Economist China Summit: The Debates Discussed

Op-Ed Commentary: Chris Devonshire-Ellis

Nov. 3 – The Economist Magazine’s China Summit was held today in Beijing, a major platform for senior business executives involved in China to get together, debate and participate in the pressing issues of China’s future. Provocatively subtitled “China and the New World Disorder,” the event was attended by some 150 senior level executives of most of the well-known MNCs operating in China today. Via a series of different sessions, a number of China strategic and development issues were raised and discussed.

The economists debate

The first session, in which Shen Mingguo, China chief economist for Citigroup, Arthur Koebler of Gavekal Dragonomics, Xiao Geng, a Colombia University professor, and Xu Sitao, chief economist for the Economist, debated China’s development in light of the Global Financial Crisis, and made a variety of comments that gave rise to an expected slowdown in the Chinese economy. Stating that a change “from fast growth to sustained growth” was occurring, predictions were made that Chinese exports were set to slow by nearly 50 percent in the next decade, and that the inflation rate was expected to remain around the 5 percent mark for the period. An appreciation of between 4 percent and 5 percent of the RMB against the U.S. dollar over the next 12 months was generally agreed likely.

It was also noted that China needed to develop its own technologies as a result, as technology acquisition would fall as a result of a reduction in export growth. Noting that the government had tried to slow property speculation, it was mentioned that the problem with reining this sector in was that no incentive had been given by the government to realign domestic savings into expenditure elsewhere. Reacting to comments over China property concerns, opinions on the “acres” of vacant buildings in many Chinese cities varied. Some argued that the vacancies would be able to be taken up by migrant workers relocating to cities, while other stated that there was an underlying problem of China becoming massively overbuilt and there was nowhere else to put money, which has fueled concerns over a potential deflationary period as such assets would turn negative in value later. It was noted that a major dynamic would be the migration of labor from the rural to urban areas of China and that some 13 million farmers per annum would relocate into cities, and that this dynamic would change China’s economy.

The issue over whether a link really existed between the one party state system and economic reform was judged “not yet proven” due to questions over whether such a system could provide more accountability. While the one party state system, it was noted, had pushed through significant reforms, much had been concentrated in infrastructure development and the real test, of consistently raising people’s income levels, was still to be answered, as was a rebalancing of the economy. When asked which market sectors in China were to look out for as hot, automated machinery was mentioned as very much a growth area in China, with imports of such being second only to food in the past 12 months. As Chinese labor becomes more expensive, automation will result, and there are opportunities for both suppliers and China’s own development in this sector. Market sectors deemed as poor prospects were any industry related to labor intensive production, which it was agreed have had their day and would be better off relocating to other Asian economies.

It was agreed that the export sector would increase in one key area: that of infrastructure services and development, and that China was already beginning to export its infrastructure development capabilities globally. China would develop more towards a provider of infrastructure related technologies and know-how, and less of a supplier to Wal-Mart type products globally. (That said, Wal-Mart is currently the largest MNC in China).

Concerning the development of Central and West China, it was stated that the development would remain on the eastern seaboard and that China’s hinterland would remain relatively weak compared to the east (not a position shared elsewhere, as I shall come to). Urbanization would provide a flow of migrant labor to the east, and this would sustain eastern development.

The debate, while of use, failed to address core issues and made rather too many assumptions on growth figures while at the same time acknowledging inherent government distortion. I personally came out of the session none the wiser, and a more detailed explanation of why certain growth figures were made would have been more useful. In the absence of such, I felt the economists themselves relied too much on assumptions and less on fundamentals, which appeared rather woolly. The general outlook I would suggest was “cautious,” and it was interesting to note economists’ views on migration of the development of Central and Coastal China varied considerably from the manufacturing sector (which I review later).

China’s global PR image

A session with Harris Diamond, CEO of Weber Shandwick, discussed the position of China Inc as a brand, with the overall consensus reached that the nation has not yet reached maturity yet to be able to properly quantify what “China” means, especially in trade. Specifying that “China has no current brand,” it was suggested that the brand development China will be defined within the next 10 years, and the verdict was out on how that would come to pass. Recognizing that China was known for strength and growth, it was implied that questions remained over China’s ability to project itself as a responsible global player and that this was a hindrance to its global perception. Recent diplomatic incidents concerning various border disputes had not helped China develop a reputation for providing regional security or stability, and concerns over the political process in choosing the next generation of leaders, coupled with a rise in costs meant that senior executives globally had some questions over the future role and development of China for the next decade. This made China’s global image difficult to pin down, and although the country had made giant steps over the past decade, what was still needed was a definite reliability on the nation, which to date was not entirely forthcoming. “Brand China” accordingly was still a work in process, the national image was in a state of flux, and there were conflicting aspects to the political system. Yes, it had delivered economic growth, but was it still the right system to manage development from here on in? The lack of an answer to that question creates uncertainty in the minds of many when considering China’s capability to consistently deliver growth as expected in the future. Consequently, China’s brand was still to be determined.

