Expat Taxes in Hong Kong – A Brief Overview

Expat taxes in Hong Kong are relatively simple to handle, but can be confusing for new arrivals and those with multiple income streams. Unlike in other jurisdictions, individuals must handle the filing and payment of tax on employment income by themselves. This guide provides a brief but comprehensive overview of tax liabilities for foreigners working in Hong Kong.

Hong Kong offers a relatively simple personal tax regime with low tax rates on salaries. However, unlike in many other jurisdictions, employers in Hong Kong are not responsible for withholding and paying tax on salaries, meaning individuals must file and settle their own tax obligations directly with the Inland Revenue Department (IRD). For expats new to the territory, understanding how the system works, including its provisional tax mechanism and biannual payment schedule, is essential to staying compliant and avoiding penalties.

Taxes for expats in Hong Kong

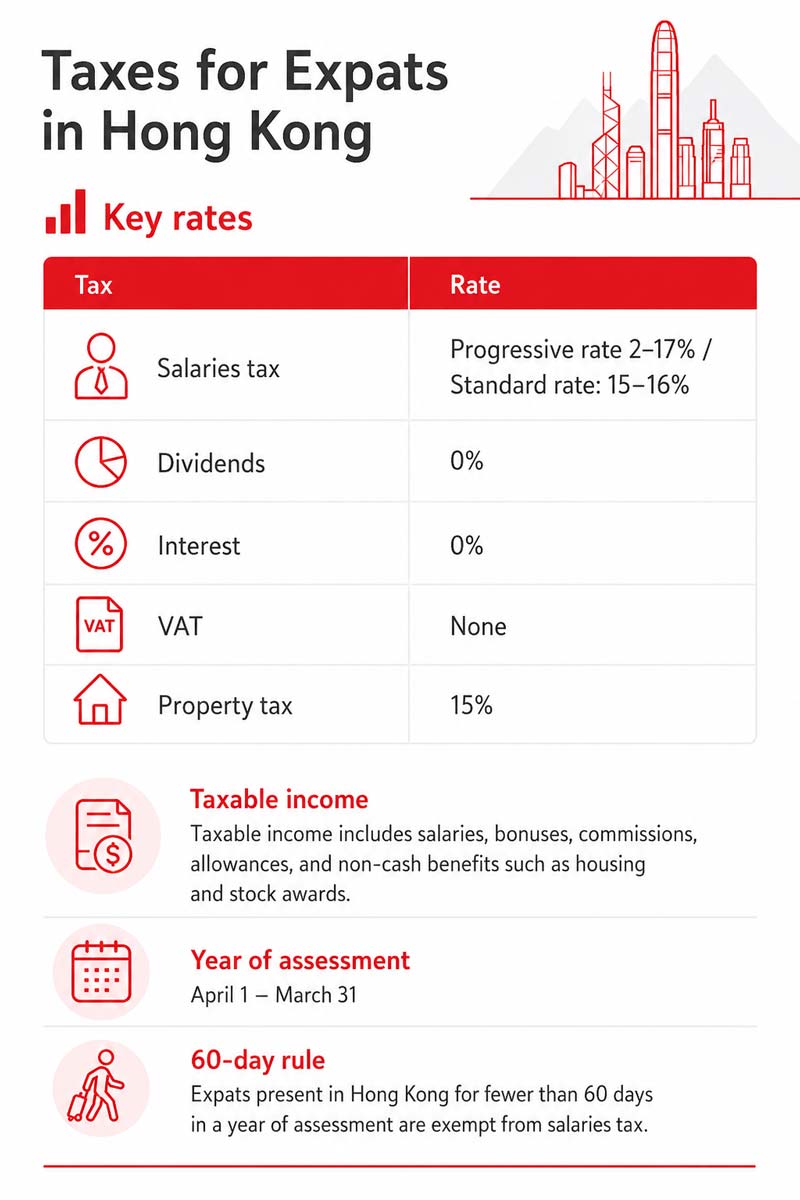

The main tax payable by expats in Hong Kong is the salaries tax, which is levied on all taxable income derived from employment in Hong Kong. Income derived from outside of Hong Kong is not subject to salaries tax.

Hong Kong does not levy any withholding taxes on interest or dividends.

Salaries tax is payable for each year of assessment (YA), which runs from April 1 to March 31 of the following year.

Taxable income includes salaries, wages, commissions, tips, bonuses, allowances, perquisites, leave pay, terminal and retirement awards, contract gratuities, and non-cash benefits such as the provision of a place of residence and the granting of stock-based awards.

Expats must also pay property tax on property they own in Hong Kong at the same rate as local residents.

Taxpayers do not need to pay salaries tax on income if they have cumulatively spent less than 60 days in Hong Kong during a given YA.

