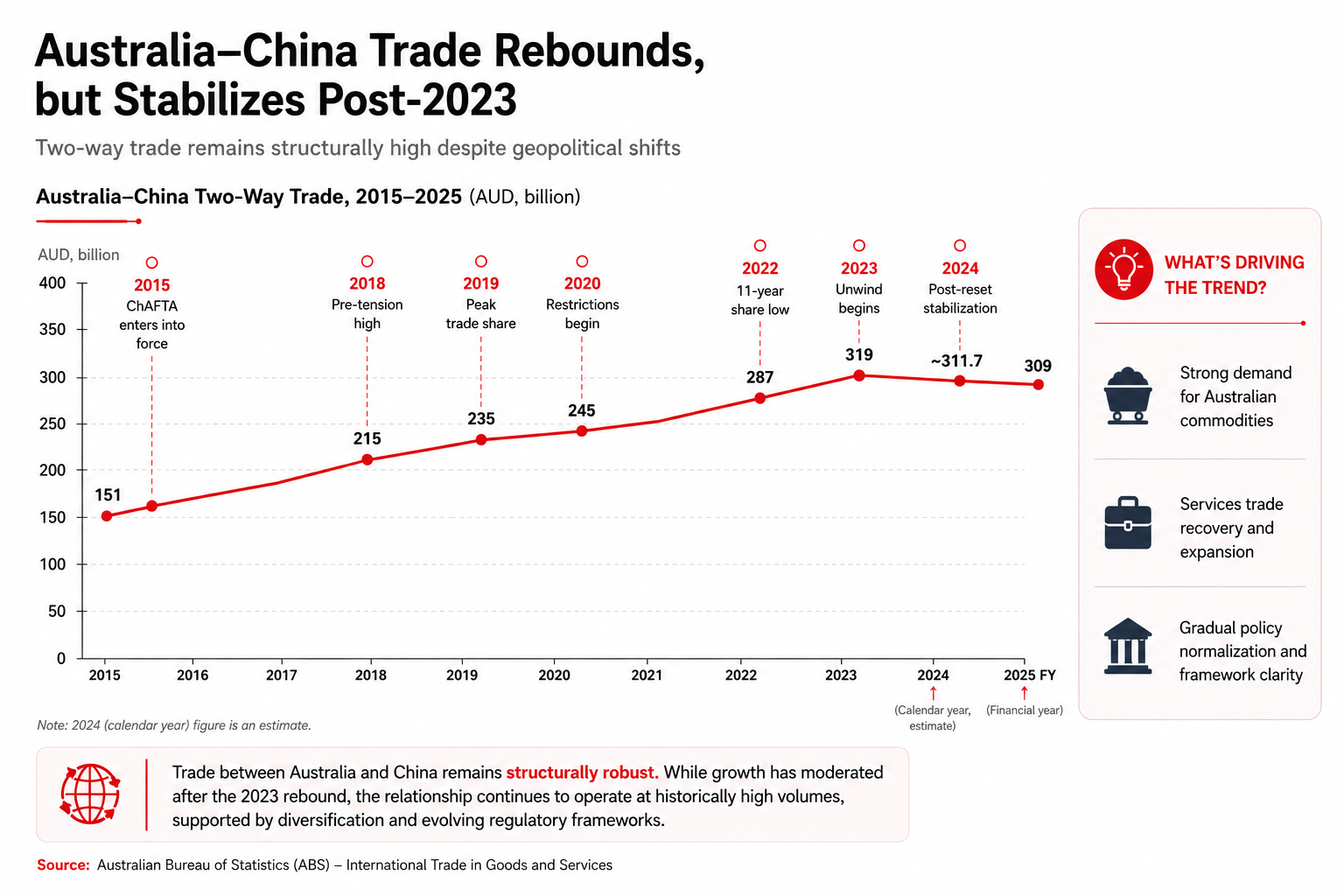

Trade recovery and structural resilience

Trade data underscores the durability of the bilateral relationship. Since the entry into force of the China-Australia Free Trade Agreement (ChAFTA), two-way trade has more than doubled, from AUD 151.2 billion (US$107.55 billion) in 2015 to AUD 311.7 billion (US$221.73 billion) in 2024. The most recent full official period (FY2024-25) still records AUD 309.0 billion (US$219.80 billion) in trade, with Australian exports to China reaching AUD 188.7 billion (US$134.23 billion).

