China’s Economic Roundup: October 2022

China’s economic indicators for the month of October reveal a slowdown in retail sales, fixed asset investment, and property investment as the country faces a number of challenges, including extended COVID-19 outbreaks, concerns over a worldwide recession, and a real estate slump. Strategic sectors like high-tech and green energy performed strongly, while the country’s expectations for attracting foreign investment continue to rise. Following recent steps to relax some COVID-19 curbs and provide financial support to the distressed property sector, Chinese officials are taking resolute actions to navigate the economy through rocky waters.

After a stronger-than-expected recovery in Q3 of 2022, China’s economy is struggling to accelerate its growth. Several key economic indicators, such as industrial output, retail sales, and fixed asset investment, released by the National Bureau of Statistics on November 15, show a slowdown in growth. The domestic economy is under strain from several factors, including continuing COVID-19 limitations, a weakening property market, a sluggish global economy, and rising inflation rates in foreign markets.

October was an eventful month in China. The 20th National Congress of the Chinese Communist Party was held in Beijing, marking a decisive moment for the future of Chinese politics and policy outlook. During the same month, tourism suffered during a weeklong public holiday as a result of ongoing travel restrictions to manage COVID-19 outbreaks. According to official statistics, tourism earnings for the holiday were only 44 percent compared to the 2019 pre-pandemic levels. Infections have increased in the interim, forcing businesses to temporarily close down.

While certain industries have defied economic challenges to see strong growth in October and the preceding months, such as the green energy and technology sectors, the overall economic scenario is not meeting expectations. The producer price index declined in October for the first time in nearly two years, while exports fell for the first time since May 2020. Moreover, with a modest 0.6 percent yearly gain, the core consumer price index – which excludes food and energy – showed no change from September. As we head into the end of the year, the government has indicated it will roll out further stimulus measures to keep the economy on the uneven road to recovery. At the same time, it will remain committed to the zero-COVID policy and refrain from adopting sweeping stimulus measures.

Below we look at the key economic and trade data for October and discuss how the government plans to steer the country out of the current economic rut.

Economy indicators show tentative growth

Industrial sector output slows, but high-tech sectors continue to thrive

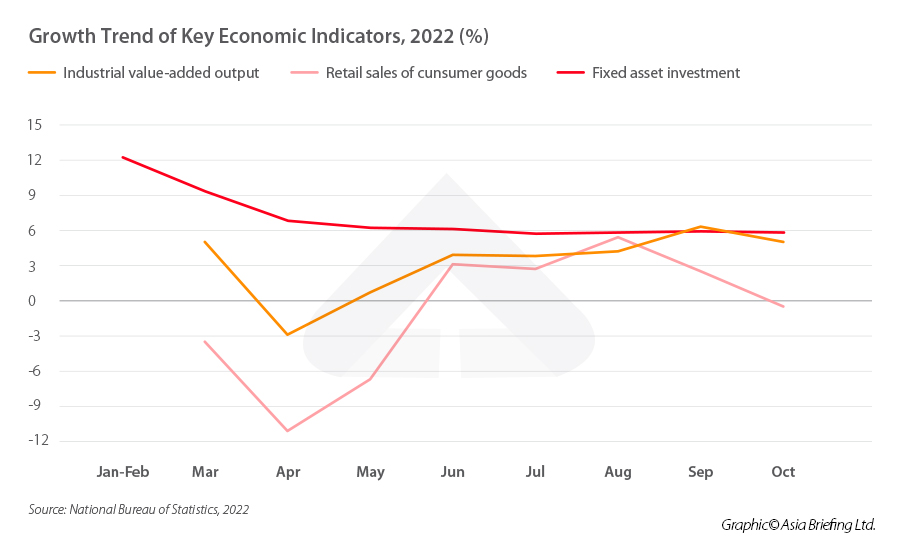

Value-added output of industrial enterprises over a designated size (those with an annual main business income of RMB 20 million, or US$2.9 million, and above) grew by 5 percent year-on-year, slightly missing expectations for a 5.2 percent gain, indicating a slowdown from the 6.3 percent growth seen in September.

