China Makes Up US Trade War Deficit by Buying from ASEAN, Belt and Road Countries

China is balancing the US trade slowdown with more bilateral trade with ASEAN and Belt and Road Initiative countries.

Op/Ed by Chris Devonshire-Ellis

The trade war instigated by US President Trump is having an effect – but it’s not one that Washington DC will like to hear. The issue has just begun to sink in as the US deferred the latest round of tariffs to until December. Postponing the tariffs will do little to alter China’s new trajectory. The simple truth is that China’s share of bilateral trade with Belt and Road Initiative (BRI) countries, coupled with increasing trade with ASEAN, is more than compensating for any US trade downturn. This is why Chinese President Xi can afford to be ambivalent about the latest round of tariffs slapped on Chinese products to the US. It is also why Washington DC appears to be having second thoughts.

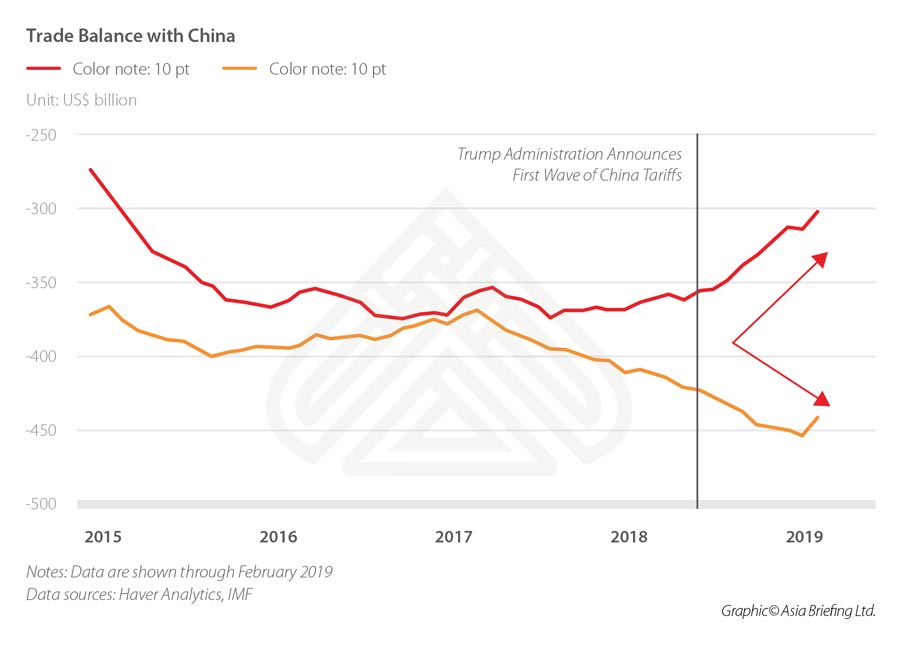

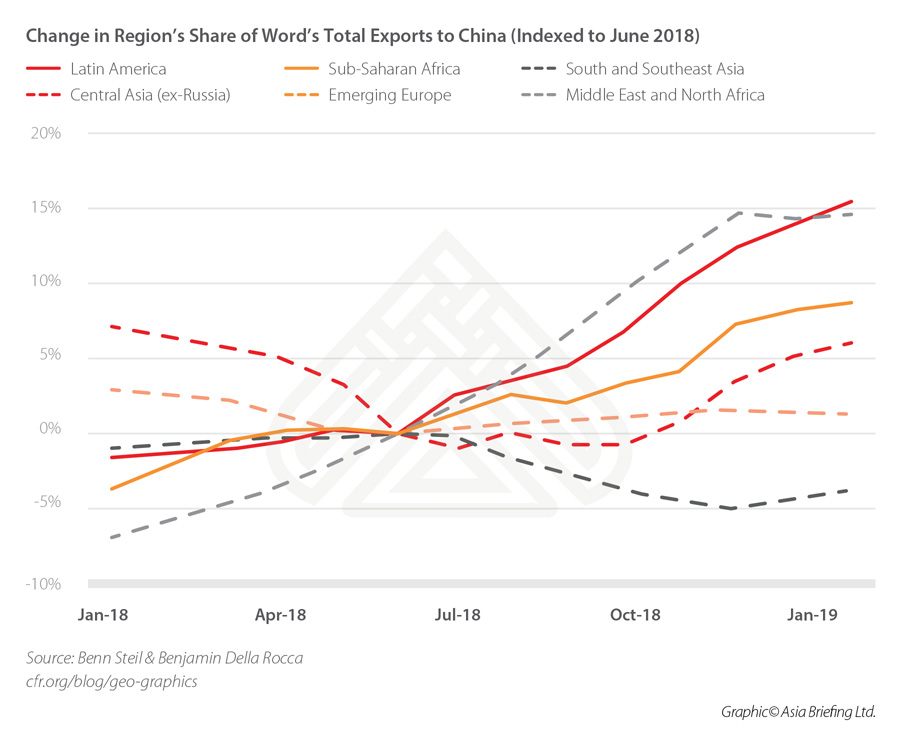

While reducing its US imports, China has instead bought more from other countries, and especially from BRI countries. The big winners have been African and Latin American countries, many of which signed off on BRI MoUs last year. This can be seen in the graphic below, which shows a huge increase in Chinese buying from alternative markets and US purchases declining significantly over the year.

In fact, the US tariffs on Chinese exports have had the opposite effect to that intended when President Trump stated his actions would reduce the Chinese trade deficit with the US. When the tariffs began, China instead pressurized its businesses to find alternative suppliers, which increased the China trade deficit with the US to just two percent of GDP. In the opposite direction, the US global trade deficit has expanded by eight percent, while the emerging market trade balance with China has moved towards a surplus – great news for ASEAN and BRI signatories.

This re-balancing is also something we have seen within Dezan Shira & Associates. Although we have a significant US client portfolio, we are not experiencing that many issues. Clients engaged in China trade have been evolving. Our firm has clients from some 70 different countries – and 69 of them do not have tariff disputes with China. China-ASEAN bilateral trade is up 4.2 percent year-on-year and hit US$293 billion in the six months to June 2019, while ASEAN became China’s second largest trade partner during that time. What is taking place is effectively an American decline. US products and services being sold to China are gradually being replaced by those from Eurasia.

Alberto Vettoretti, Managing Partner of the firm in China, states “ASEAN and China trade volumes have been growing for quite some time so this will likely intensify going forward. Red hot destinations include Indonesia, Singapore, and Vietnam, which are all heavily involved in how supply chains and trade are moving across the region, while Thailand and the Philippines are also experiencing large growth volumes.”

