Taxation affects almost all aspects of doing business in China. Given China’s distinctive legal system, which is widely different from its Western counterparts, a strong understanding of tax liabilities enables foreign investors to maximize the tax efficiency of their overseas investments while ensuring full compliance with the country’s tax laws and regulations.

The tax system is still evolving at a rapid pace as authorities seek to improve transparency, compliance, and the ease of doing business in the country. Among others, China will accelerate the process of upgrading relevant tax regulations into law, improve the certainty of tax policies, enhance the authority of tax documents, and ensure the efficiency of tax administration.

In this guide, we discuss:

- Tax laws, their administration, and applicability;

- Tax calculation methods for different taxes;

- International taxation;

- Tax incentives for doing business in China;

- Audit and compliance; and,

- Chinese accounting standards.

Summary of tax rates

|

Tax |

Standard Rate |

Variations |

Abbreviation |

|

Corporate Income Tax |

25% |

10%, 15%, 20%, 25% |

CIT |

|

Value Added Tax |

13% |

6%,9%,13% |

VAT |

|

Withholding Tax |

10% |

0-15% |

|

|

Stamp Tax |

0.005%-0.1% |

0.005%-0.1% |

|

|

Individual Income Tax |

3%-45% |

3%-45% |

IIT |

Major laws governing taxation in China

|

Tax Law |

Promulgation Date |

Implementation Date |

|

Law of the People's Republic of China on Customs Duties |

April 26, 2024 |

December 1, 2024 |

|

Stamp Tax Law |

June 1, 2021 |

July 1, 2022 |

|

Deed Tax Law |

August 11, 2020 |

September 1, 2021 |

|

Urban Maintenance and Construction Tax Law |

August 11, 2020 |

September 1, 2021 |

|

Resources Tax Law |

August 26, 2019 |

September 1, 2020 |

|

Vehicle and Vessel Tax (Revised) |

April 23, 2019 |

April 23, 2019 |

|

Corporate Income Tax Law (Revised) |

December 29, 2018 |

December 29, 2018 |

|

Environment Protection Tax Law (Revised) |

October 26, 2018 |

October 26, 2018 |

|

Implementation Rules for the Provisional Regulations of Value-added Tax |

October 28, 2011 |

November 1, 2011 |

|

Value Added Tax Law |

Draft released on December 25, 2024 |

January 1, 2026 |

|

Consumption Tax Law |

Draft released |

- |

|

Property Tax Law |

To be developed |

- |

|

Land Appreciation Tax Law |

Draft released |

- |

|

City and Town Land Use Tax |

To be developed |

- |

Corporate Income Tax in China

The standard CIT rate in China is 25 percent.

This rate is applicable to resident enterprises and non-resident enterprises with income-generating establishments in China. All enterprises (except sole proprietorships and partnerships), including all organizations that generate income in China, are subject to Corporate Income Tax (CIT). Resident and non-resident enterprises are subject to different tax obligations, but the standard CIT rate applied to all companies in China, both domestic and foreign, is 25 percent.

Reduced CIT rates are available based on entity type, size, sector, or location. A reduced CIT rate of 20 percent applies to small and low-profit enterprises (SLPEs) on 25 percent of the taxable income amount for the portion not exceeding RMB 1 million (effective from January 1, 2023 to December 31, 2027), resulting in an effective CIT rate of 5 percent for that income portion. Enterprises that qualify as high-tech enterprises or that operate in certain encouraged sectors or regions (such as Lingang and Hengqin) may be subject to a reduced CIT rate of 15 percent.

CIT is settled on an annual basis but is often paid quarterly, with adjustments either refunded or carried forward to the next year. The final calculation is based on a company’s year-end audit.

Corporate income tax (CIT) is one of the main taxes for businesses. The fundamental regulations on China’s corporate income tax are the CIT Law and its Implementation Guidelines.

Value-Added Tax in China

General taxpayers pay VAT at a rate of 6-13 percent, while small-scale taxpayers are subject to a uniform rate of 3 percent.

Value-added tax (VAT) is one of the major indirect taxes in China.