Although early indicators for 2026 suggest slightly softer values due to commodity price normalization, overall volumes remain robust. A working estimate of around AUD 300 (US$213.40 billion) reflects price moderation rather than demand contraction, supported by recovering services and stable export flows.

This reinforces a key point for investors: China remains Australia’s largest trading partner, but the relationship is now less binary and more diversified across sectors.

Australian export composition: Concentration with gradual diversification

Australia’s export structure to China continues to be anchored by natural resources, particularly iron ore, which accounts for over half of exports. Other key categories include liquefied natural gas, coal, and education-related travel.

However, the composition tells a more nuanced story than before:

- Education services have re-emerged as a major growth pillar;

- Tourism flows have rebounded to record levels; and

- Agricultural exports, while fragmented in data, remain strategically significant.

Rather than a single-channel dependency, exporters are increasingly operating across multiple commercial tracks, including commodities, services, and premium consumer goods.

|

Australia–China Two-Way Trade, 2015-2025 (AUD, billion) |

||

| Category | (AUD, billion) | Share of exports to China |

| Iron ore | 104.8 | >55% |

| LNG | 20.9 | ~11% |

| Education-related travel services | 12.7 | ~7% |

| Coal (thermal + metallurgical) | 12.5 | ~7% |

| Gold | ~7 | ~4% |

| Lithium spodumene concentrate | ~5 | ~3% |

| Beef, wine, barley, dairy, lobster (combined) | ~6 | ~3% |

| Other | Balance | ~10% |

| Source: Australian Bureau of Statistics (ABS) – International Trade in Goods and Services | ||

Investment trends: Selective engagement over expansion

Foreign direct investment remains the most constrained dimension of the relationship, but the trend is better described as selective restructuring rather than decline. China’s FDI stock in Australia stood at approximately AUD 36 billion (US$25.60 billion) by the end of 2024, with new investment continuing at lower but steady levels. Importantly, the composition of investment has shifted:

- From large-scale acquisitions;

- Toward greenfield projects, minority stakes, and joint ventures;

This reflects both regulatory changes and evolving investor strategies.

Australia’s updated foreign investment framework (implemented since May 1, 2024) applies a risk-based approach, accelerating approvals for low-risk sectors while tightening scrutiny in areas such as:

- Critical infrastructure;

- Critical minerals; and

- Sensitive data and technologies.

For foreign investors, this means opportunities remain viable, but deal structuring is now critical.

Expanding policy ecosystem beyond bilateral ties

A defining feature of the 2026 landscape is the expansion of Australia’s external economic framework. Rather than replacing China, policymakers are building complementary channels to reduce overdependence.

Key developments include:

- Ongoing review of ChAFTA to improve market access;

- The Australia-EU Free Trade Agreement, which opens with near-zero tariffs for most goods;

- The US-Australia Critical Minerals Framework, supporting strategic supply chains; snf

- The Critical Minerals Strategic Reserve, enhancing project bankability.

Collectively, these initiatives create a multi-layered trade and investment environment, where engagement with China is supplemented (not replaced) by alternative partnerships.