Two of the three main industries experienced a growth slowdown, while one accelerated:

- Mining grew by 4.0 percent year-on-year, slowing from 7.2 percent in September

- Manufacturing grew by 5.2 percent year-on-year compared to 6.4 in September

- Electricity, heat, gas, and water production and supply grew by 4.0 percent year-on-year, an acceleration from just 2.9 percent in September

Certain sectors still saw significant month-on-month growth despite the overall slowdown, in particular, green energy and smart products, such as new energy vehicles and solar energy batteries:

- New energy vehicles were up 84.8 percent year-on-year

- Lithium batteries grew by 142.6 percent year-on-year, up from 10.8 percent in September

Meanwhile, growth of the value-added output of the high-end manufacturing industry also outpaced the overall industrial sector, reaching 10.6 percent, growing 1.3 percentage points faster than in September.

The manufacturing purchasing manager’s index (PMI), which gives an indication of manufacturing activity in China, showed a contraction in October at 49.2 percent, down 0.9 percentage points from September.

Retail sales fall amid weak demand, the service sector accelerates its digital transformation

The Index of Service Production (ISP) for October, which indicates the output change of the service industry, increased by 0.1 percent year on year, down from 1.3 percent in September.

Production indicators of the main services sectors still saw positive growth:

- Information transmission, software, and IT services grew 9.2 percent year-on-year, 0.7 percentage points faster than in September

- The financial industry grew 6.4 percent year-on-year, 1.5 percentage points faster than in September

Meanwhile, between January and October 2022, the operating income of service enterprises above a designated size grew 4.7 percent from the same period last year. Among these:

- Information transmission, software, and IT services grew 8.0 percent year-on-year

- Health and social work services grew 8.9 percent year-on-year

- Scientific research and technical services grew 7.9 percent year-on-year

China’s Service Business Activity Index for July, which indicates development in the service sector business activities, was 47 percent. The index for industries including railway and air transportation, catering and hospitality, telecommunications, radio and television, satellite transmission services, ecological protection and public facility management, culture, sports, and entertainment stood at 55 percent, indicating that they are still within the region of expansion.

The slowdown in the ISP was due in part to drag from the real estate market, which saw an 8.8 percent contraction in its production index. In addition, some in-person services also saw slowed growth due to the impact of COVID-19 outbreaks and restrictions.

Meanwhile, retail sales in July continued to see sluggish growth, reaching 2.7 percent, a slowdown of 0.4 percentage points from June. Among the various types of consumption:

- Retail sales of goods reached RMB 3.6 trillion (US$502 billion), a year-on-year increase of 0.5 percent

- Catering revenue reached RMB 409.9 billion (US$57 billion), a year-on-year decrease of 8.1 percent

- Retail sales of grain, oil, and food companies above the designated size (annual main business income of RMB 20 million and above for wholesale companies, RMB 5 million and above for retail, and RMB 2 million and above for catering and hospitality) increased by 8.3 percent a year-on-year

- Retail sales of gold, silver, and jewelry companies above the designated size fell by 2.7 percent year-on-year

- Retail sales of household appliances and audio-visual equipment companies above the designated size fell by 14.1 percent

In the period between January and October 2022, total retail sales of consumer goods decreased by 0.5 percent from the same period in 2021. Of this, online sales of material goods accounted for 26.2 percent of total retail sales, growing 7.2 percent from the same period in 2021 to reach RMB 9.4 trillion (US$1.3 trillion).

Fixed asset investment growth slows, housing crisis deepens

Growth of fixed asset investments (FAI) in October increased just 0.12 percent month-on-month and slowed from 6.1 percent in the first half of 2022 to 5.8 percent in the period from January to September 2022. Meanwhile, infrastructure investment grew 8.7 percent year-on-year on the back of increased government spending through the issuance of special purpose bonds (SPBs), and manufacturing investment grew 9.7 percent year-on-year. Real estate development decreased by 8.8 percent from January to October, further lowering from the 8.0 percent drop registered in the first nine months of 2022.