Taxes payable by directors

Holding the position of a director in an office in Hong Kong is considered holding an office, and earnings from an office are subject to salaries tax if the company’s central management and control are exercised in Hong Kong. This means that fees paid to a director of a company in Hong Kong can be subject to salaries tax even if the individual is not based in Hong Kong.

If the director is simultaneously an employee at the company, both the salary and the director’s fees are subject to salaries tax.

Salaries tax rates

Hong Kong charges salaries tax through two different mechanisms:

- A progressive tax, charged on assessable income after deduction and allowances.

- A two-tier standard tax, charged on assessable income after deductions but before allowances.

Tax is calculated using both methods, and you pay tax at the rate that yields the lower amount.

Currently, the progressive tax rates range from 2 percent to 17 percent.

| Hong Kong Progressive Tax Rates | ||

| Net chargeable income (HK$) | Rate | Tax (HK$) |

| On the first 50,000 | 2% | 1,000 |

| From 50,000 to 100,000 | 6% | 3,000 |

| From 100,000 to 150,000 | 10% | 5,000 |

| From 150,000 to 200,000 | 14% | 7,000 |

| Over 200,000 | 17% | |

As of YA 2024/25, the standard tax rate is 15 percent on the first HK$5 million of net income and 16 percent on the remainder.

|

Hong Kong Standard Tax Rates |

||

| YA | 2020/21 to 2023/24 | 2024/25 onwards |

| Standard Rate | 15% | |

| On the first HK$5,000,000 of net income | 15% | |

| Above HK$5 million of net income | 16% | |

Tax deductions and allowances

Hong Kong allows taxpayers to apply a broad range of tax deductions to reduce their net chargeable income. Allowances and deductions are claimed on the annual tax return.

Deductions can include, but are not limited to:

- Outgoings and expenses, where they are wholly, exclusively, and necessarily incurred in the production of the assessable income

- Assisted reproductive service expenses (applicable on or after YA 2024/25)

- Qualifying premiums paid under the Voluntary Health Insurance Scheme (VHIS) policy

- Qualifying annuity premiums and tax-deductible mandatory provident fund (MPF) voluntary contributions

- Domestic rents

- Approved charitable donations

- Expenses of self-education

- Contributions to an MPF scheme or a recognized occupational retirement scheme

In addition to the tax deductions, tax allowances can be deducted from taxable income under the progressive tax rate – but not the standard tax rate. This means the standard tax rate only applies when you reach a very high income threshold, although the specific threshold will depend on the amount of personal allowances you receive.

|

Tax Deductions in Hong Kong |

|||

| YA | % of tax reduction | Maximum per case (HK$) | Applicable tax types |

| 2020/21 and 2021/22 | 100% | 10,000 | Profits tax, salaries tax, and tax under personal assessment |

| 2022/23 | 100% | 6,000 | Profits tax, salaries tax, and tax under personal assessment |

| 2023/24 | 100% | 3,000 | Profits tax, salaries tax, and tax under personal assessment |

| 2024/25 | 100% | 1,500 | Profits tax, salaries tax, and tax under personal assessment |

| 2025/26 * | 100% | 3,000 | Profits tax, salaries tax, and tax under personal assessment |

All taxpayers who pay salaries tax or elect personal assessment are entitled to a basic allowance to reduce their taxable income base. Some taxpayers can claim other allowances if they fulfill certain requirements that are related to family circumstances.

|

Personal Allowances in Hong Kong |

||

| Type | 2024/25 and 2025/26 (HK$) | 2026/27* and onwards (HK$) |

| Basic allowance | 132,000 | 145,000 |

| Married person’s allowance | 264,000 | 290,000 |

| Child allowance (for each of the first to ninth child) | 130,000 | 140,000 |

| For each child born during the year, the child allowance will be increased by: | 130,000 | 140,000 |

| Dependent brother or sister allowance (for each dependant) | 37,500 | 37,500 |

| Dependent parent and dependent grandparent allowance – aged 60 or above or eligible under disability allowance scheme | 50,000 | 55,000 |

| Dependent parent and dependent grandparent allowance – aged 55 to 59 | 25,000 | 27,500 |

| Additional dependent parent and dependent grandparent allowance – aged 60 or above or eligible under disability allowance scheme | 50,000 | 55,000 |

| Additional dependent parent and dependent grandparent allowance – aged 55 to 59 | 25,000 | 27,500 |

| Single parent allowance | 132,000 | 145,000 |

| Personal disability allowance | 75,000 | 75,000 |

| Disabled dependant allowance (for each dependant) | 75,000 | 75,000 |

| *Legislative amendments are required for implementing the tax measures as proposed by the Financial Secretary in the 2026-27 Budget. | ||

The annual income levels that an individual must reach based on their allowances before the standard rate applies are summarized in the table below.

