China’s Agreement with ASEAN – What it Means for China-Based Foreign Manufacturers

China’s growing consumer market to be serviced from Asia

Op-Ed Commentary: Chris Devonshire-Ellis

China agreed to a full Free Trade Agreement with ASEAN, effective from 2010, yet the implications of this, given the preoccupation with the global financial crisis, are only now starting to become apparent. What this agreement does is to eliminate import-export tariffs and barriers on some 90 percent of all products traded between China and the ASEAN member states. ASEAN is a ten member Asia trade bloc, including the Asian Tigers of Singapore, Indonesia, Malaysia, Philippines and Thailand, all of whom have already reduced tariffs (and China has done in reciprocity) on the majority of traded products between them. By the end of next year, the same will also apply to the other ASEAN members of Cambodia, Laos, Myanmar and Vietnam.

The reason this is important is almost entirely an economic exercise. While the full impact of the economics behind the China-ASEAN FTA has yet to be felt by foreign investors, it is already starting to change the way the global supply chain operates – and this has huge implications for global manufacturers, especially those operating in China.

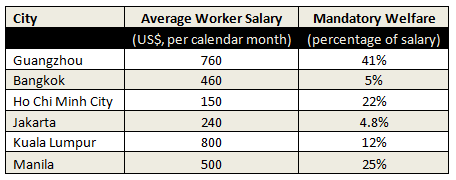

China, as has been mentioned many times in the media, is becoming far more expensive to manufacture goods. Wage levels have been increasing by leaps of 15-20 percent per annum for the past five years, and this trend is set to continue. What isn’t often recognised is that the total cost in employing Chinese workers is increasing as well – China imposes mandatory welfare payments on employers for hiring permanent staff, and these payments – typically amounting to between 40-50 percent of the total salary cost – are directly linked to that expense. Therefore, if wages go up – so does the mandatory welfare.

When assessing ASEAN’s potential, however, it is important to differentiate between the bloc’s capabilities. Singapore is essentially a service hub, and although it does possess some manufacturing capabilities, is not typically a destination for lower-cost production; its role is in regional management. Brunei is almost exclusively an oil and gas play, while the smaller ASEAN economies of Cambodia, Laos and Myanmar are still infrastructure poor and unlikely to be able to handle sustainable quality production at this time.

For this reason, in this study I focus on the more developed ASEAN economies of Indonesia, Malaysia, Philippines, Thailand and Vietnam. They are all having a large effect on the regional financial competitiveness of skilled workers when compared as follows:

Notes: Guangzhou welfare can vary depending upon amount of housing fund contribution. Shown is the mean average. All other country welfare figures can vary depending on a number of circumstances. Shown are the typical contribution rates paid.

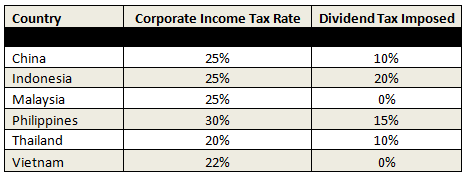

Over the past twenty years, much of the global supply chain moved to China to take advantage of well organised infrastructure, cheap labour and low tax rates. However, with tax reform a few years ago increasing corporate income tax to 25 percent from 15 percent, and additionally imposing a dividend tax of 10 percent on foreign manufacturers in China, the tax benefit as well as the cheap labour benefit have now disappeared. China now compares with its regional rivals as follows:

Notes: Vietnam to further reduce its CIT rate to 20% from 2016. Dividend Taxes can further be reduced by 50% if applicable DTA is invoked. For more information, click here.

In all cases, these competitive tax burdens coupled with lower labour costs are now making the overall cost of manufacturing in China less competitive than the major ASEAN economies. Yet a mass departure of foreign investors from China has not occurred, although there has undoubtedly been some leakage. The reason for this is the upside to the increasing labour costs of China – the development of a considerable middle class consumer market.

Today, China has a middle class consumer market of about 250 million people – yet in what will become one of the fastest growing wealth trajectories ever seen, that number is set to increase to 600 million by 2020 – just six years from now. This means that factories already extant in China and servicing the China market are not relocating – these same factories possess and are continuing to build their China supply chains to reach out to the new Chinese consumers. But what is happening is that the additional manufacturing capacity that is gradually being required to service China is being repositioning elsewhere – and it is a direct consequence of the China-ASEAN FTA that it is doing so. Nearly all import duties from the ASEAN nations featured above have largely been eliminated. Vietnam follows suit in December next year.

This now means a double-pronged strategy is being developed by many companies intent on servicing the Chinese market. The intention is to develop a strategic hub in China, which may include some manufacturing, and which definitely needs to sit tight on the supply chain management, while combining this with production of either component parts or the complete product sourced from other factories within ASEAN.

Here, there seems to be a general rule of thumb, at least amongst Dezan Shira & Associates’ own clients – if the non-China production can reach 70 percent of the level that can be achieved by the China factory, it usually makes good sense to house your production in the non-China facility. That production gap is only going to close as regional infrastructure improves.

We have already seen Foxconn announce they are to up sticks from China and gradually relocate to Indonesia. With a workforce of over one million, the China price of manufacturing components for Apple is becoming too high for the end product to remain globally competitive. Indonesia, as part of the China-ASEAN FTA, provides a solution. Others will follow.

The implications are clear. As the Chinese economy moves from an export manufacturing base to a consumer driven model, production facilities driven by lower labour and tax overheads elsewhere in Asia will emerge to take up the challenge. China’s Free Trade Agreement with ASEAN dictates that the main beneficiaries of this will, over the next decade, be Indonesia, Malaysia, Philippines, Thailand and Vietnam. Foreign manufacturers based in China will need to establish the benefits of placing increased manufacturing capacity to service the China market, and a resurgent export market, from these countries in ASEAN in particular.

Chris Devonshire-Ellis is the Founding Partner of Dezan Shira & Associates – a specialist foreign direct investment practice providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in emerging Asia. Since its establishment in 1992, the firm has grown into one of Asia’s most versatile full-service consultancies with operational offices across China, Hong Kong, India, Singapore and Vietnam, in addition to alliances in Indonesia, Malaysia, Philippines and Thailand, as well as liaison offices in Italy and the United States.

For further details or to contact the firm, please email china@dezshira.com, visit www.dezshira.com, or download the company brochure.

You can stay up to date with the latest business and investment trends across Asia by subscribing to Asia Briefing’s complimentary update service featuring news, commentary, guides, and multimedia resources.

Related Reading

Why ASEAN is Appealing for Manufacturing as Costs in China Keep Rising

Philippines Poised for Foreign Investment Sweet Spot

Malaysia’s 2013 FDI Soars to Record High

Made in ASEAN: Vietnam Cuts Import Taxes for ASEAN-made Vehicles

Indonesia Prepares For Demographic Changes

Understanding ASEAN’s Free Trade Agreements

- Previous Article China in Asia Round Up – February 2014

- Next Article Dezan Shira & Associates Global Speaking Events – March 2014