Real estate development investment and sales still represent the largest contraction, with commercial housing sales dropping 26.1 percent year-on-year (a slight recovery compared to a decrease of 26.3 percent from January to September 2022). Since several developers started making loan defaults in the second half of 2021, China’s housing industry has been in a serious crisis, and a mortgage boycott continues to scare away prospective homebuyers.

Investment across most other sectors showed some loss, with FAI slowing slightly from September, and showing a slow recovery from the same period in the previous year in the three main industry sectors:

- FAI in primary industries grew 1.4 percent year-on-year, slowing slightly from 1.6 percent in September

- FAI in secondary industries grew 10.8 percent year-on-year, slowing from 11.1 percent in September

- FAI in tertiary industries grew 8.7 percent year-on-year, increasing from the 8.7 percent growth in September

Meanwhile, FAI in high-tech sectors in October remained strong:

- High-tech manufacturing increased 23.6 percent year-on-year

- High-tech services increased 14.3 percent year-on-year

Among the high-tech manufacturing sectors, investment in electronics and communications equipment manufacturing grew 20.8 percent year-on-year compared to 19.9 percent in September.

China exports slow down, FDI on the rise

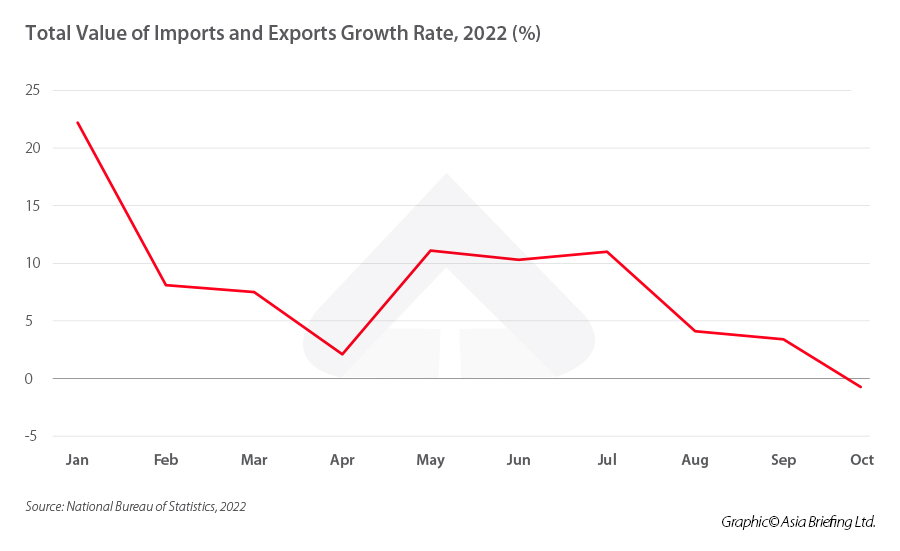

China’s trade data disappointed forecasts in October. Total import and export of goods in October reached RMB 3.4 trillion (US$482 billion), a year-on-year increase of 9.5 percent, which is however slower than the growth rate registered in September. Exports decreased 0.3 percent from the previous year, registering the first drop since May 2020, amid weak overseas demand.

As local demand declined in the face of tight COVID-19 curbs, imports shrank at a quicker 0.7 percent rate compared to the previous month, marking the first decline since August 2020.

Imports and exports between private companies accounted for 50.4 percent of the total in the period between January and October, increasing 2.2 percent year-on-year.

Compared with September, the year-on-year growth rate of imports and exports in October slowed down. As the global economic scenario continues to look gloomy, many markets are preparing for an approaching recession. The resistance from the global side of demand to exports could be the main reason why China’s export growth may fall again in the next four quarters. Leading indicators such as the decline of global PMI and the year-on-year decline of the inventory of major durable goods in the US all indicate that the overseas demand market is highly likely to continue to shrink.