Key investment and trade sectors

Critical minerals: Opportunity within structural constraints

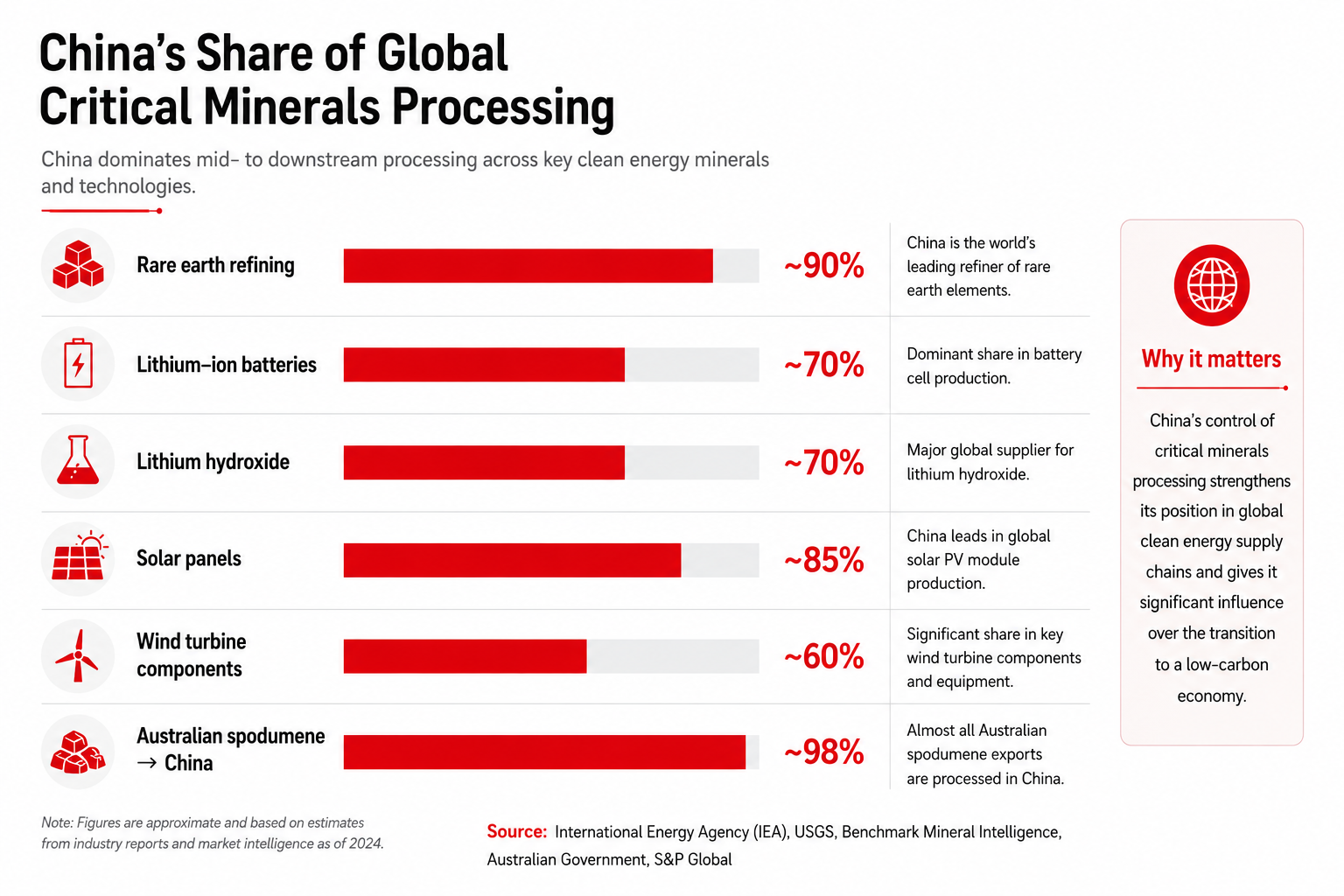

Critical minerals illustrate both the strengths and limitations of the current model.

Australia remains a leading upstream supplier, while China dominates processing capacity, including:

- Around 70 percent of global refining across key minerals; and

- Up to 90 percent in rare earth processing.

This creates a structural dependency, particularly in lithium and clean-tech supply chains.

However, Australia is actively developing midstream capabilities through:

- Tax incentives;

- Public financing; and

- Strategic offtake agreements.

