China CIT Filing 2026: Fix Salary Deduction Errors Before May 31

China CIT salary deduction issues come under heightened scrutiny as the annual CIT reconciliation deadline of May 31 approaches. Misclassification of salaries, bonuses, and employee welfare expenses can have a cascading impact on multiple deduction caps under China’s CIT rules. This article explains where salary‑related risks commonly arise and how employers can correct them before filing.

Salary and employee‑related expenses are among the most closely reviewed items in China’s annual corporate income tax (CIT) filing. In practice, classification errors are rarely isolated. A single misstep in treating wages, incentives, or allowances can distort the calculation bases for employee welfare fees, staff education funds, and union dues.

As a result, salary‑related compliance issues remain one of the most frequent triggers for post‑filing CIT adjustments. Beyond disallowed deductions, companies may face late payment surcharges and increased scrutiny in subsequent tax years. Proper classification, consistent accounting treatment, and robust supporting documentation are therefore critical to managing tax exposure.

This article provides a practical self‑check for employers ahead of the filing deadline, highlighting common salary deduction pitfalls and outlining how to align payroll‑related tax treatment with current regulatory expectations.

The Deadline Is May 31: Get Expert Eyes on Your Filing Now

Our China tax advisors can review your salary classifications, welfare expense calculations, and dispatch cost treatment before you submit.

- Salary reasonableness review

- Welfare expense classification

- Labor dispatch cost split

- Full CIT reconciliation support

To arrange a free consultation, please contact China@dezshira.com.

Can salary and wage expenses be deducted before tax?

Yes, salary and wage expenses can be deducted before tax in full, provided they are “reasonable”. Article 34 of the Implementing Regulations of the Corporate Income Tax Law permits full pre-tax deduction of reasonable salary and wage expenditure. There is no percentage cap or fixed ceiling, unlike welfare expenses.

The definition of salary and wages is deliberately broad. It covers all forms of employee compensation paid during the tax year, including basic salary, bonuses, allowances, subsidies, year-end increments, overtime pay, and any other cash or non-cash remuneration directly tied to employment. The word “reasonable” does all the heavy lifting –size alone does not disqualify a deduction.

Why this matters for reconciliation:

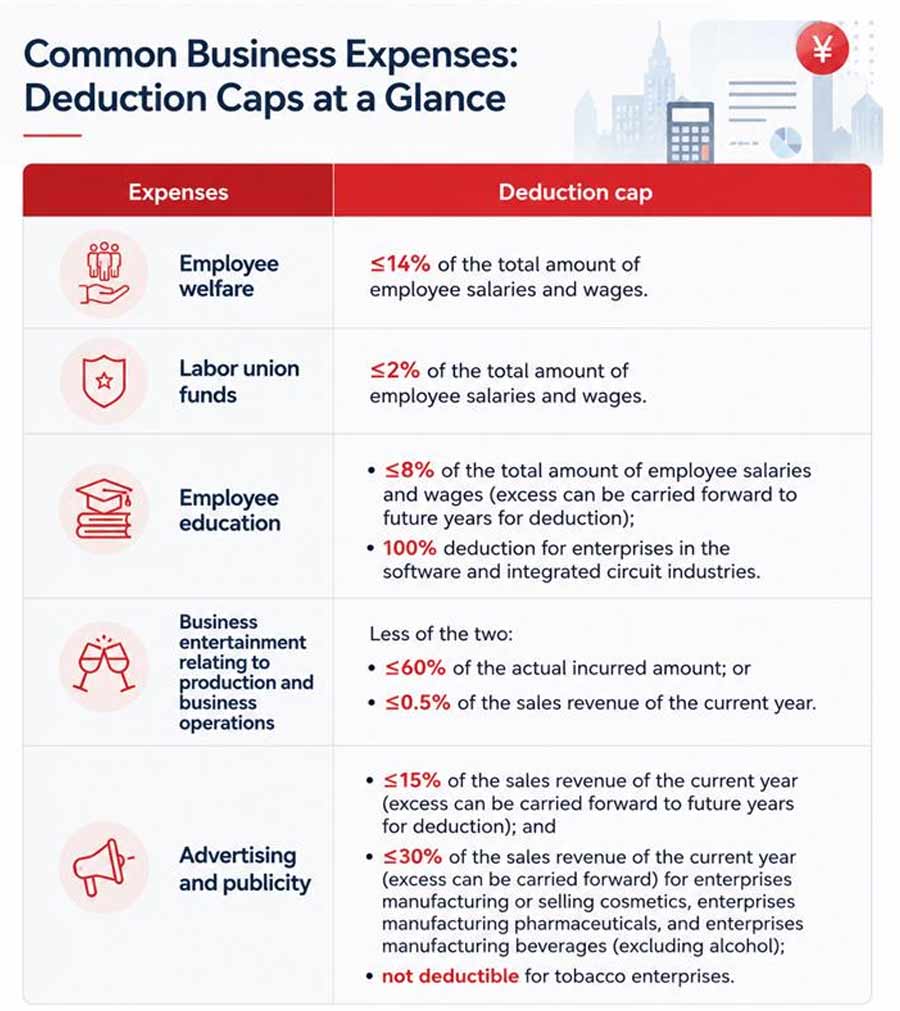

Total salary is the base figure from which welfare expense (14%), education expense (8%), and union fee (2%) ceilings are calculated. An understated salary base shrinks all three downstream deductions simultaneously.