Specifically, China’s exports to the EU, the US, Japan, and the United Kingdom continued to show slower growth trends. The reason is still that the production capacity of these developed countries is weak, while their import demand continues to decline.

China’s largest trade partner in 2022 remains the Southeast Asian region, which accounted for the majority of all imports and exports in the period between January and October. China’s trade surplus with the region expanded during this period, reaching RMB 5.26 trillion (US$736 billion), and accounting for 15.2 percent of China’s total foreign trade. China’s highest imports came from ASEAN, amounting to RMB 2.2 trillion (US$334 billion), showing a year-on-year growth rate of 15.8 percent.

The EU was China’s second-largest trading partner with a total of RMB 4.6 trillion (US$641.7 billion). Exports from China to the EU grew 15.9 percent year-on-year, while imports fell by 4.7 percent, likely due to the impact of the Russia-Ukraine conflict and slowing market demand.

The US is China’s largest export country and third-largest trade partner. Exports from China to the US grew by 8.5 percent year-on-year to reach RMB 325 billion (US$45.3 billion), while imports grew just 1.7 percent year-on-year.

South Korea is China’s fourth largest trade partner. Exports to South Korea grew by 16.3 percent, while imports declined by 0.3 percent.

From the perspective of commodities, in October, the growth rate of steel and copper imports continued to decline by 19.72 percent and 18.08 percent, respectively, from 18.66 percent and 5.71 percent registered in September. On the other hand, the import growth of crude oil was 43.81 percent. Imports of iron, soybeans, and integrated circuits contracted by – 26.79 percent, – 6.05 percent, and -1.05 percent year-on-year.

FDI to grow double digits

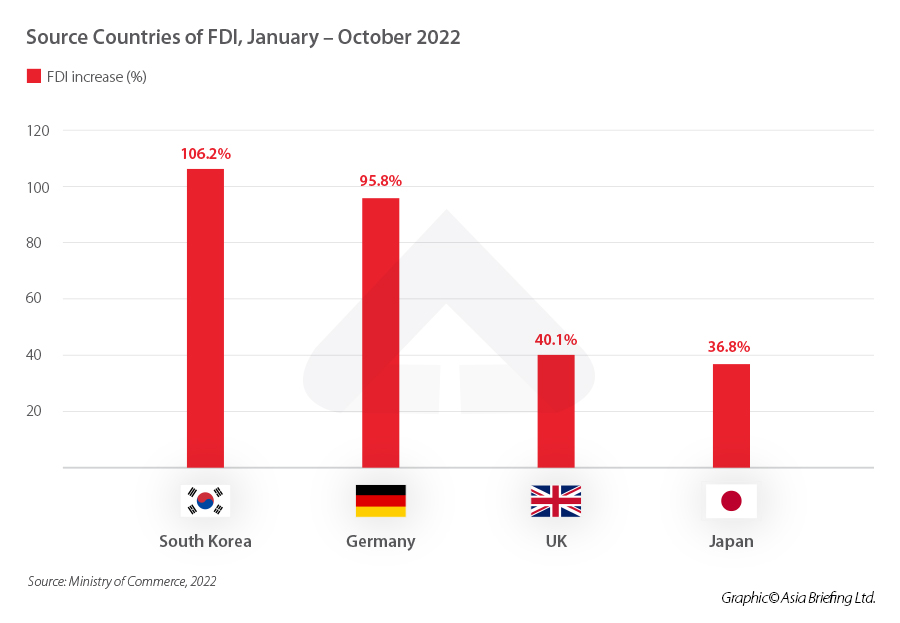

Following the performance between January and October, which created a strong platform for growth, the inflow of foreign direct investment (FDI) is projected to increase by double digits this year, according to market observers and company leaders.