The result is a gradual shift toward a more balanced value chain, although economic viability still depends heavily on policy support.

Agriculture and services: Renewed growth drivers

Agricultural trade has shown clear signs of normalization following the removal of earlier restrictions:

- Wine exports resumed in 2024;

- Meat export suspensions were lifted; and

- Lobster trade reopened.

At the same time, new safeguards, such as quotas on beef imports, indicate a transition toward managed market access rather than unrestricted trade.

|

Australia–China Two-Way Trade, by Category |

|||

| Product | 2025 result | 2026 risk/event | Investor implication |

| Beef | 1.545Mt record; China 273kt | Quota 205kt; 55% out-of-quota tariff | Diversification mandatory |

| Wine (TWE) | Penfolds +7.3%; +21% China depletions Oct | −40% H1 FY26 EBITS guidance | Channel restructuring underway |

| Dairy | A$987M China exports | Final tariff elimination 1 Jan 2026 | Premium positioning vs NZ |

| Barley | 73.1% reconcentrated to China | Saudi Arabia / Vietnam fall back | Single-buyer risk returns |

| Apples | <1% exports; A$680M domestic | Mainland market access from May 2026 | Greenfield growth runway |

| Lobster | Ban lifted Dec 2024 | Tropical Rock Lobster (Torres Strait) still impeded | 97.7% pre-ban concentration risk |

In parallel, services have emerged as a major strength:

- Chinese tourism spending has returned to high levels;

- Visitor arrivals have surpassed one million annually; and

- China remains the largest source of international students in Australia.

This reinforces the shift toward a broader economic relationship that includes people flows, services exports, and consumption-driven demand.

Green economy, clean tech, EVs

Chinese electric vehicle (EV) imports have rapidly become one of the most dynamic components of Australia’s automotive market, with China’s BYD emerging as the leading driver of this shift. The company reached 100,000 cumulative deliveries in Australia by April 2026 (less than three and a half years after entering the market), highlighting both strong consumer uptake and the scalability of its distribution model.

This rapid expansion is reflected in broader market dynamics. Battery electric vehicle (BEV) adoption continues to accelerate, supported by competitive pricing, expanding model availability, and improvements in charging infrastructure. In February 2026, Chinese brands collectively accounted for more than half of Australia’s BEV market, with BYD models and newer entrants such as Zeekr gaining traction alongside established players.

Solar, batteries, and grid-scale renewables

China’s role in global clean-energy supply chains remains dominant, and this influence is clearly visible in Australia’s renewable energy sector. Chinese manufacturers supply an estimated 85 percent of global solar panels, 70 percent of lithium-ion batteries, and approximately 60 percent of wind turbine components, making them integral to project development across Australia.

Domestic investment in clean energy has also strengthened. Australia recorded AUD 12.7 billion (US$9.03 billion) in clean-energy investment in 2024, including AUD 9 billion (US$6.40 billion) in new large-scale generation commitments, the highest level since 2018.

Despite this strong activity, formal Chinese outbound direct investment (ODI) in Australia’s renewable sector remains relatively limited. In 2024, only one transaction valued at AUD 183 million (US$130 million) was recorded.

Hydrogen: Cooperation under pressure

Hydrogen development has emerged as a more complex and uncertain area of Australia–China cooperation. Several high-profile projects have faced setbacks due to shifting policy environments and challenging project economics. At the same time, cooperation has not disappeared but is evolving into more targeted forms. In 2025, Fortescue secured a US$2 billion green financing package from Chinese banks, representing one of the largest sustainable finance transactions between the two countries. The company has also partnered with Taiyuan Iron and Steel, a subsidiary of China Baowu, to develop hydrogen-based, plasma-enhanced green iron technology, with an industrial trial line targeting 5,000 tonnes of output.