What makes a salary “reasonable”?

A salary is considered reasonable when it is actually paid to employees under a structured compensation policy established by an authorized body, such as the shareholders’ meeting, board of directors, remuneration committee, or equivalent management body.

Tax authorities assess reasonableness against five criteria:

- The company operates under a documented, formal salary policy

- Compensation levels are consistent with industry and regional benchmarks

- Salaries are relatively stable over time, and any adjustments are orderly and traceable

- The company has withheld and remitted individual income tax (IIT) on all payments

- The salary arrangement is not structured to reduce or evade tax

Pre-filing check:

Confirm your compensation policy document is signed by the authorizing body and on file. Then, cross-check the IIT withholding records against the actual payroll. A gap between the two is one of the most common audit triggers.

How is “total salary base” defined?

The total salary base is the sum of salaries and wages actually paid by the company during the year. It explicitly excludes the following, which are calculated separately:

- Employee welfare expenses

- Employee education expenses

- Union fees

- Social insurance contributions (pension, medical, unemployment, work injury, maternity)

- Housing Fund contributions

Welfare allowances: Deduct as wages, or as welfare expenses?

This will depend on how the employee’s welfare allowance is structured and paid. Under SAT Circular Guoshuihan [2009] No. 3, tax treatment turns on two cumulative conditions, both of which must be satisfied:

- First, the allowance must be explicitly provided for in the company’s formal compensation policy or internal remuneration rules.

- Second, it must be paid on a fixed and regular basis, together with the monthly salary, rather than on an ad hoc or discretionary basis.

If both conditions are met, the allowance may generally be treated as salary and wages, allowing it to be deducted in full for CIT purposes. However, if either condition is not satisfied, the payment is typically regarded as an employee welfare expense, meaning its deductibility is subject to the 14 percent statutory cap based on the company’s total wage base.

Common grey area: Transport subsidies, meal allowances, and phone allowances all look similar but may be treated differently depending on how they are structured and paid. Review each item individually before filing, and document the policy and the payment cadence for every allowance you intend to classify as wages.

Labor dispatch costs: Salary, service fee, or both?

The tax treatment of labor dispatch costs depends less on the employment arrangement itself and more on who ultimately receives the payment. In CIT practice, dispatch‑related payments may be treated as service fees, salaries, or welfare expenses, each with different deductibility consequences. Getting this classification wrong can affect not only current‑year deductions, but also the calculation of multiple downstream deduction ceilings.

| Payment Recipient | Tax Treatment | Counts Toward Salary Base? |

| Labor dispatch company (per contract) | Service fee — deduct as labor cost | No |

| Directly to individual workers (wage nature) | Salary and wages — deductible in full | Yes |

| Directly to individual workers (welfare nature) | Welfare expense — subject to 14% ceiling | No |

The portion classified as salary and wages counts toward the total salary base, which in turn determines the ceilings for welfare, education, and union fee deductions. Misrouting dispatch payments to the service fee category permanently shrinks those three downstream deductions.

Pre-deadline self-check before May 31

Before submitting the annual CIT reconciliation, companies should conduct a focused review of salary‑related items that frequently trigger tax adjustments:

- Compensation policy in place: Ensure a formal, written compensation policy is on file, approved by the board or shareholders’ meeting, and clearly covers all salary components, allowances, and payment frequencies.

- IIT withholding fully reconciled: Verify that all payroll payments can be matched to corresponding IIT withholdings and remittances. Any timing differences or exceptions should be clearly documented and justifiable.

- Salary base correctly calculated: Confirm that the total salary base used for deduction caps excludes social insurance and housing fund contributions, and that welfare‑type allowances are assessed and classified individually.

- Labor dispatch costs properly split: Check that payments made to labor dispatch agencies and amounts paid directly to workers are clearly separated in accounting records and classified according to their economic substance.

A focused review of these areas before filing can help reduce the risk of post‑submission adjustments, limit late payment surcharges, and ensure salary‑related deductions are aligned with current regulatory expectations.

See also:

- As a Foreign Company, Do I Need to Make Annual CIT Filing in China?

- Annual CIT Reconciliation in 2026: Key Areas to Focus

- China Issues Updated Rules on Tax Deduction for Advertising and Promotion Expenses

Tax planning and compliance in China can be complex and fast-changing. Our experienced advisors help businesses manage corporate tax, indirect tax, individual tax, international tax, and transfer pricing across China’s diverse regions.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article IR56B Common Errors: A Guide to Avoiding IRD Follow-Up in Hong Kong

- Next Article China Public Holiday Schedule 2026