China's Individual Income Tax (IIT) system, governed by the amended IIT Law, applies to all individuals, Chinese and foreign nationals alike, who reside in or derive income from China. Tax residents are subject to worldwide taxation, while non-residents are taxed only on China-sourced income.

Comprehensive income is subject to progressive tax rates ranging from 3 to 45 percent, applied on a cumulative basis.

Employers are responsible for accurately calculating and withholding IIT on all forms of employment income — including wages and salaries, bonuses, stock options, and allowances — before remitting the net amount to employees.

Key Features of the Amended IIT Law

- Individuals who qualify as Chinese tax residents are taxed on their global income, not just income earned within China.

- China's participation in the Common Reporting Standard (CRS) means that overseas financial accounts and income are increasingly visible to Chinese tax authorities, heightening the importance of accurate reporting.

- Both employees and employers carry significant compliance responsibilities. Failure to meet withholding or reporting obligations can result in penalties for the employing entity.

This section covers the fundamentals of individual taxation that are imperative for all employers to understand before establishing a business presence in China.

China’s individual income tax system explained

Under China's IIT Law, individual income tax applies to a broad range of income types earned by both resident and non-resident taxpayers. Understanding which categories of income are taxable, and how they are computed, is essential for employers to meet their withholding obligations.

Who is subject to IIT in China?

China's IIT Law divides taxpayers into two categories based on residency, each carrying different tax liabilities:

- Individuals who have a domicile in China, or who reside in China for 183 days or more in a tax year, are treated as resident taxpayers and are generally subject to IIT on their worldwide income.

- Individuals with no domicile in China who reside in China for fewer than 183 days in a tax year are non-resident taxpayers, subject to IIT only on income sourced in China.

Categories of taxable income

The IIT Law identifies nine categories of individual income subject to tax, each with its own computation method and applicable deductions:

- Wages and salaries. The most common category for employed individuals, including base pay, bonuses, allowances, and stock options. Employers must withhold IIT monthly.

- Income earned from services provided outside of an employment relationship. A 20 percent deemed expense deduction applies before computing taxable income.

- Income from the publication or distribution of works. A 20 percent deemed deduction applies, with a further 30 percent discount on the remaining amount when calculating taxable income.

- Income from licensing intellectual property rights for use in China. A 20 percent deemed expense deduction applies.

- Income derived from the operation of sole proprietorships, partnerships, or contracted/leased operations.

- Investment returns distributed by enterprises, institutions, or resident individuals in China. Taxed at a flat rate without an expense deduction.

- Rental income from real estate or other assets leased within China.

- Gains from the sale or transfer of immovable property, equity, or other assets located in China.

- Contingent income. One-off income not falling into any of the above categories, such as prizes and windfalls.

For resident taxpayers, the first four income types — wages and salaries, labor remuneration, author's remuneration, and royalties — are consolidated into a single category called comprehensive income and are assessed on an annual basis. However, employers are still required to calculate and withhold IIT on a monthly basis throughout the year. The taxable amount of comprehensive income is calculated as:

Annual gross income minus standard deduction (RMB 60,000/year, approx. US$8,500) minus special deductions, special additional deductions, and other statutory deductions.

The resulting balance is the taxable income on which progressive IIT rates of 3 to 45 percent are applied.

|

IIT Withholding Rates Table for Resident Individuals |

|||

|

Level |

Taxable income amount subject to cumulative withholding (RMB) |

Withholding rate |

Quick deduction ( RMB) |

|

1 |

≤36,000 |

3% |

0 |

|

2 |

36,000 - 144,000 |

10% |

2,520 |

|

3 |

144,000 - 300,000 |

20% |

16,920 |

|

4 |

300,000 - 420,000 |

25% |

31,920 |

|

5 |

420,000 - 660,000 |

30% |

52,920 |

|

6 |

660,000 - 960,000 |

35% |

85,920 |

|

7 |

>960,000 |

45% |

181,920 |

For non-resident taxpayers, the first four types of income are computed separately per time or per month when it occurs. The taxable income amount for income from wages and salaries of a non-resident individual shall be the balance after the deduction of the standard deduction (RMB 5,000 per month, approx. US$710), as well as other applicable deductions. The IIT rates for non-resident taxpayers are generally equal to those for resident taxpayers.