ASEAN nations are also experiencing high GDP growth rates this year as a result.

This is easily explained by China’s Free Trade Agreement with ASEAN, which has deleted tariffs on some 95 percent of all products and services traded between them. Someone in Washington DC didn’t do their homework: China has free trade options to the US, and only needed to increase purchases.

In terms of the BRI, China has not only been busy signing MoUs with interested nations, it has been going a step further by committing to a lengthy series of Double Tax Agreements, which also reduce taxes on specific products on a case by case basis. How far this extends can be seen below.

This explains why China has been buying more products from emerging markets.

Additionally, China is now at a stage with the BRI when it actively wants foreign, third-party participation. This was specifically catered for in the latest additions to China’s Foreign Investment Law, which allowed foreign participation in public procurement projects for the first time. I discussed this in the article, “China’s New Foreign Investment Law and the Impact on the Belt and Road Initiative”. I also discussed the Top 20 BRI countries purchasing from China in the article, “The Main Buyers of China’s Belt and Road Initiative Materials.”

However, there are other regional advantages coming into play as well.

The BRI will almost certainly make China more prepared than the US when it comes to waging tariff wars. For example, Chinese businesses have been heavily investing in Africa over the past five years, establishing subsidiaries throughout the continent. These companies are domiciled as African, and are now poised to take huge trade advantages from the recent African Continental Free Trade Agreement (AfCFTA), which removes tariffs of 90 percent on all products traded across Africa. With DTAs also in place with many African countries, Chinese businesses are beginning an African trade bonanza. I wrote about the impact this would have in the article, “China’s African Moves through the Belt & Road, Double Tax Treaties, and AfCFTA”. So much for what President Trump dismissed as “shithole countries.” They are now replacing US producers for the China market.

It’s a similar, if rather more diverse story in South America, which I covered in the article “China’s Belt and Road in South America”, where countries, such as Venezuela, Guyana, Suriname, Ecuador, Bolivia, Uruguay, and Chile have all signed off on China’s BRI. It is a developing scenario, but one that can be expected to accelerate in terms of DTA and BRI trade in coming years. China has not yet made roads into Central America, so as not to overly push the US too far, but as Trump continues to build his wall with Mexico, these countries may feel better off under trade generated with Beijing rather than Washington DC. My comments on this can be read in the article, “China’s Belt and Road in Mexico and Central America”. These current, and almost guaranteed, trade partners with China will find trade opportunities with Beijing as Washington DC rejects them.

