China’s Labor Market in 2026: Wage Realignment, Mobility Shifts, and the New Talent Map

China’s labor market in 2026 rewards precision over scale: hiring decisions now hinge on role criticality, location strategy, and long-term workforce structure. Wage pressure is increasingly concentrated on specific skills, cities, and functions.

As China enters 2026, its labor market is settling into a period of adjustment shaped by slower growth, structural demographic pressures, and a more cautious corporate mindset. For foreign‑invested enterprises (FIEs), this shift has important implications: hiring is becoming more selective, wage growth more differentiated, and workforce planning increasingly tied to location and risk considerations rather than expansion targets alone.

While headline narratives often oscillate between optimism and pessimism, the underlying reality of China’s labor market is more nuanced. Costs are not falling, but neither are they rising uniformly. Talent mobility has not disappeared, but it has become more deliberate. And the traditional dominance of Tier‑1 cities is gradually giving way to a more complex, multi‑city talent landscape.

Understanding these dynamics is essential for companies making hiring and investment decisions in China in 2026.

Wage trends: Moderation with pockets of pressure

One of the most common misconceptions about China’s labor market is that slower economic growth automatically translates into declining labor costs. In reality, 2026 is shaping up to be a year of wage moderation rather than wage contraction. Salary growth has clearly decelerated from the pre‑pandemic period, but it has not reversed, and the direction of change varies significantly by role, function, and city.

This moderation is most visible in Tier‑1 cities and in mature industries, where wage levels are already relatively high. For many white‑collar positions, particularly in administrative, support, and mid‑level management functions, base salary increases have flattened. Employers are increasingly cautious about committing to across‑the‑board adjustments, opting instead to link compensation more closely to individual performance, business profitability, and role criticality.

Recent survey data support this trend. According to 51job’s 2026 Resignation and Salary Adjustment Survey Brief, 42.8 percent of surveyed companies implemented salary increases in 2025, a slight decline from 44.8 percent in 2024. The average adjustment rate also edged down, from 4.3 percent in 2024 to 4.1 percent in 2025. Looking ahead, enterprises surveyed anticipate further budget tightening, with the average salary increase expected to dip marginally to around 4.0 percent in 2026 as companies take a more conservative view of revenue and margin growth.

At the same time, wage pressure has not disappeared – it has become more concentrated. Positions linked to technology transformation, advanced manufacturing, compliance, and operational risk management continue to command noticeable premiums. Demand remains particularly strong for AI‑related roles, experienced engineers, and professionals capable of navigating complex regulatory or cross‑functional environments. Even in a slower hiring market, these skill sets remain scarce.

This has resulted in a more polarized wage environment. While average salary growth appears modest at the macro level, companies competing for high‑value talent continue to face upward pressure, especially when hiring experienced professionals or localizing roles previously held by expatriates. The same 51job survey shows that in 2025, employees in technical R&D and professional skill roles received average salary increases of 5.3 percent, significantly higher than other functional groups.

A similar divergence can be observed between blue‑collar and white‑collar labor. Blue‑collar wages remain heavily influenced by local labor supply conditions, minimum wage adjustments, and overtime availability. In several regions, policy‑driven minimum wage increases continue to support income growth at the lower end of the labor market. Survey data indicate that frontline and service employees saw average salary increases of 4.1 percent in 2025, a trend closely linked to national policies promoting income growth among skilled and frontline workers. White‑collar compensation, by contrast, is increasingly shaped by role specificity and skill scarcity rather than by general market momentum.

Notably, salary adjustment rates across different cities declined slightly year‑on‑year in 2025, with new Tier‑1 cities recording average increases of around 4.1 percent, largely in line with established Tier‑1 cities. This convergence reflects both cost pressures in emerging hubs and greater discipline in compensation management nationwide.

For employers, the key challenge in 2026 is therefore not managing wage inflation across the board but identifying where wage pressure persists and where it has eased. As salary increase budgets tighten further, HR strategies are evolving accordingly. Companies are prioritizing differentiated incentives over uniform adjustments, concentrating resources on high‑value roles with proven impact. The 51job.com survey results suggest that “performance‑based differentiated salary increases” and “preferential adjustments for core employees” have become the two most widely adopted approaches, selected by 45.7 percent and 40.7 percent of companies respectively. In contrast, only a small minority of firms continue to rely on uniform, across‑the‑board adjustments.