|

IIT Rates Table for Non-resident Individuals (Monthly) |

||

|

Taxable income amount (RMB) |

IIT rate |

Quick deduction (RMB) |

|

≤3,000 |

3% |

0 |

|

3,000 - 12,000 |

10% |

210 |

|

12,000 - 25,000 |

20% |

1,410 |

|

25,000 - 35,000 |

25% |

2,660 |

|

35,000 - 55,000 |

30% |

4,410 |

|

55,000 - 80,000 |

35% |

7,160 |

|

>80,000 |

45% |

15,160 |

Taxpayers and tax liability

To calculate IIT for an employee, the employer must decide whether an employee is liable for IIT.

The IIT Law divides IIT taxpayers into two categories: resident taxpayers and non-resident taxpayers.

Domestic employees and foreign employees who stayed or are expected to stay in China for at least 183 days are regarded as resident taxpayers, while expatriates who come to China for short-term (less than 183 days) work, such as commercial performance and training, are regarded as non-resident taxpayers.

Resident taxpayers and non-resident taxpayers have different tax liabilities to their income, as summarized below:

|

Tax Liability of Resident Taxpayer and Non-Resident Taxpayer |

||

|

Taxpayer status |

Domicile and residence time |

Tax liability |

|

Resident taxpayer |

Having a domicile in China |

|

|

|

|

|

|

|

|

Non-resident taxpayer |

|

Income sourced in China |

|

Income sourced in China that is paid or borne by domestic employer |

|

Six-year rule

Individuals who do not have a domicile in China will not be required to pay IIT on their worldwide income until they have lived in China for 183 days or more in a year for more than six years in a row. The six-year rule began on January 1, 2019. The number of years before 2019 won’t be included in the six-year count, and individuals with no domicile in China won’t be subject to worldwide income before 2024.

The six-year count can be reset by living in China for less than 183 days in a tax year or by leaving China for more than 30 days in a row where their days of residence in China have reached 183 days in a tax year.

Income sourced in China

The following income shall be deemed income sourced in China, regardless, if the place of payment is in China or not:

- Income derived from independent services provided in China due to tenure of office, employment, performance of contract, etc.;

- Income derived from the lease of property to a lessee for use in China;

- Income derived from licensing of various licensing rights for use in China;

- Income derived from the transfer of properties such as immovable property in China or transfer of other properties in China; and

- Income from interest, dividends, and bonuses is derived from enterprises, institutions, other organizations, and resident individuals in China.

As to employment relationship, income sourced in China is defined by 'salary and wages that are related to the individual’s working period in China'.

Under the IIT Law, the working period is counted in days, including actual working days, public holidays, annual leaves, and training days that occurred inside and outside of China during the individual’s China working period.

A day in which a non-domicile person stays in China for less than 24 hours will be counted as 0.5 days when calculating their working period in China for tax calculation purpose. This applies to non-domicile people who are employed by domestic and foreign employers simultaneously or who are employed by foreign employers only but provide work in China and abroad at the same time.

The actual work-time rule does not apply if the individual holds a senior management position in domestic enterprises in China. Their director’s fees, supervisor’s fees, wages and salaries, and other similar income, such as bonuses and stock options paid by the domestic enterprise, shall be regarded as income sourced from China, regardless of whether they work in China.

