China’s GDP Growth – More Shocks Ahead

Last week China released its GDP growth figures for Q3 2015. Officially stated as being 6.9 percent, this marked the lowest period of growth in China since the beginning of the Global Financial Crisis in 2007. Most analysts merely shrugged these figures off as being far better than what both the United States and EU are producing, while others have begun to raise doubts over whether China’s growth figures have ever been especially accurate. It remains true that much of China’s 10 percent plus growth over the past two decades has been fueled by development and building – not all of it successfully. Large swathes of empty buildings occupy most Chinese cities today.

While GDP growth is just one way of examining the health of China’s economy, the issue of how accurate these official figures are is one that does now start to become more pressing. China’s growth rates impact upon the international investment strategies of all MNCs, and getting this right is a balancing act that all boards of directors have to go through lest they face the wrath of their shareholders. Over-investment in China, however, can have a stultifying effect on other emerging markets, such as India, parts of ASEAN, and even into Central Asia, the Middle East and Africa that could perhaps offer better rates of return, should that money be free to invest elsewhere.

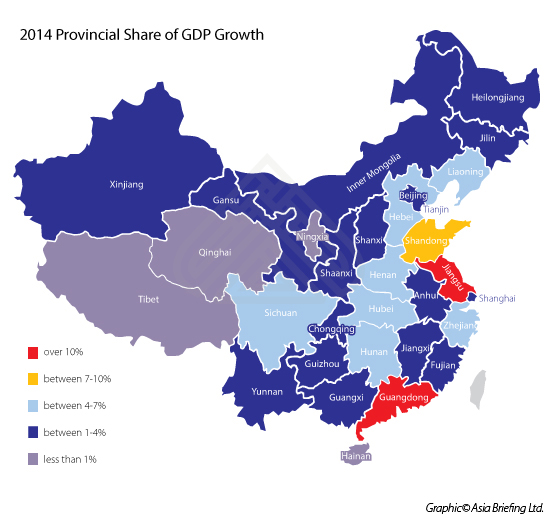

In terms of China as a whole, we can look at the percentage of GDP that each Province provides to China’s total in this graphic:

These figures date from 2014 and are presented in our graph format from data published by the China National Bureau of Statistics. There are no real surprises here: much of China’s total GDP continues to be provided by various Star Provinces along the South-East Coast, as has been the case for much of the past 20 years. What is surprising however is that just three of China’s Provinces – Shandong, Jiangsu and Guangdong – combined provide approximately 30 percent of China’s total output, with another seven making up most of the national balance. With a combined 32 Provinces, SARS and Municipalities, this indicates that only a third of them were actually productive in 2014. The rest were just ticking over, and essentially only producing as much as they locally consume. Of these Provinces, it should be noted that they form a protective ‘ring’ around the Eastern seaboard. The true core of China, it can be suggested, only extends along the east coast from Beijing to Guangdong.

There are some China political and development issues here. Firstly, with Shandong being a major supplier to the Japanese markets, it may not be wise for Beijing to continue to pick at the Japanese from the diplomatic perspective. The Province, largely agricultural-based, contributes the third highest Provincial share of China’s total GDP.

Of the essentially non-productive Provinces, it is also interesting to note that these spread out away from Beijing, Shanghai and the South Coast and essentially hug China’s land borders. That such a massive swathe of land, stretching from the North-East and borders with Russia and Mongolia, West to Kazakhstan and South to border Vietnam and the potentially lucrative ASEAN markets, indicates China has not been successful yet in developing its overland trade. That may change with the instigation of China’s new Silk Road Economic Belt, but this will take time.

Of more immediate concern is China’s constant attention to border disputes. What is little known is that these exist with every country that has land borders with China, including North Korea and Russia. If China is serious about getting its border areas productive, it needs to reach a great deal of agreements to settle its border and maritime disputes with its neighbors. If not, these entire regions, including the increasingly important South-East Asia access, are likely to remain retarded. Growth in these massive regions must involve more local input and not be purely directed by Beijing. A disconnect between Beijing’s Foreign Ministry, the Ministry of Commerce, and getting growth into China’s outward Provinces seems apparent, and needs resolving.