|

Annual Income Levels Approaching Standard Salaries Tax Rate |

||

| YA 2026/27 (HK$) | YA 2024/25 & 2025/26 (HK$) | |

| Single | 2,132,500 | 2,022,000 |

| Married | 3,365,000 | 3,144,000 |

| Married + 1 child* | 4,555,000 | 4,249,000 |

| Married + 2 children* | 6,490,000 | 5,708,000 |

| Married + 3 children* | 8,870,000 | 7,918,000 |

| With two dependent parents or grandparents aged 60 or above: | ||

| Single | 3,067,500 | 2,872,000 |

| Married | 4,300,000 | 3,994,000 |

| Married + 1 child* | 5,980,000 | 5,198,000 |

| Married + 2 children* | 8,360,000 | 7,408,000 |

| Married + 3 children* | 10,740,000 | 9,618,000 |

| With two co-living dependent parents or grandparents, both aged 60 or above: | ||

| Single | 4,002,500 | 3,722,000 |

| Married | 5,470,000 | 4,844,000 |

| Married + 1 child^ | 7,850,000 | 6,898,000 |

| Married + 2 children^ | 10,230,000 | 9,108,000 |

| Married + 3 children^ | 12,610,000 | 11,318,000 |

| With one co-living dependent parent or grandparent aged 60 or above and one disabled dependent brother or sister: | ||

| Single | 4,023,750 | 3,828,250 |

| Married | 5,512,500 | 4,950,250 |

| Married + 1 child* | 7,892,500 | 7,110,500 |

| Married + 2 children* | 10,272,500 | 9,320,500 |

| Married + 3 children* | 12,652,500 | 11,530,500 |

| As a single parent with: | ||

| 1 child* | 4,555,000 | 4,249,000 |

| 2 children* | 6,490,000 | 5,708,000 |

| 3 children* | 8,870,000 | 7,918,000 |

| Note: Tax deductions not included.

*Not including the Additional Child Allowance in the year of birth |

||

Tax exemptions

Taxpayers can seek a complete or partial exemption of tax liabilities ot a tax credit if they have spent a considerable amount of time outside of Hong Kong in a given YA. The grounds for such an exemption are:

- Performing all services outside Hong Kong during a YA;

- Working outside Hong Kong, where that work was controlled and supervised outside Hong Kong, with aggregated time spent in Hong Kong during the YA not exceeding 60 days;

- Having paid income tax to a territory outside Hong Kong in respect of income derived from services rendered in that territory (where the territory does not have a comprehensive double taxation agreement or arrangement with Hong Kong); or

- Claiming double taxation relief by way of tax credit in respect of income derived from services rendered in a territory that has a comprehensive double taxation agreement or arrangement with Hong Kong (available to Hong Kong residents only).

Taxes for self-employed expats

Expats who are self-employed and do not have any earnings from formal employment can pay profits tax instead of salaries tax on their income. Hong Kong imposes a two-tiered profits tax system, with a rate of 7.5 percent applied to the first HK$2 million of profits, and 15 percent applied to the remaining profits.

If you simultaneously have earnings from employment and profits from self-employment, then you pay both salaries and profits tax on your respective income.

Profits tax paid by individuals must be declared through the annual Individual Tax Return (ITR), along with salaries tax if applicable.

As with earnings from employment, profits tax is only levied on profits arising from or derived in Hong Kong.

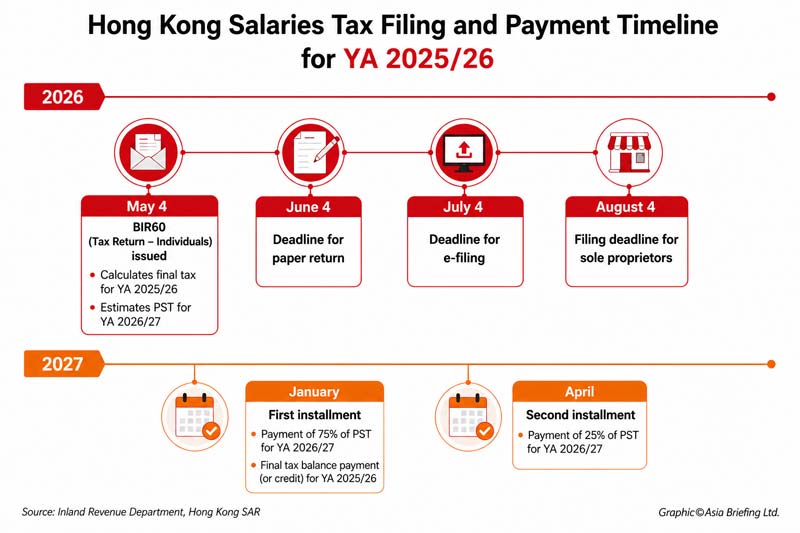

Filing and paying taxes in Hong Kong

Hong Kong does not have a withholding tax system, meaning the responsibility for filing and paying salaries tax lies with the individual.

