What Are the Main Compliance Calendars Foreign Businesses Must Track in China?

China compliance calendar requires foreign businesses to manage continuous monthly, quarterly, and annual obligations in an increasingly digital and data-driven regulatory environment. Success depends on integrating compliance into core operations, ensuring accuracy across systems, and adapting to both national and local regulatory requirements.

Foreign companies operating in China are often surprised by the frequency and intensity of compliance obligations. Unlike many jurisdictions, China operates a high-frequency, multi-agency compliance system, where monthly, quarterly, and annual filings overlap. Missing deadlines can trigger unnecessary scrutinies, credit-downgrades, penalties, or even restrictions on business operations.

For foreign-invested enterprises (FIEs), compliance is a continuous operational requirement. Understanding and managing China’s compliance calendar is therefore critical to maintaining regulatory standing and supporting long-term growth.

How we can help

Navigating China’s compliance calendar requires a detailed understanding of local regulations, administrative practices, and evolving policy frameworks. We support foreign businesses by:

- Designing compliance calendars tailored to business activities

- Managing monthly, quarterly, and annual filings

- Conducting tax health checks and audit preparation

- Advising on regulatory changes and risk mitigation

For support with compliance management or market entry in China, contact our advisors at china@dezshira.com.

Monthly compliance

Monthly compliance forms the foundation of China’s regulatory system and applies even to companies with no revenue or operational activity.

Key obligations:

- Corporate income tax (CIT) prepayment filing (for taxpayers approved or required to prepay on a monthly basis)

- Value-added tax (VAT) and surcharges linked to VAT filings (for taxpayers assessed for monthy filing)

- Other taxes where monthly filing applies, such as consumption tax (CT) and resources tax, subject to the tax authority’s assessment

- Individual income tax (IIT) withholding and reporting on salaries and wages

- Social insurance and housing fund contributions

Most monthly tax filings and payments must be completed within 15 business days after the end of the month, with deadlines adjusted for public holidays and subject to local tax bureau implementation. While the tax scope and frequency depend on the taxpayer’s classification and industry, authorities increasingly rely on monthly data to perform cross‑checks and risk profiling rather than waiting for annual reviews.