Moving forward to the end of 2015, a number of interesting developments have occurred over the year. With offices serving foreign investors scattered throughout the country, Dezan Shira & Associates is a useful benchmark in terms of assessing client behavior as to how the Chinese economy fared. North-East China, to be frank, took a battering, and especially the automotive led Province of Liaoning. Businesses in China’s North-East are closing down and laying off staff. Tianjin too, the main operational hub for Northern and Far Western China as its operational Port, will show relatively good 2015 figures, but the reality is that since the chemical explosions a couple of months ago, both foreign and local investors are leaving. That is a very serious matter for the Chinese government to contend with, as Tianjin is one of its most important national Ports. Beijing too is suffering – long term expats may not be leaving China (although many are repositioning themselves around Asia, especially in ASEAN) – but many Beijingers are becoming Shanghai based instead. Clearly, China’s environmental promises made during the 2008 Olympics proved to be empty words.

Shanghai meanwhile appears to be fine, while performances in South China by foreign investors are somewhat erratic. Many FIEs located in Guangdong are growing their businesses out to countries such as Vietnam and downsizing their China operations.

This is also backed up by the following graphic, taken from data from the China Economic Review that calculates relative provincial and per capita GDP:

While the majority of media and analysts tend to concentrate on China’s national GDP growth figures, in reality these statistics are purely a mean average. It is far more instructional to examine what is going on in China on a regional basis. However, what is interesting here is that although China has declared an annual target of 7.8 percent GDP growth for 2015, even last year it appeared this was not going to happen. Only three of China’s Provinces – Shandong, Henan and Guangdong – achieved growth in excess of 7 percent. Another three – Sichuan, Hebei and Jiangsu – achieved growth between 5-7 percent, while all others fell way below that 7.8 percent target. The figures shown appear to indicate that China’s actual GDP growth in 2014 was probably closer to the 4 percent mark. With the slowdown continuing and spreading during 2015, it is not beyond the realms of probability that 2015 GDP growth in China will be around the 3 percent mark; some way short of the 7.8 percent official target, which is probably close to the official figure that Beijing will suggest its economy reached.

This has implications for foreign investors in China. While there are growth hotspots, and Guangdong, Shanghai and the Yangtze River Delta and Shandong all look positive and should remain productive, businesses operating in other parts of China will have to batten down the hatches and remain operational rather than grow. This is of course nothing new, it is merely an indicator that China is indeed going through a transformational phase and that it needs to pass through this period of lower growth first. China, it appears, in becoming a market driven economy is following the same development patterns as economies such as the United States and Europe – who themselves on occasion have even gone into recession. It is likely that some entire Chinese Provinces are already in that mode, and investors need to prepare for their 2016 investments and take a hard look at the immediate two year potential for the PRC.

Later in the week I shall examine the GDP growth patterns for ASEAN, including Vietnam, as well as India to provide clues as to whether the China alternatives really exist, and whether or not, when faced with a realistic China GDP growth rate of 3 percent, it makes sense to be looking elsewhere in Asia for business opportunities during 2016.

|

Chris can be followed on Twitter at @CDE_Asia. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

|

![]()

An Introduction to Doing Business in China 2015

An Introduction to Doing Business in China 2015

Doing Business in China 2015 is designed to introduce the fundamentals of investing in China. Compiled by the professionals at Dezan Shira & Associates, this comprehensive guide is ideal not only for businesses looking to enter the Chinese market, but also for companies that already have a presence here and want to keep up-to-date with the most recent and relevant policy changes.

Importing and Exporting in China: a Guide for Trading Companies

In this issue of China Briefing, we discuss the latest import and export trends in China, and analyze the ways in which a foreign company in China can properly prepare for the import/export process. With import taxes and duties adding a significant cost burden, we explain how this system works in China, and highlight some of the tax incentives that the Chinese government has put in place to help stimulate trade.

How to Restructure an Underperforming Business in China

In this issue of China Briefing magazine, we explore the options that are available to foreign firms looking to restructure or close their operations in China. We begin with an overview of what restructuring an unprofitable business in China might entail, and then take an in-depth look at the way in which a foreign company can go about the restructuring process. Finally, we highlight some of the key HR concerns associated with restructuring a China business.

- Previous Article IMF Warning – China To Experience Mass Corporate Bankruptcies

- Next Article The U.S. TPP “Yarn Forward” Program and Implications for China & Vietnam