While your employer does not need to file or pay taxes on your behalf, they do need to notify the IRD of chargeability by submitting Form IR56E after three months of the commencement of your terms of employment.

Salaries tax is paid on a provisional basis, usually in two instalments each year, after nine months (in January) and 12 months (in April). Provisional salaries tax (PST) is estimated based on your income in the previous tax year.

If your income for a given YA does not exceed the personal allowance threshold, you do not need to file or pay tax on that income for the YA.

| Item | Amount | |

| Total monthly income | 40,000 | |

| Contributions | MPF 1,500/month | |

| Total annual income | 40,000 x 12 | 480,000 |

| Less | MPF contributions (1,500 x 12) | 18,000 |

| Net total income | ||

| Less | Basic allowance (progressive rate only) | 145,000 |

| Net chargeable income (progressive) | 317,000 | |

| Net chargeable income (standard) | 462,000 | |

| SALARIES TAX PAYABLE | ||

| Progressive rate | ||

| First HK$50,000 | HK$50,000 x 2% | 1,000 |

| HK$50,000 – 100,000 | HK$50,000 x 6% | 3,000 |

| HK$100,000 – 150,000 | HK$50,000 x 10% | 5,000 |

| HK$150,000 – 200,000 | HK$50,000 x 14% | 7,000 |

| Over HK$200,000 | HK$117,000 x 17% | 19,890 |

| Balance | 35,890 | |

| Standard rate | ||

| First HK$5,000,000 | HK$462,000 x 15% | 69,300 |

PST is paid on the lower amount, so the PST payable for YA 2026/27 would be HK$35,890.

For the 2026/27 YA, salaries tax should be paid according to the following schedule:

| Amount payable |

Due date |

|

| 1st installment |

26,917.5 (75%) |

January 2027 |

|

2nd installment |

8,972.5 (25%) |

April 2027 |

Filing ITRs

Individual tax returns (IRDs) (Form BIR60) are issued to all taxpayers around the first working day of May of each year, through which taxpayers report their actual earnings in the previous YA. Based on the information provided on this form, the assessor will calculate the final tax payable on income from the previous YA and estimate PST for the new YA.

Taxpayers generally have one month to complete and submit the ITR; however, an automatic one-month extension is granted to all filings submitted electronically through the eTax portal. The deadline for sole proprietors is in August.

Taxpayers generally have one month to complete and submit the ITR; however, an automatic one-month extension is granted to all filings submitted electronically through the eTax portal. The deadline for sole proprietors is in August.

For first-time taxpayers, the IRD will issue an individual tax return (ITR) (Form BIR60 or BIR60C) within five months of receiving the notice of chargeability from your employer. You must then report the details of your income from your new employment, from which the assessor will estimate PST. You will then file your actual income through the ITR according to the normal timeline the following year.

Profits tax on any business income gained through a sole proprietorship is declared in Part 5 of the ITR.

For more information on filing ITRs, see our article: Filing Individual Tax Returns in Hong Kong: A Complete Guide

Payment of taxes

Taxes due can be paid through a range of different methods, including:

- Payment by Phone Service (PPS)

- Online (e-cheque, Faster Payment System)

- At a bank ATM (HSBC, Hang Seng Bank, or JETCO ATM)

- By post (crossed cheque and payment document)

- In person at a post office, convenience store, business registration office, or stamp office

Penalties for failure to file or pay tax

Failure to file or pay taxes on time can result in severe penalties and even criminal prosecution and imprisonment in severe cases. Errors in tax filing documents can also result in penalties, even if it was not intentional.

As salaries tax is only charged twice a year, rather than monthly as in many other jurisdictions, expats should also make sure to set aside a portion of earnings each month to ensure there are sufficient funds to pay taxes due when the time comes and avoid penalties for late payment of taxes.

Expats who are new to Hong Kong, in particular, are advised to seek professional help in order to ensure full compliance with their filing and payment obligations and avoid costly penalties.

Dezan Shira & Associates works with globally mobile professionals, foreign employees, and HR teams across Hong Kong to manage personal tax compliance. This includes individual income tax planning and optimization, advisory for expatriates and non-residents, and tax residency determination. The firm also handles annual income tax reconciliation and filing, provisional tax holdover applications, personal assessment elections, and allowance and deduction claims. For businesses managing internationally mobile staff, the team also advises on employer return compliance and tax clearance for departing employees.

Tax planning and compliance in Hong Kong require careful navigation of evolving local and international tax rules. Our experienced advisors support businesses with corporate tax, indirect tax, individual tax, international tax, and transfer pricing, helping them remain compliant while optimizing their tax position in Hong Kong and the wider Asia?Pacific region. About Us China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland. For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

![]()

![]()

- Previous Article Entering China: The Most Important Setup Decisions for Your Manufacturing Success

- Next Article