Meanwhile, non‑monetary measures, such as flexible benefits, clearer career development pathways, and improved performance feedback, are playing a larger role in maintaining engagement when salary growth is limited.

| China’s Salary Adjustment Trends | |

| Year | Average salary adjustment rate |

| 2024 | 4.3% |

| 2025 | 4.1% |

| 2026 (est.) | 4.0% |

Source: 51Job.com

| Average Salary Increase by Industry | |||

| Industry | 2024 | 2025 | 2026 (est.) |

| High Technology | 5.2% | 4.9% | 4.9% |

| Pharmaceuticals & Healthcare | 4.8% | 4.4% | 4.3% |

| Manufacturing | 4.4% | 4.3% | 4.3% |

| Energy & Chemicals | 4.6% | 4.3% | 4.4% |

| Consumer Goods | 4.5% | 4.1% | 4.0% |

| Automotive | 4.3% | 4.1% | 4.1% |

| Trading / Wholesale & Retail | 4.3% | 4.0% | 4.0% |

| Transportation / Logistics | 4.2% | 4.0% | 4.0% |

| Catering / Hotels / Tourism | 4.0% | 3.7% | 3.7% |

| Financial Services | 3.8% | 3.5% | 3.2% |

| Culture / Education / Media | 3.2% | 3.0% | 3.0% |

| Real Estate | 3.1% | 2.9% | 2.8% |

Source: 51Job.com

Talent mobility: From opportunism to selectivity

China’s job‑hopping culture has undergone a visible shift since the peak mobility years of the late 2010s and the immediate post‑pandemic rebound. While labor mobility remains a defining feature of the market, it has become more selective and risk‑aware.

In 2024 and 2025, many employees prioritized job security over rapid advancement, particularly in large cities where hiring competition intensified, and layoffs in certain sectors reshaped expectations. This trend has not reversed heading into 2026. For a broad segment of the workforce, especially mid‑career professionals, stability, employer reputation, and long‑term development prospects now weigh more heavily than short‑term salary gains.

|

China Employee Job Hopping Rate |

|

| Year | Job-hopping rate |

| 2023 | 16.5% |

| 2024 | 15.3% |

| 2025 | 14.8% |

Source: 51Job.com

That said, mobility has not disappeared but simply become more segmented. Employees with skills aligned to growth areas, particularly AI, digital transformation, and advanced manufacturing, remain more willing to change jobs, often seeking roles that offer both higher compensation and stronger development trajectories. For these candidates, the market still rewards movement, albeit with greater scrutiny on employer credibility and role substance.

Sectoral patterns further highlight this divergence. Consumer‑facing service industries such as catering, hospitality, and tourism continue to record the highest turnover, with a 2025 attrition rate of 16.5 percent, only marginally lower than the previous year. Manufacturing followed closely at 15.7 percent, reflecting ongoing industrial upgrading, production line optimization, and workforce restructuring amid digitalization and “dual‑carbon” pressures. While demand for skilled technicians has strengthened, frontline production roles continue to face higher churn. The real estate sector, though seeing a modest decline from 2024, remains under pressure, with a 15.4 percent attrition rate as industry consolidation and personnel optimization persist. By contrast, transportation, logistics, and related sectors saw the most pronounced improvement in workforce stability in 2025, with attrition falling by 1.4 percentage points year‑on‑year. This trend reflects the maturation of logistics networks and the increasing use of flexible employment models, which together are contributing to more resilient employment ecosystems in these industries.

This divergence has important implications for employers. Attrition risk is no longer evenly distributed across the workforce. Instead, it is concentrated on specific functions and skill categories. Companies that fail to address development pathways and role clarity for high‑value talent may experience turnover even in an otherwise stable labor market, while those relying on generalized salary increases may find diminishing returns.

The evolving city‑tier equation

Perhaps the most significant structural shift in China’s labor market is the gradual rebalancing of talent across cities. While Beijing, Shanghai, Shenzhen, and Guangzhou remain central to China’s business ecosystem, their dominance as default hiring locations is increasingly being questioned.

Tier‑1 cities continue to offer deep talent pools, mature professional services, and strong infrastructure. However, they also come with higher labor costs, more intense competition for skilled professionals, and stricter compliance and enforcement environments. For many companies, especially those with established China operations, the question is no longer whether to operate in Tier‑1 cities, but which functions genuinely need to be located there.