Tax-exempt income

Under the IIT Law, the following types of individual income shall be exempted from individual income tax:

- Awards for achievements in science, education, technology, culture, public health, sports, environmental protection, etc., granted by the provincial people’s governments, ministries, and commissions under the State Council, units of the Chinese People’s Liberation Army at or above corps level, as well as foreign organizations and international organizations;

- Interest income on treasury bonds and other financial debentures issued by the state;

- Subsidies and allowances issued on a unified basis in accordance with the provisions of the state;

- Welfare benefits, compensation, and relief funds;

- Insurance claims;

- Military severance payment, demobilization pay, and decommissioning pay received by members of the armed forces;

- Settling-in allowance, severance pay, basic pension or retirement pay, retirement allowances, and subsidies given to public servants and workers on a unified basis in accordance with the provisions of the state;

- Income derived by diplomatic representatives, consular officers, and other personnel of embassies and consulates in China, which are exempted from tax in accordance with the provisions of the relevant laws of China;

- Tax-exempt income stipulated in international conventions and executed agreements to which the Chinese Government is a party; and

- Other tax-exempt income stipulated by the State Council.

Deductions

The IIT Law allows several deductions, like, standard deductions, special deductions, special additional deductions, and other deductions determined pursuant to the law, to be deducted from the wage and salaries when calculating the taxable income.

Standard deductions

Standard deduction refers to a fixed amount of money that can be deducted from the individual’s taxable income, which equals to the government’s evaluation of the basic living expenses of the individuals.

The standard deductions for all taxpayers (domestic and foreign employees) are unified to RMB 5,000 per month.

Special deductions

Special deductions refer to the basic social insurance premiums and housing fund contributed by the employee in accordance with the scope and standard stipulated by the laws and regulations.

Each region has their stipulated basic contribution rates. Contributions beyond that might not be pre-tax deductible. For example, although employees are allowed to make additional contributions to the housing fund, it’s not pre-tax deductible for the part over 12 percent of their salary.

Special additional deductions

The IIT system introduced ‘special additional deductions for specific expenditures’ (hereinafter, special additional deductions), which include:

|

IIT Special Additional Deductions in China |

|||

|

Item |

Applicable scope |

Deduction Amount |

Deduction method |

|

Nursing expenses for children under 3 years old |

Nursing expenses |

RMB 2,000/month for each child (or RMB 24,000/year for each child) |

The standard deduction for each kid 50/50 split between parents (guardian), or 100% deducted by one parent (guardian) |

|

Children’s education expenses |

Pre-school education Diploma education |

RMB 2,000/month for each child (or RMB 24,000/year for each child) |

The standard deduction for each kid is 50/50 split between parents, or 100% deducted by one parent (guardian) |

|

Continuing education expenses |

Diploma education Professional qualification |

RMB 400/month, up to 48 months (or RMB 4,800/year, up to four years) RMB 3,600 in the year when the related certificate was issued |

Standard deduction A parent could choose to claim such expenses for their child if it’s for diploma education |

|

Healthcare costs for serious illness |

Expenses recorded in the social medical insurance management system |

Maximum RMB 80,000 based on actual basis |

Deduction on actual expenses Can only deduct the medical cost that is over RMB 15,000 and borne by the individuals Could claim for the spouse and the underaged children |

|

Housing loan interest |

First housing loan under taxpayer or spouse’s name |

RMB 1,000/month up to 240 months (or RMB 12,000/year, up to 20 years) |

Standard deduction Could be a 50/50 split between the couple, or 100% deducted by one of them. |

|

Expenses for supporting the elderly |

Parents over 60 years old Other legal dependent |

RMB 3,000/month (or RMB 36,000/year) |

The standard deduction in total, regardless of the actual number of the elderly Could share among siblings, but each one can deduct no more than RMB 1,500/month (or RMB 18,000/year) |

|

Housing rent |

The taxpayer and spouse do not have a house in the city where they work |

Three applicable deduction amounts based on working locations: RMB 1,500/month (or RMB 18,000/year) RMB 1,100/month (or RMB 13,200/year) RMB 800/month (or RMB 9,600/year) |

Standard deduction Shall be 100% deducted by one of the couples if they live in the same city The couple can claim this deduction separately if they live in different cities and have no house in both cities |

Tax-exempt fringe benefits for foreigners

The Chinese tax bureau currently allows foreign employees to enjoy certain fringe benefits without imposing the tax on these benefits. It’s common practice that companies structure part of their foreign employee’s salary as fringe benefits.