This points to a narrower but strategically important cooperation niche: industrial decarbonization, particularly in iron and steel production. Initiatives such as Fortescue–Baowu collaboration, BHP’s memoranda of understanding (MoU) with Chinese partners, and government-led platforms like the Steel Decarbonisation Roundtable suggest that climate-related industrial cooperation remains one of the most viable areas for sustained engagement.

Here, hydrogen is not an independent growth driver. Rather, its role is tied to wider decarbonisation efforts, where business incentives and emissions targets are converging.

Lithium operations under Chinese ownership

Chinese companies continue to play a significant role in Australia’s lithium sector, particularly through joint ventures, equity participation, and long-term offtake agreements.

Tianqi Lithium, for example, holds a 51 percent stake in Talison Lithium Energy Australia (TLEA), alongside IGO, and is involved in the Greenbushes mine, one of the world’s largest lithium operations, alongside Albemarle. The company has also invested in downstream processing capacity, although operations at the Kwinana refinery have faced interruptions.

Ganfeng Lithium has similarly established a diversified presence in Australia through investments in Pilbara Minerals, Core Lithium, and several smaller projects, as well as through long-term supply agreements.

While Chinese participation remains substantial, the structure of involvement has evolved. There is a gradual shift away from majority ownership toward joint ventures, minority stakes, and offtake-linked financing, reflecting both regulatory considerations and risk management strategies. Overall, Chinese involvement in Australia’s lithium sector remains critical to project development and global supply chains, even as ownership structures become more balanced and subject to closer regulatory oversight.

Comparative sector snapshot

| Variable | Critical Minerals | Premium Agriculture | Green Economy / EVs |

|---|---|---|---|

| Bilateral exposure | ~A$5–8bn lithium spodumene + REE; 49 mining + 29 processing projects | ~A$6bn beef/wine/dairy/barley + apples opening 2026 | EV imports dominant; renewable FDI modest (A$183m 2024) |

| Growth profile | Moderate-high (CMPTI from 2027; A$18bn export target) | Moderate; quota-constrained | High on import side; slow on Australian green-export side |

| Risk level | High (Chinese processing dominance; FIRB divestment) | Medium (quotas + NTBs + grey-market crackdown) | Medium-high (FIRB scrutiny; supply-chain concentration) |

| Preferred Chinese entry mode | Minority equity + offtake; greenfield processing-adjacent | CBEC / O2O distribution; brand JV | Greenfield distribution (BYD model); equipment supply |

| Key 2026 policy event | CMSR operational H2 2026; CMPTI from 1 July 2027 | Beef quota 1 Jan 2026; dairy 0% 1 Jan 2026; apples May 2026 | EU FTA tariff-free critical minerals from March 2026 |

| Lobster | Ban lifted Dec 2024 | Tropical Rock Lobster (Torres Strait) still impeded | 97.7% pre-ban concentration risk |

Implications for investors

The China-Australia trade reset marks a transition from unrestricted expansion to structured, policy-aware engagement.

For investors, the key strategic considerations include:

- Structuring investments to align with regulatory priorities;

- Diversifying exposure across markets and sectors;

- Leveraging new policy frameworks and trade agreements; and

- Expanding into services and value-added segments.

The relationship has developed into a high-volume trade corridor, with rules and opportunities that continue to evolve.

Conclusion

The 2026 phase of China–Australia economic engagement is becoming more complex, but it is also offering clearer avenues for investment. Trade flows remain substantial, services are expanding, and policy frameworks are gradually opening new pathways for growth.

For businesses, success will depend on adjusting to this evolving landscape rather than expecting a return to past conditions. Scale, diversification, and regulatory strategy are all becoming central considerations.

Whether launching, restructuring, or expanding, we ensure our clients benefit from coordinated input across legal, HR, tax, and financial teams. From startup to exit, our advisory scales with your business—designed to meet both immediate needs and long-term goals.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article How to Succeed in IP Litigation in China – Lessons from the Supreme Court’s Case Files

- Next Article What Are the Main Compliance Calendars Foreign Businesses Must Track in China?