What was likely to occur from the commercial perspective is that Chinese state-funded enterprises would grow stronger, and MNCs investing in China would find it took longer than was previously the case to establish and develop their businesses as a result. MNCs would not find growth as easy to accomplish as in the past, and the rise of China’s SOE’s and companies would provide new challenges. China had developed as an OEM manufacturer, but by definition this meant no brands had developed. As China’s OEM manufacturers developed their own brands, a shift would occur, but they remained less transparent than Indian MNCs as an example, which were often top in class and free of political interference. As a result, Chinese companies may not always succeed globally due to continuing perceptions of government involvement in their operations, and “brand China” had yet to emerge.

China in a multipolar world

This session, which included Jon Huntsman, the U.S. ambassador to China, Simon Tay, the chairman of the Singapore Institute for International Affairs, and Pang Zhongying, professor of international affairs at Renmin University, examined China’s role in an increasingly multi-polar world. Noting that 10 years on from China’s accession to the WTO it had now grown to become the world’s largest economy, it was suggested that China had still not politically adapted to this position. While the United States was often criticized, it was understood that in such a position people will challenge your authority, just as China had challenged that of the U.S. economy and of the U.S. dollar as a reserve currency. Yet when China was criticized, the reaction was often more inflammatory, and that the country needed to move on and develop, and get used to being in the spotlight in international affairs.

It was also suggested that while China had achieved a global position and was respected, it was still yet to be fully trusted. To be trusted meant that China needed to integrate better into global world views, participate more, and that issues such as the free flow of information, economics, democratic institutions and rule of law were still out of norm with its global counterparts. The issue over trust with China remains unresolved at the present time, it was suggested. Ambassador Huntsman commented that the U.S.-China relations were progressing, but still had to find “cruising altitude.” Another commentator likened China as “being on the world stage, but with its back to the audience.” The ambassador countered by suggesting that China needed to provide security, stability and predictability, and that much remained to be done concerning the latter aspect, although it was noted that of U.S.-China commercial disputes, only about 3 percent of such transactions went to litigation, suggesting the WTO mechanism was working well. The ambassador also stressed that the United States had been engaged within the Asia region for over a hundred years now and that this position would be both strengthened and maintained. Comments that China was deliberately being contained, he said, were purely conspiracy theories of no merit, and that the American position was purely to maintain and keep open global trade routes with and throughout Asia. The panel viewed predictability as being the predictability of results, including rule of law, a democratic process in decision making, and independent arbitration over disputes.

The rise of India was mentioned, and the view was that this presented a new opportunity for capital flows to find safe havens in India, as opposed to China. It was expected that China would lose some momentum to India, which in contrast did possess the values mentioned under the predictability of results platform, and that this was now about to work to India’s global trade advantage.

China governance debate

This section was contributed to by Donald Clarke, of George Washington University Law School, Sanjay Peters, professor of economics for the Center for Emerging Markets at the IESE Business School, James Miles, China correspondent for The Economist, and Mao Yushi, president of Unirule Institute of Economics. Much of the session revolved around the new leadership due to be put in place in China by 2012, and whether this would indicate China was entering into a risky period, and whether the political system could provide stability. Comment was made also on the rise of trade unionism in China, and the position over collective bargaining, in which employees have the right to decide who the Union leader should be via a democratic vote. It was pointed out that the last leadership change from Jiang Zemin and Zhu Rongji to Hu Jintao and Wen Jiabao had also raised concerns in the Western media, but had in fact proceeded smoothly, and that this was expected to be no different. The issue over collective bargaining was likened to the rise of democratic institutions and labor unions in the West, and that the development of these issues was a sign of China progressing, rather than becoming more militant. However, it was accepted that especially in South China where much of the labor unrest had occurred, the government wanted to take more control of the movement in unionization to prevent it becoming too militant.

Concerning the development of China’s judiciary, a rather bleak picture was presented, whereby China had previously answered the “Red or Expert” question over judges by recruiting more legal experts into the system. However, that position now seemed to have moved backwards, with mediation often being the preferred route, often by judges unfamiliar with the rule of law. A culture of legal predictability versus incentives was prevalent, with judges being swayed by incentives rather than rule of law or precedent in handling cases. This remained a problem, with China’s judiciary remarked upon as having devolved into handling “plea bargaining plus incentives.”