.

Generally, the below allowances are not taxable:

- Housing expense;

- Meal expense;

- Laundry expesne;

- Education expense for children;

- Language training expense;

- Relocation expense;

- Business travel expenses; and

- Home visit expense.

When applying these tax-exemption benefits on foreigners’ income, certain conditions must be met, and the employers need to do proper arrangement from the start of the employees’ assignment to make sure the foreigners are aware of these conditions and make sure the conditions are met when enjoying this kind of tax-exemption.

To attract and retain foreign talent, the Ministry of Commerce and the State Taxation Administration jointly extended China’s preferential IIT policy on foreigners' fringe benefits until December 31, 2027.

Other deductions determined pursuant to the law

The IIT Law allows certain other deductions, such as payment by an individual for enterprise annuity and occupational annuity, which comply with state provisions, expenditure of an individual for purchase of commercial health insurance and tax-deferred commercial pension insurance which comply with State provisions, and other deductible items stipulated by the State Council.

IIT calculation

For resident individuals

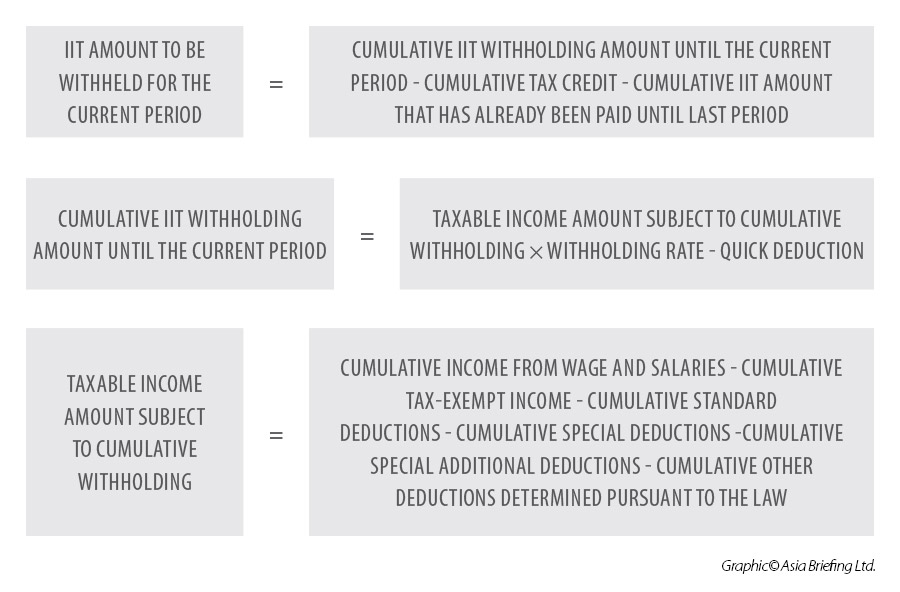

When a company pays wages and salaries to an employee who is regarded as a resident individual, it must compute the IIT amount using the ‘cumulative withholding method’ and withhold and report the IIT on a monthly basis.

Under the cumulative withholding method, the ‘IIT amount to be withheld for the current period’ should be the balance of the ‘cumulative IIT withholding amount until the current period’, with the ‘cumulative tax credit’ and the ‘cumulative IIT amount that has already been paid’.

To calculate the cumulative IIT withholding amount until the current period:

- Calculate the taxable income amount subject to cumulative withholding by deducting various items – including the cumulative tax-exempt income, the cumulative standard deductions, the cumulative special deductions, the cumulative special additional deductions, and cumulative other deductions determined pursuant to the law – from the taxpayer’s cumulative income from wages and salaries for the tax year derived from employment up to the current month; and,

- Apply the applicable withholding rates and quick deductions stipulated in the IIT Withholding Rates Table for Resident Individuals.