It’s a similar “in progress” story across Eurasia, where the two competing blocs are Brussels and Moscow. Moscow is the leading partner in the Eurasian Economic Union, which includes Armenia, Belarus, Kazakhstan, Kyrgyzstan, and Russia itself. While that might sound an unlikely grouping, it wields real geopolitical influence as it effectively covers a land mass that stretches from China to the borders of the EU.

The development of the EAEU is catching many analysts by surprise. The EAEU-China FTA signed last year was largely dismissed in academic and trade circles as it was non-preferential, meaning it didn’t include any specific categories of goods. However, this rather misses the point – getting the FTA arrangement started is the salient point, as products can simply be added at a later date, without the need for intensive negotiations. This means the China-EAEU FTA can roll-out the product specifics when China and Russia determine the time is right. In Trumpian terms, it is in fact “locked and loaded” – all that is needed is the addition of product categories. When enacted, it is likely to take many analysts by surprise, and it is already apparent that Russia and China are negotiating a product and service specific FTA between them and the members of the EAEU right now, as confirmed by presidents Xi and Putin in May.

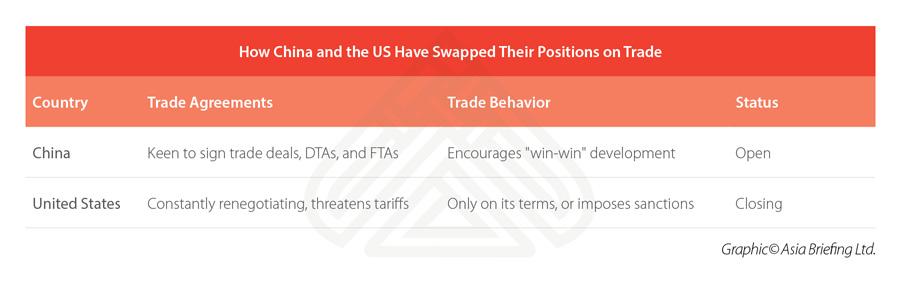

These differing paths between China and the US effectively means their respective positions have swapped.

The impact of the US-China tariff war will long be felt, and especially by US citizens and US companies overseas. Many of the latter, however, are already adapting to life externally from a US-based perspective. Some will become far more global and cease being “American” businesses in all perhaps but name.

However, what does now seem apparent, when trade figures, and developments instigated by China, become more clear, is that the trade war is effectively already over. The sad thing about the US is that as China’s national purchasing strategy has changed, and it shifts its supplier base away from the US, those American businesses are highly unlikely to get that China market share back.

Asia is far closer, more predictable, and acts with rather more trade sustainability than Washington DC trade policy appears capable of providing. Global businesses need to have sustainable and predictable logistics and trade relationships in place to continue to provide a demanding and rapidly growing worldwide market.

It is unfair to place this all upon Trump’s shoulders; the decline has been there for some time. The US, generally, has been overly bombastic about its own strengths, while neglecting the hard work and efforts that need to be put in place on the ground.

This includes a shocking neglect of bilateral trade ties, agreements, and investment treaties, some of which are still current, despite being 20 years out of date. The increasingly odious talk of American superiority has drowned out the real diplomatic work that underpins ongoing relations, which have been relegated to an afterthought amid all the pro-US bombast.

Instead, that calm, longer term global strategic diplomatic play is now being provided for by China, while the US is rapidly being relegated to the status of an unpredictable market, and one in which the extension of the deadline of imposition of further tariffs on Chinese products until December only serves to prolong the uncertainty.

Instead, the smart money is investing in China, ASEAN, and the emerging markets of the BRI. It is important to be on the right side of history in this struggle, and that increasingly means working with and properly understanding a sustainable and predictable China – and the trade initiatives it brings along for the ride.

About Us

China Briefing is written by Dezan Shira & Associates. Chris Devonshire-Ellis is the Founding Partner. The firm assists foreign investors throughout Asia and has done since 1992, servicing clients from offices across China, Hong Kong, ASEAN, India, and the Belt & Road. Please contact us at china@dezshira.com or visit us at www.dezshira.com.

- Previous Article Investing in India’s Maharashtra State, Vietnam’s Port Infrastructure – China Outbound

- Next Article In Trump’s Remodelling of the US, the North Pole is in China