Thanks to new opening-up policy measures, high-standard business platforms, and multilateral trade initiatives like the annual China International Import Expo and the Regional Comprehensive Economic Partnership (RCEP) agreement, China has managed to create a favorable environment for the growth of foreign-funded companies.

In particular, high-tech industries experienced a significant year-on-year rise in FDI of 31.7 percent between January and October as China entered its new era of environmentally friendly and innovation-led growth. Specifically:

- FDI increased by 57.2 percent in high-tech manufacturing, year-on-year

- FDI increased by 25 percent in high-tech services, year-on-year

What is the government doing to spur economic growth in Q4?

For the remainder of 2022 and the first half of 2023, the Chinese economy’s recovery could be slower than anticipated. A slow real estate market and low consumer confidence are reducing domestic demand. Without a set end date, the zero-Covid policy will remain in place, and the government is not expected to introduce significant stimulus measures to boost the real estate market. In addition, a global economic slowdown, particularly in the US and Europe, will affect China’s export orders.

In a meeting on the economy held in late July 2022, China’s Politburo subtly retracted its 2022 GDP growth target of “about 5.5 percent,” indicating it does not anticipate reaching this level by the end of the year. The governing body argued in favor of “focusing on stabilizing employment and prices, keeping the economy working within a tolerable range.” Moreover, China has historically followed a “prudent” monetary policy that prefers the use of targeted financial instruments over more forceful stimulus, such as lending and policy loans to boost certain businesses and groups and broader loan rate decreases to inject cash into the banking system. The goal of this policy is to prevent flooding the market with liquidity and overstimulating the economy. The government, however, might still turn to a policy of fiscal expansion to spur the economy at last.

To maintain economic stability, Beijing has signaled several positive steps in the direction of opening up and reviving the general business sentiment. In recent declarations, Chinese authorities reaffirmed that growth was still a top goal and that they will continue with reforms. This helped to support stock markets that had already been boosted by expectations that Beijing might relax its stringent COVID-19 regulations. Investors clung to the hope that China may relax its strict COVID policy in the coming months, despite the fact that the number of cases has been increasing, and lockdowns continue without a clear end in sight.

As China’s industrial chain continues to meet global companies’ demands, from equipment manufacturing to high-end product research and design, the country is eager to attract foreign investment. The nation’s main economic regulator, the National Development and Reform Commission (NDRC), released 15 measures in October to facilitate foreign-invested projects. The measures include enabling foreign businesses to raise capital on domestic stock exchanges and assisting them in their industrial endeavors.

Infrastructure investment has historically been a key driver of China’s economic growth, and it appears the government will continue to rely on infrastructure investment to support the economy in the upcoming months. In a recent effort to contain the housing market problem, Chinese financial authorities asked the nation’s banks to facilitate more financing to the real estate industry, releasing 16 financial measures to promote market development.

In a meeting with Managing Director Kristalina Georgieva of the International Monetary Fund (IMF), Premier Li Keqiang also reassured that, in order to maintain the major economic indicators within a reasonable range, consolidate and expand the steadily upward trend of the economy, and make a full-scale effort to improve results throughout the year, China will continue to fully implement a package of policy measures for stabilizing the economy.

The investments in infrastructure targeted monetary tools, and further opening up of the economy may continue to support China in avoiding the worst effects of the global recession, while the country pursue slow yet steady economic growth.

About Us

China Briefing is written and produced by Dezan Shira & Associates. The practice assists foreign investors into China and has done so since 1992 through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Dongguan, Zhongshan, Shenzhen, and Hong Kong. Please contact the firm for assistance in China at china@dezshira.com.

Dezan Shira & Associates has offices in Vietnam, Indonesia, Singapore, United States, Germany, Italy, India, and Russia, in addition to our trade research facilities along the Belt & Road Initiative. We also have partner firms assisting foreign investors in The Philippines, Malaysia, Thailand, Bangladesh.

- Previous Article How to Sell to Chinese Consumers Through Cross-Border E-Commerce Platforms

- Next Article China-Cuba: Bilateral Trade and Investment Prospects