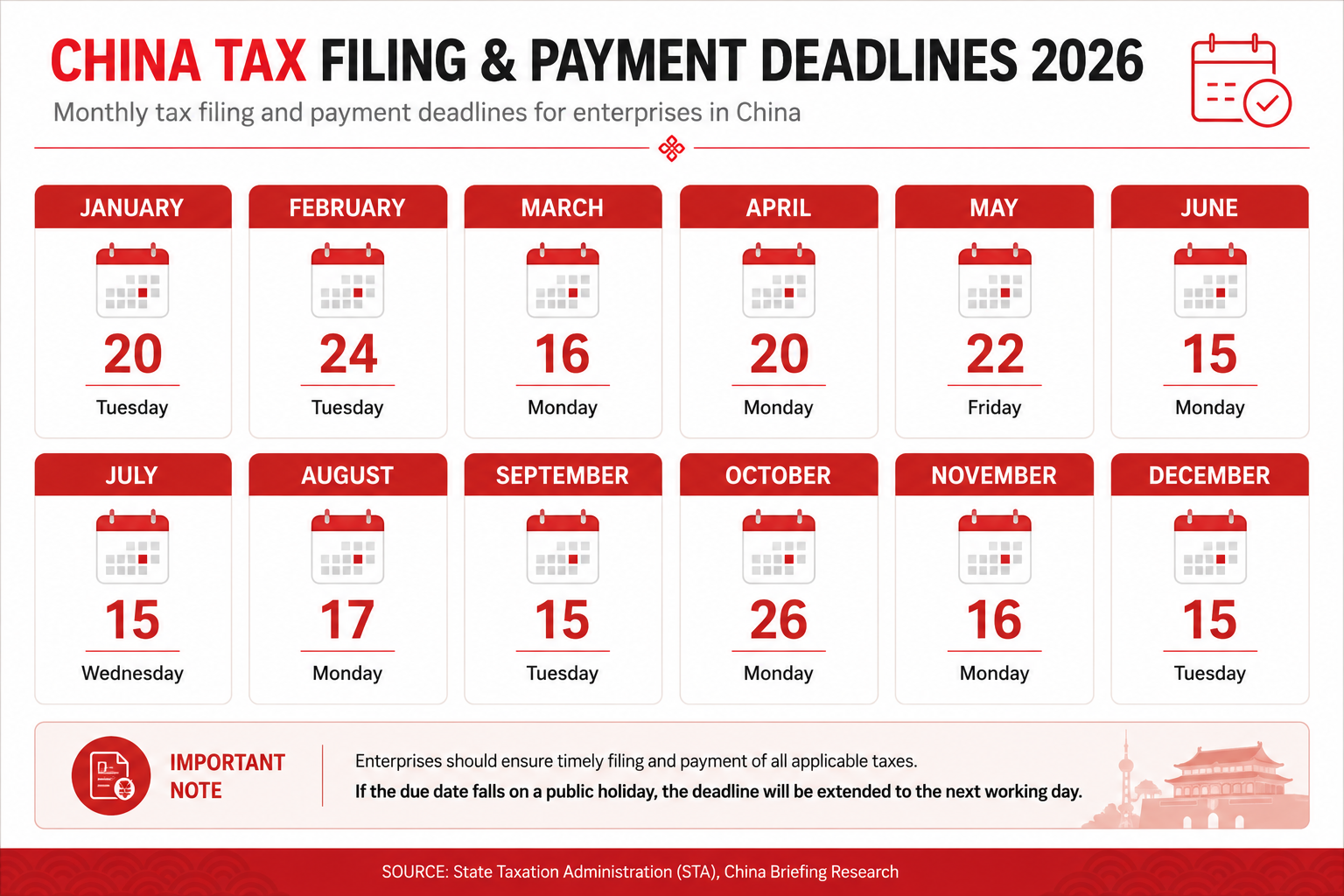

See also: China Tax Filing and Payment Deadlines for 2026

Why it matters

Monthly compliance is where most risks arise. Errors in VAT invoicing (fapiao), payroll calculations, or delayed filings are among the most common sources of regulatory scrutiny and follow‑up by tax authorities. As China’s tax system becomes increasingly digitized, particularly under the Golden Tax framework, oversight is shifting toward continuous, data‑driven monitoring.

Compliance issues are more likely to be flagged through system alerts and risk profiling rather than through traditional retrospective audits, increasing the importance of accuracy and consistency in day‑to‑day filings.

Quarterly compliance

Quarterly compliance in China is not limited to CIT. Depending on the taxpayer’s size, industry, and assessed risk profile, multiple taxes may be filed and paid on a quarterly basis rather than monthly, as determined by the local tax bureau.

Taxes that may adopt quarterly filing and payment cycles include:

- CIT prepayment for eligible taxpayers approved for quarterly filing

- VAT and surcharges for eligible taxpayers approved for quarterly filing

- CT where quarterly payment periods are granted

- IIT for certain business income scenarios

- Resource tax

- Environmental protection tax calculated monthly but declared quarterly

These taxes are generally required to be declared and paid within 15 days after the end of the quarter, subject to statutory holidays and local tax bureau adjustments.

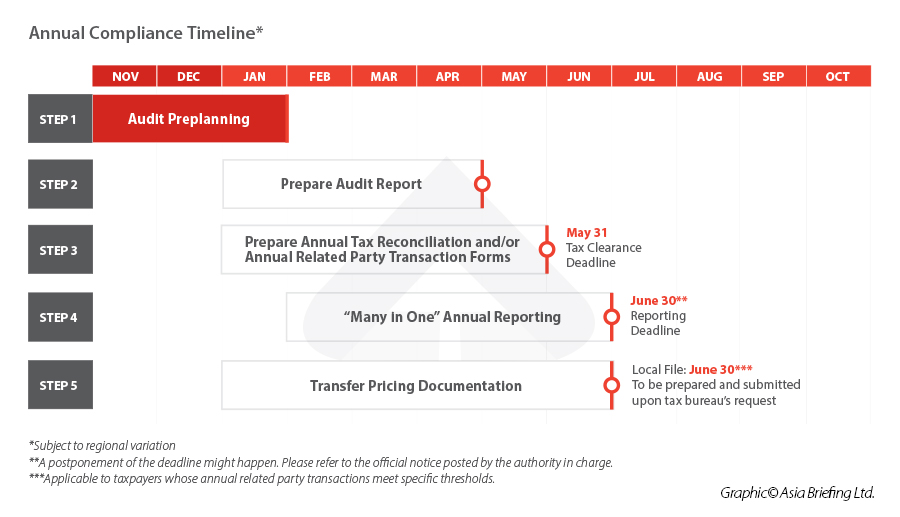

Annual compliance

Annual compliance represents the most complex and closely monitored stage of the compliance calendar.

Core requirements for general businesses include:

- Statutory annual audit (conducted by a licensed CPA firm)

- CIT annual reconciliation by May 31

- Annual reporting to multiple government agencies by June 30

- Transfer pricing documentation (if applicable) to be prepared by June 30

- Annual social insurance and housing fund base adjustment with deadlines subject to city variances

See also: Annual Compliance Requirements in China: A Step by Step Guide

In addition, annual compliance obligations may vary by industry and entity type, such as license renewals, environmental or cybersecurity filings (where applicable), and requirements specific to NGOs or other regulated entities.

