China Clarifies Issues Related to New IIT Law

Aug. 9 – Following amendments to China’s Individual Income Tax (IIT) Law, which are scheduled to come into effect from September 1 this year, China’s State Administration of Taxation (SAT) made a new announcement on July 29 with regards to the revised IIT Law. The document specified how taxpayers will be subject to the old and new tax rates during different times of the tax year and how IIT on the income of individual businesses shall be calculated.

The “Announcement on Issues Related to the Implementation of the Revised IIT Law (SAT Announcement [2011] No.46)” clarified the following issues:

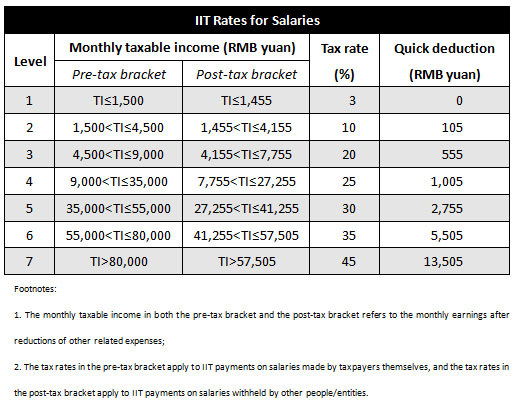

Standards of IIT exemption threshold and tax rates for salaries

The salaries taxpayers receive on and after September 1, 2011 are subject to the new IIT exemption threshold of RMB3,500 and tax rates listed in the following chart.

The IIT on salaries earned before September 1, 2011 shall be subject to the old IIT exemption threshold and tax rates, regardless of whether or not the actual tax payments have been made.

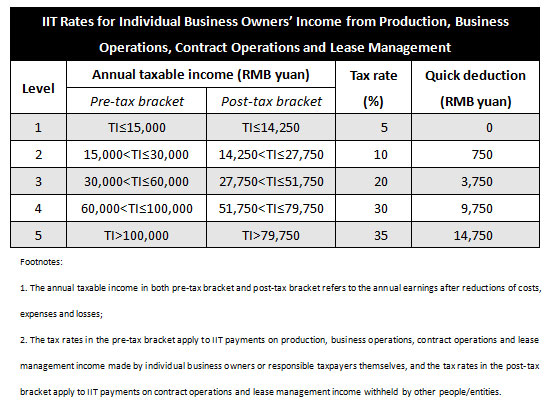

Calculation of individual business owners’ taxable income from production and business operations

IIT on production and business operation income earned by individual business owners, sole proprietors, and investors/partners of partnership enterprises on and after September 1, 2011 shall be subject to the IIT exemption threshold and tax rates stipulated in the revised IIT Law. The IIT rates for individual business owners are as follows:

Individual business owners shall calculate their taxable income of 2011 first before figuring out the amount of their IIT payments for the year. They shall calculate the amount of IIT payments of 2011 according to the following formulas:

- IIT of the first eight months = (Annual taxable income × Corresponding tax rates in the IIT Law before revision – Quick deduction) × 8/12

- IIT of the last four months = (Annual taxable income × Corresponding tax rates in the revised IIT Law – Quick deduction) × 4/12

- IIT of 2011 = IIT of the first eight months + IIT of the last four months

Taxpayers shall settle 2011’s IIT payments within three months after the year ends.

The amount of IIT that contractors and lease managers for enterprises should pay shall be calculated in the same way.

The Announcement will take effect on September 1, 2011. From this date, the expired tax rate charts from the previous SAT Announcement (guoshuifa [1994] No.89) will be repealed.

Dezan Shira & Associates is a boutique professional services firm providing foreign direct investment business advisory, tax, accounting, payroll and due diligence services for multinational clients in China. For advice, please email tax@dezshira.com, visit www.dezshira.com, or download the firm’s brochure here.

This article is also available on Dezan Shira & Associates’ online business resource library. To view the article, and other regulatory updates, please click here.

Related Reading

Doing Business in China

Doing Business in China

Our 156-page definitive guide to the fastest growing economy in the world, providing a thorough and in-depth analysis of China, its history, key demographics and overviews of the major cities, provinces and autonomous regions highlighting business opportunities and infrastructure in place in each region. A comprehensive guide to investing in China is also included with information on FDI trends, business establishment procedures, economic zone information, and labor and tax considerations.

The China Tax Guide (Fifth Edition)

The China Tax Guide (Fifth Edition)

This popular book, fully updated with all recent tax changes and amendments, details all taxes in China affecting businesses and individuals, how to calculate the amounts due, tax registration and filing procedures, tax minimization techniques, and claiming VAT rebates. It also details good financial management techniques, handling negotiations with the tax bureau and annual audit and compliance procedures.

Individuals Subject to IIT Payment When Terminating Investments

Foreign IIT Exemption Threshold to Remain the Same

NPC Passes IIT Revisions, Lifts Tax Exemption Threshold to RMB3,500

Individuals to Pay IIT on Gifts Received from Businesses

Hong Kong to Return 75% of Salaries Tax to 1.5 Million Tax Payers

SAT Clarifies IIT Collection Method for Lump-sum Bonuses

SAT’s New IIT Collection Measures to Focus on Foreigners

- Previous Article Roles and Responsibilities of the China Chief Representative

- Next Article Tax Policy Clarification Released for China’s Western Region