Will China develop beyond middle income?

This session involved Michael Koenig of Bayer, Christophe Bezu of Adidas, Mary Boyd from The Economist, Ling Hai of Mastercard, Peng Xizhe, a Fudan University professor, and Roberto Leonardi of Munich Health. In it various summaries were provided on population trends and demographics, while Bayer and Adidas were in agreement over one particular aspect of China’s growth – that the coastal regions were slowing in growth and that the new markets were inland. While it was noted that there would be a shift in rural populations to cities, this was now expected to take place only within the provinces themselves, and not so much as inter-province as before. (A fact borne out by the relative closeness of income levels in China’s second and third-tier cities). As migrant workers no longer needed to travel so far to find a better level of income, so their own travel would decrease and remain within their own province. Any changes to the hukou system would be expected to accelerate this process.

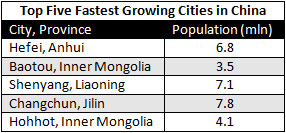

Both Bayer and Adidas stated they believed that although the coastal cities would gradually become more sophisticated, and align with some of the demands of consumers in markets such as the United States and the European Union, the real growth driver was in rural China, and the inland urban populations they contained. The top five fastest growing cities in China, determined by per capita GDP and disposable income, were thought to be:

In terms of the nine most popular items purchased in what were loosely termed as “rural areas,” these were identified as being:

- Mobile phone

- Personal computer

- Television

- Digital camera

- Hi-Fi

- Microwave oven

- Car

- Video camera

- Refrigerator

Meaning that unlike 10 years ago, most families now possessed a washing machine and were computer literate. Such demographic trends show that growth in the more rural, second and third-tier cities would outstrip that of the eastern seaboard, and that MNCs selling into the China market now needed to tap into the emerging consumers in rural areas. It was also suggested that product offerings should adapt to an aging population, and that products associated with lifestyle, sports, and related to an aging population should be adapted for the China market in these areas.

Summary

At such events it is always difficult to try and pull real hard facts from the debates as there remains such a divergence of opinion about China. However, where the major disagreement came about was between the economist’s view of the changes of China, and especially the migrant labor changes from rural to urban consumers, and the views of industry. It appeared to me at least that the industrialists were better prepared and had more thorough practical research to back up their claims than the economic experts did. However, the general feeling I took from the event was one of some caution needing to be deployed towards China, and while all delegates remained optimistic for the longer term, it seemed apparent a certain sense of unease was developing over aspects of the Chinese economy, and the greater expenses that China seems to be placing upon corporate businesses. The debate over the extent of a property price bubble and the admitted overbuild of China was felt not to be of a concern by the economists, yet again their views that such properties would be taken up by migrant labor do not seem to be borne out by the demographic trends evolved from industry. A disconnect between what the economists see of China, and what the manufacturers see appears to be developing.

Concerns also about the predictability of China seem to be on the rise, both in terms of its governance, political system, and the handover of power to the next generation of leaders. Yet, as was wisely pointed out, we’ve seen this before in terms of “concern” only to see China sail through such issues without any problems. Again, the overall perspective remains mixed. My own view is more of the same, yet China’s own demographics are changing and it is becoming a more, rather than less complex market to both predict and to assess. Opportunities obviously exist within China’s inland regions, yet the rise of domestic competition – often with state funding – will pose more problems for investing companies than previously was the case. However, it was also acknowledged that India remains an option for capital flows, and that the rise of other emerging Asian destinations also developing to compete with China will dictate at least one positive – MNCs have far more choice now than ever before as to where to spend their investment dollars – both within China and beyond it.

I recommend that businesspeople in China serious about investment and development in the country subscribe to the Economist Intelligence Unit for China and their related programs. They remain the benchmark forum for impartial and far-reaching discussions. Please access their China pages for details of their complete China archives.

Chris Devonshire-Ellis is the principal and founding partner of Dezan Shira & Associates, establishing the firm’s China practice in 1992. The firm now has ten offices in China, five in India, and two in Vietnam. For advice over China strategy, trade, investment, legal and tax matters please contact the firm at info@dezshira.com. The firm’s brochure may be downloaded here.

Chris also contributes to the Asia Briefing publications India Briefing, Vietnam Briefing, and 2point6billion.com.

- Previous Article Approval for China Outsourcing Services Decentralized to Provincial Gov’t

- Next Article Customs Adds Extra Administrative Processes for Enterprises Importing Trade Goods