At the same time, a group of “new Tier‑1” and strong Tier‑2 cities, including Chengdu, Hangzhou, Chongqing, Suzhou, Nanjing, Wuhan, Ningbo, and others, are attracting increasing attention from both employers and job seekers. These cities benefit from growing university talent pipelines, supportive local policies, and lower overall employment costs, while offering living standards that appeal to younger professionals.

For certain functions, particularly back‑office operations, shared services, engineering support, and even some technology roles, these cities now offer genuine labor‑cost arbitrage without the severe talent constraints once associated with non‑Tier‑1 locations. However, this arbitrage is not automatic. Savings depend on realistic expectations around productivity, management oversight, and retention. Companies that relocate functions without adapting management structures or compliance processes often find that initial cost advantages erode over time.

In 2026, effective workforce location planning increasingly involves a multi‑city approach rather than a single‑hub model.

Demographics and the growing skills mismatch

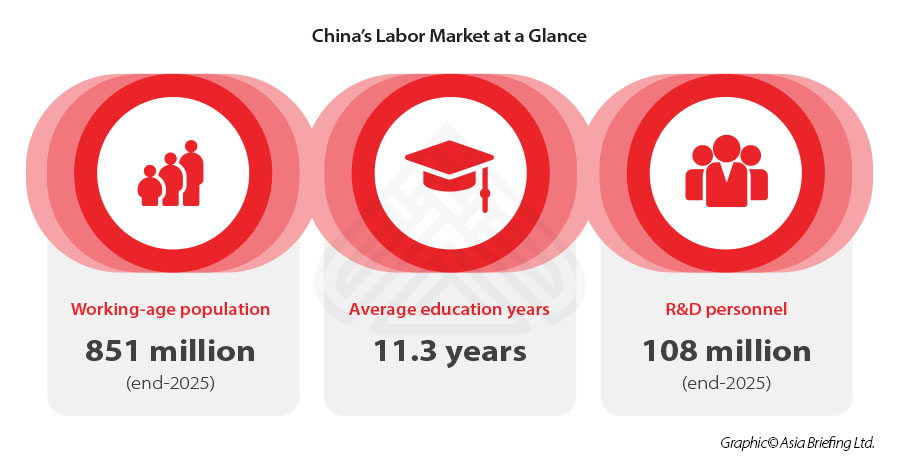

Underlying these market dynamics is a longer‑term structural challenge: China’s demographic transition. Although the country still maintains one of the world’s largest labor forces, with the 16–59 working‑age population standing at around 851 million at the end of 2025, this cohort is gradually shrinking, while the average age of workers continues to rise. At the same time, the economy’s demand for advanced technical, digital, and management capabilities is accelerating, creating a widening gap between labor supply in aggregate and skill availability in practice.

This creates a growing mismatch between labor supply and labor demand. On one hand, there is no shortage of workers in aggregate terms. On the other hand, employers frequently report difficulty hiring professionals with the specific skills required to operate automated systems, manage complex compliance environments, or support digital transformation initiatives.

As China invests heavily in automation, robotics, and AI, the demand for skilled operators, engineers, and managers capable of integrating technology into business processes continues to rise. Yet, training and reskilling systems are still catching up with this pace of change. For employers, this means that labor availability alone is no longer a reliable indicator of hiring ease.

In this context, competition for skills is likely to intensify even if overall employment growth remains modest.

What this means for employers in 2026

Taken together, these trends point to a labor market that rewards precision rather than scale. Hiring strategies in 2026 must be localized, role‑specific, and aligned with realistic assessments of both cost and risk. Compensation strategies should reflect market moderation while remaining flexible enough to address genuine skill shortages. Workforce planning must anticipate uneven attrition patterns rather than relying on historical averages.

Most importantly, sustainable hiring is increasingly about structure rather than speed. Companies that invest in clear role design, compliant employment frameworks, and thoughtful location planning are better positioned to navigate China’s evolving labor environment than those focused solely on short‑term cost savings or rapid expansion.

In a market shaped by adjustment rather than acceleration, a disciplined workforce strategy has become a competitive advantage.

(This article was originally published in China Briefing Magazine: Labor Trends and Risk Management in China 2026, complimentary download is available.)

Regional HR Expertise

Dezan Shira & Associates’ specialized HR teams support companies in managing compliant, efficient HR and payroll operations across Asia. To learn how localized HR expertise can help you navigate China’s evolving labor landscape with confidence, please contact China@dezshira.com.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article China’s 15th Five-Year Plan: Key Insights for Foreign Investors

- Next Article