Where the IIT amount to be withheld is negative, a tax refund will not be made in the interim. Where the balance amount at the end of the tax year is still a negative value, the taxpayer will, through completing annual tax reconciliation for consolidated income, obtain a tax refund for excess tax paid and make retrospective payment if there is underpaid tax.

For non-resident individuals

When a company pays wages and salaries to a non-resident individual, it is required to withhold and report IIT on a monthly basis, or for each payment, in accordance with the following methods:

- Calculate the taxable income amount by lessening standard deduction (RMB 5,000) and other deductions – special additional deductions (where it is applicable), tax-exempt fringe benefits (where it is applicable) – from the non-resident taxpayers’ monthly income amount liable to Chinese IIT;

- Apply the applicable tax rates and quick deductions stipulated in the IIT Withholding Rates Table for Non-resident Individuals.

Annual reconciliation

Resident taxpayers are required to make a settlement during the period between March 1 and June 30 of the following year.

This mechanism applies specifically to the following scenarios:

- Taxpayers deriving comprehensive income from two or more sources, and the balance after deducting special deductions from the amount of annual comprehensive income exceeds RMB 60,000;

- Taxpayers deriving one or more items of comprehensive income from labor services, author’s remuneration or royalties, and the balance after deducting special deductions from the amount of annual comprehensive income exceeds RMB 60,000;

- Taxpayers deriving comprehensive income, and the total tax paid in monthly IIT filings within a tax year is less than the tax payable amount; and

- Taxpayers derive comprehensive income and can apply for a tax refund.

IIT declaration and filing

IIT declaration

We have detailed the circumstances under which taxpayers need to make a tax declaration below:

- The taxpayer obtains taxable income, but there is no withholding agent;

- Non-resident individual derives income from wages and salaries from two or more sources in China;

- Taxpayer obtains comprehensive income and needs to process annual tax reconciliation;

- The taxpayer obtains taxable income, but the withholding agent does not withhold tax;

- Taxpayer obtains overseas income;

- Taxpayer has migrated overseas and cancelled his/her household registration in China; or

- Any other circumstances stipulated by the State Council.

IIT filing

The employer is required to make IIT filing within the first 15 days of the month following the tax withholding either through the IIT system online or submit a Filing Form for Individual Income Tax Withholding to the Tax Bureau in charge.

When the employer pays income to a taxpayer for the first time, it shall complete an Individual Income Tax Basic Information Sheet (Form A) based on basic information such as tax ID provided by the taxpayer and submit it to the tax authorities at the time of tax filing in the following month.

Preferential IIT policies in special regions

To lower the IIT rate and offset the difference with Hong Kong, nine mainland GBA cities have introduced IIT subsidies from 2019 to 2023 (extended to the year 2027). During this period, the portion of the IIT that exceeds 15 percent of the taxable income paid to qualified overseas talent will be refunded as fiscal subsidies.

China Annual IIT Reconciliation – Your Tax Owed Payment FAQs Answered

I am a foreigner working for Company A (in China) in the first half of 2026 with a monthly salary of RMB 10,000, and worked for Company B (in China) in the second half of 2026 with a monthly salary of RMB 15,000. Is it possible that I have tax owed?

Companies serve as the withholding agents and will withhold tax monthly.

When you switch to Company B, Company B shall assume July 2026 as the starting month of your income. Without aggregating your income from Company A, your accumulated income was zero when Company B started calculating your IIT, and you were subjected to a lower tax rate.

At the annual IIT reconciliation, your income from both Company A and Company B shall be combined for calculation, and you shall be subjected to higher tax rates and be required to pay the tax owed. The calculation is demonstrated below.