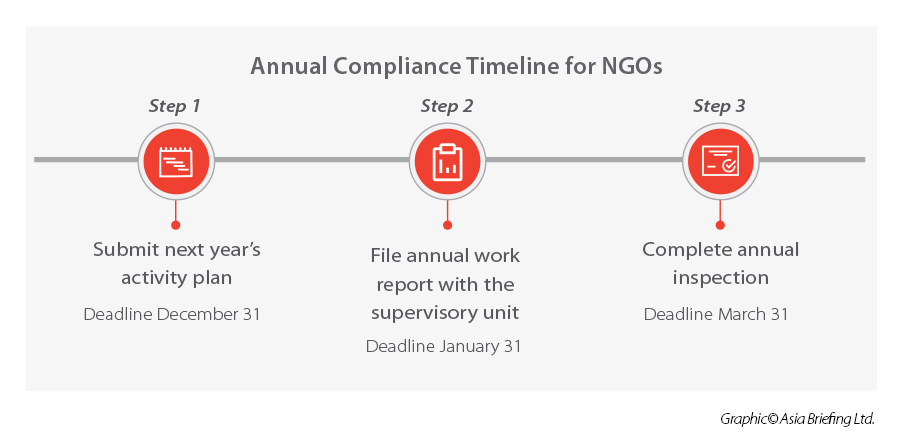

See also: Annual Compliance Requirements for Foreign NGOs in China

Why it matters

This is the stage where regulators assess a company’s overall tax compliance and financial integrity. Failure to meet requirements can result in:

- Financial penalties and late payment surcharges

- Audit investigations

- Restrictions on profit repatriation

- Negative records in China’s corporate credit system

Key compliance risks for foreign businesses

Foreign companies operating in China commonly face the following challenges:

- Fragmented regulatory system: Multiple authorities (tax, commerce, HR, customs) with overlapping requirements;

- Localization risk: Enforcement and procedures vary across cities and provinces;

- Data-driven enforcement: Authorities increasingly rely on digital systems to cross-check invoices, bank flows, and filings; and

- Mismatch between accounting and tax reporting.

China’s digital tax system is reshaping compliance

One of the most important developments affecting compliance in China is the rapid digitalization of tax administration. The rollout of systems such as the Golden Tax System Phase IV is enabling tax authorities to integrate data across invoices (fapiao), banking transactions, customs records, and payroll reporting.

This shift means that discrepancies between different filings (such as VAT declarations, corporate income tax filings, and financial statements) can be identified more quickly and with greater accuracy. As a result, compliance in China is increasingly real-time and data-driven, rather than reliant on periodic audits.

For foreign businesses, this has two key implications. First, manual or fragmented reporting processes carry higher risk, as inconsistencies are more likely to be detected. Second, companies must ensure that their accounting, tax, and operational data are fully aligned across systems.

In practice, this is accelerating the transition from reactive compliance toward continuous compliance management, where internal controls and data consistency are as important as meeting filing deadlines.

Regional variations

While China’s compliance framework is nationally defined, enforcement and administrative practices can vary significantly across regions. Cities such as Shanghai, Beijing, and Shenzhen typically offer more streamlined digital filing systems and clearer administrative procedures, while smaller cities may require more manual interaction with local authorities.

Differences can also arise in:

- Social insurance contribution rates and calculation bases;

- Local tax bureau interpretation of policies; and

- Implementation timelines for regulatory updates.

For foreign businesses, this means compliance cannot be managed solely at the national level. Instead, companies must adapt their processes to local regulatory practices, particularly when operating across multiple jurisdictions.

Key takeaway: How to manage China compliance calender effectively

China’s compliance framework is structured around continuous monthly, quarterly, and annual obligations, requiring foreign businesses to adopt a proactive and system-driven approach.

As regulatory enforcement becomes more digital and data-driven, compliance is no longer limited to meeting filing deadlines. It now requires alignment across accounting systems, operational processes, and regulatory reporting, with increasing emphasis on accuracy and consistency.

Foreign businesses are advised to:

- Establish integrated accounting and tax systems aligned with Chinese regulations;

- Conduct monthly internal compliance checks, not just annual reviews;

- Align finance, HR, and legal teams to avoid siloed reporting; and

- Work with local advisors to manage regulatory updates and regional differences.

For investors, the key is not simply to remain compliant, but to build compliance into the core of business operations.

With rapid reforms and inconsistent enforcement across the region, companies face challenges at every stage of their lifecycle. Dezan Shira & Associates’ tax advisory teams include experienced tax accountants, lawyers, and former tax officials who help clients navigate these complexities, reduce risk, and optimize tax outcomes—providing clients with comprehensive advisory and compliance support tailored to regional requirements.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article China-Australia Trade Reset: What It Means for Investors in 2026

- Next Article IR56B Common Errors: A Guide to Avoiding IRD Follow-Up in Hong Kong