VAT taxpayers are categorized into general taxpayers and small-scale taxpayers based on their annual taxable sales amount. (The taxable sales here refer to the accumulated VAT taxable sales of the taxpayer during the continuous business period of no more than 12 months or four quarters). Taxpayers with annual taxable sales exceeding the 5 million CNY sales ceiling set for small-scale taxpayers must apply for general taxpayer status.

The fundamental legal framework for VAT in China consists of the Interim Regulation of VAT promulgated by the State Council and its Implementation Guidelines released jointly by the Ministry of Finance and State Taxation Administration. The new VAT Law will enter into force in January 2026.

Individual Income Tax in China

An individual’s comprehensive income is subject to 3 percent to 45 percent of progressive income tax rates.

The IIT Law divides IIT taxpayers into two categories:

- Resident taxpayers refer to individuals who have a domicile in China or individuals who do not have a domicile in China but have resided in China for 183 days or more cumulatively within a tax year.

- Non-resident taxpayers refer to individuals who do not have a domicile in China and have not resided in China, or individuals who do not have a domicile in China and have resided in China for less than 183 days cumulatively within a tax year.

The Individual Income Tax Law of China recognizes nine different categories of income, with several different deductions, tax rates, and exceptions applying to each of them – with foreigners working also eligible for certain fringe benefits.

It is the employer’s responsibility to accurately calculate and withhold individual income tax (IIT) on employment income, including wages and salaries, bonuses, stock options, and allowances, before paying a net amount to its employee.

Withholding Tax in China

The withholding CIT rate for non-tax resident enterprises is 20 percent, which is currently reduced to 10 percent.

Withholding tax (WHT) for CIT is levied on the income of foreign enterprises that do not have a physical establishment in China but provide services to China-based businesses. Any China-derived income arising from such a transaction between an overseas entity and a Chinese business is withheld by the China-based client, deducted from the gross income amount, and taxed by the Chinese tax authorities at a flat concessionary rate.

It is the responsibility of the China-based client to ensure compliance with the withholding tax policies. Not doing so may lead to penalties, and the local tax bureau will take up repayment with the China-based client and not the overseas entity.

Tax incentives in China

Tax incentives are preferential tax policies offered by the government to incentivize or encourage a particular economic activity or to support disadvantaged business owners or individuals. From the investor’s perspective, tax incentives are legitimate tools for reasonable tax planning and cost savings. They are a useful indicator of market trends and government priorities.

There are multiple forms of tax incentives available to businesses, such as tax exemptions, tax reductions, lower tax rates, tax refunds or rebates, tax credits, etc.

Tax incentives are usually based on:

- Type of tax: Such as corporate income tax (CIT), value-added tax (VAT), and individual income tax (IIT).

- Size of business: Such as small and low-profit enterprises, small- and medium-sized enterprises, and small-scale VAT taxpayers.

- Sector-wise: This is to guide industrial upgrades, to support the development of the sector, or to respond to the special characteristics of the sector.

- Region-based: Such as to encourage investments in certain less attractive areas or to give comparative advantages to more economic zones. Or IIT refund policies to attract talent in certain areas.

FIEs and domestic companies can generally apply for tax incentives equally, based on their qualifications, although local governments can offer certain tax incentives at their discretion to attract foreign investment.

Profit repatriation

The most common is for the company’s China-based entity to pay dividends directly to its foreign parent company, which is subject to certain prerequisites.

In accordance with the Company Law of the People's Republic of China, the General Rules on Enterprise Finance and relevant tax laws, profit distribution for enterprises (primarily corporate enterprises) must follow a statutory order. The core process is starting from pre-tax loss offset tax payment, after-tax loss offset, surplus reserve withdrawal, dividend distribution, retained earnings accumulation.

Other Cross-border considerations

Transfer Pricing

China's transfer pricing policy follows international standards (such as the OECD's BEPS Action Plan) and has formed a unique regulatory framework in combination with domestic regulations.

The three primary documentation requirements for transfer pricing in China include the master file, local file, and country-by-country report. These align with the three-tier structure proposed by the OECD, yet China may impose specific additional requirements. For instance, the submission thresholds for the master file and local file, as well as the monetary thresholds for related-party transactions, could differ from the OECD guidelines.