When Company A and Company B were calculated separately, the withheld IIT in total was RMB 4,380:

|

|

Monthly income (RMB) |

Number of months |

Total income (RMB) |

Total deduction (RMB)* |

Taxable income (RMB) |

IIT |

Tax rate |

|

Company A (January to June 2026) |

10,000 |

6 |

60,000 |

30,000 |

30,000 |

900 |

3% |

|

Company B (July to December 2026) |

15,000 |

6 |

90,000 |

30,000 |

60,000 |

3,480 |

10% |

|

In total |

|

|

|

60,000 |

90,000 |

4,380 |

|

*Here, we only take into account the standard deduction, which is RMB 60,000 per year. In practice, it’s possible that there will be other kinds of deductions, such as special deductions (the individual’s social insurance and housing fund contributions), special additional deductions (children’s education, continuing education, serious illness medical treatment, housing loan interest or housing rent, expenses for elderly support, etc.), or the tax-exempt fringe benefits for foreigners.

After IIT reconciliation, the recalculated IIT payable is RMB 6,480:

|

|

Amount (RMB) |

|

Company A's taxable income |

30,000 |

|

Company B's taxable income |

60,000 |

|

Total taxable income |

90,000 |

|

IIT payable |

6,480 |

|

Tax rate |

10% |

That is to say, the tax owed of RMB 2,100 needs to be paid.

I am a foreigner. I worked for Company A in 2025; my monthly salary was RMB 20,000. I also provided labor service to Company B for the whole year, and my monthly service fee was RMB 20,000. Is it possible that I have tax owed?

Yes, wages and salaries, labor remuneration, author’s remuneration, and royalties are declared separately in the withholding stage but shall all be combined into comprehensive income in the final IIT reconciliation. After the combination, you might be subjected to a higher tax rate.

In the withholding stage, Company A withheld IIT for salary, and Company B withheld IIT for labor service separately. The two companies withheld RMB 57,480 IIT in total.

|

IIT on Salary Income from Company A |

|

|

Monthly income (RMB) |

20,000 |

|

Total income (RMB) |

240,000 |

|

Deduction (RMB) |

60,000 |

|

Taxable income (RMB) |

180,000 |

|

Total IIT withheld (RMB) |

19,080 |

|

Tax rate |

20% |

|

|

Service Fee Withheld by Company B |

|

Monthly service fee paid (RMB) |

20,000 |

|

Deduction per month (RMB) |

4,000 |

|

Taxable income per month (RMB) |

16,000

|

|

IIT per month (RMB) |

3,200 |

|

Total IIT for the service fee (RMB) |

38,400 |

|

|

20% |

In the annual IIT reconciliation, the taxpayer is taxed by aggregating both salary income and income from labor service every year. Incomes are combined and subjected to a higher tax rate of 25 percent. For the whole year, the IIT payable is RMB 61,080.

You shall be required to pay tax owed of RMB 3,600.

|

|

Amount |

|

Taxable income from labor service (RMB) |

16,000*12=192,000 |

|

Taxable salary income (RMB) |

180,000 |

|

Total Taxable comprehensive income (RMB) |

372,000 |

|

IIT payable in total (RMB) |

61,080 |

|

Tax rate |

25% |

What are the consequences if the tax owed is not paid within the time limit? If there was an overdue tax payment of the 2025 annual IIT reconciliation, would it affect my annual IIT settlement for 2026?

If the individual fails to complete the annual IIT reconciliation and payment on time (i.e., before June 30 every year unless it is otherwise stipulated), the tax authority will send a reminder. Where the circumstances are serious, the individuals might be held accountable, and this will be documented on the individuals’ personal tax credit files.

Also, individuals failing to settle their taxes owed in time will need to pay a late payment interest at the daily rate of 0.05 percent on any tax in arrears and may be subject to additional penalties.

Such individuals are not eligible for the 2021 annual IIT reconciliation before they complete the 2020 annual IIT reconciliation and pay the tax owed.

Any final recommendations?

Annual IIT reconciliation is one of the most common topics of concern and confusion among individual taxpayers. Individual taxpayers are recommended to make the annual IIT settlement before the required deadline. Taxpayers who have taxes owed are recommended to pay the tax owed in time according to relevant regulations to avoid unnecessary late fees, fines, and the negative impact on their personal credit record.