All transactions between the HQ and its China-side entity should be conducted based on the arm’s length principle, as the two are related parties according to Chinese tax laws.

From a transfer pricing perspective, taxpayers have to be aware of their tax filing obligations. This consists of two parts:

- Ensuring that related party transactions are appropriately disclosed in the tax return; and

- Preparing and maintaining detailed transfer pricing documentation, if required.

Being well-versed with various transfer pricing rules can ensure full compliance for companies while still guaranteeing that the transfer pricing process is effective and worthwhile. Besides, setting up a transfer pricing system early in the business cycle helps to mitigate transfer pricing risk exposure and ensure that the enterprise’s adopted system is the most tax-effective, consistent with its commercial objectives, and documented efficiently.

Foreign currency controls

China implements a strict system of foreign currency controls, limiting the inflow and outflow of foreign currency. This system distinguishes between transactions made under an enterprise’s current account item and capital account item, and requires foreign investors to open separate bank accounts for the two.

The State Administration of Foreign Exchange (SAFE) and its local branches are the bureaus in charge.

Customs duties and import-export taxes

Customs duties include import duties and export duties, which are computed either on an ad valorem basis or quantity basis.

Several factors, including preferential taxes under FTA, rates for Most-Favored Nations, lower rates for quota items, and provisional duty rates, affect the amount of customs duty payable for import. Further, export duties are only imposed on a few resource products and semi-manufactured goods.

Import taxes and duties can be calculated after determining the duty-paying value, tax, and tariff rates of the goods.

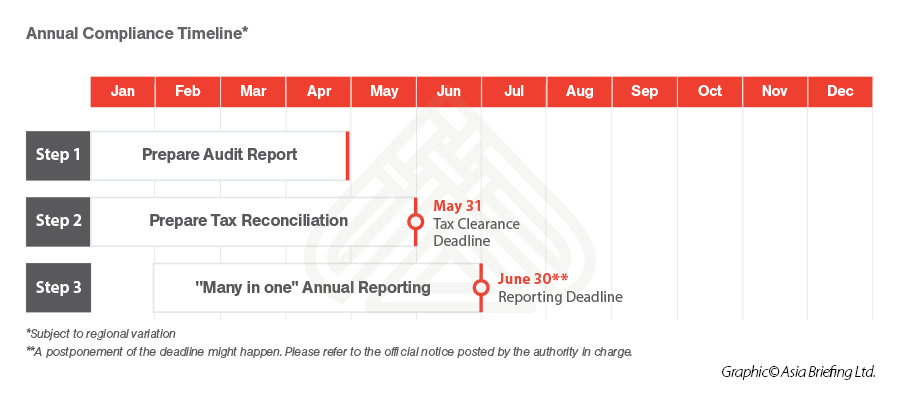

Audit and compliance

China’s company law requires that companies prepare financial accounting reports at the end of each fiscal year. These financial accounting reports should be audited by an accounting firm following the provisions of the law.

A financial audit is an objective examination and evaluation of the financial system and statements of an organization to make sure that the financial records give a true and fair view of the financial position of the company. Most companies conduct a yearly audit of their financial statements – which includes an examination of the income statement, balance sheet, cash flow statement, and statement of changes in equity, among others – as the first step of annual compliance.

This also applies to all FIEs, irrespective of their corporate structure.

Chinese accounting standards

Businesses operating in China are required to follow the Chinese Accounting Standards (CAS), also known as the Chinese Generally Accepted Accounting Principles (GAAP).

The CAS framework is based on two standards:

- Accounting Standards for Business Enterprises (ASBEs); and

- Accounting Standards for Small Business Enterprises (ASSBEs).

The ASBE standards are significantly converged with the International Financial Reporting Standards (IFRS) and all listed companies in China must comply with the ASBEs for the preparation of their financial statements. Most foreign-invested entities also generally follow the ASBEs.

The ASSBEs is a counterpart of the ASBEs, providing unified standards for small-size enterprises. The ASSBEs use the ASBEs as a reference but are more similar to tax laws in terms of their tax calculation methods, which simplify the process of making adjustments between accounting standards and tax rules. Small-scale enterprises can choose to adopt either the ASBEs or ASSBEs.