The Past, Present and Future of VAT Reform in China

SHANGHAI — At the start of 2012, China launched a massive reform to replace BT with VAT, two of the country’s three major indirect taxes. Prior to the reform, VAT was levied only on the sale and import of tangible goods and on the provision of processing, repair, and replacement services. Meanwhile, BT was levied on the provision of all other services as well as the transfer of intangible and real assets. In this article, we survey the past, present and future of VAT reform for its unavoidable and thoroughgoing consequences for foreign investors with operations in country.

VAT is considered a neutral tax, allowing businesses to offset VAT incurred in relevant purchases from their VAT liability. Conversely, BT is levied on gross turnover with no deduction permitted for tax paid when purchasing other goods or services. The two taxes are generally not mutually deductible. Replacing BT with VAT means that the risk of double taxation is eliminated, as the sale of goods and the provision of services will no longer be treated separately. This is expected to enhance the competitiveness of companies in the service sector and encourage them to upgrade their infrastructure. Under the VAT reform, enterprises will be able to deduct tax from the purchase of goods, fixed assets and services used in their business.

VAT payers are separated into two categories – general taxpayers and small-scale taxpayers – with tax rates varying between the two. The two categories are also associated with two distinct methods for calculating VAT payable: the general and simplified calculation methods are used for general and small-scale taxpayers, respectively.

General Calculation Method

- VAT payable = Current output VAT – Current input VAT

*Output VAT refers to the VAT amount calculated according to the sales volume of the taxable services provided and the applicable VAT rate.

**Input VAT refers to the VAT paid by the taxpayer when purchasing goods or receiving processing, repair and replacement services and other taxable services.

Simplified Calculation Method

Under the simplified calculation method, no input VAT is deductible and a uniform 3 percent levying rate applies:

- VAT payable = Sales volume * VAT levying rate (3 percent)

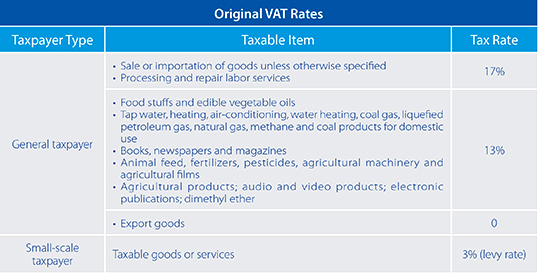

This chart below shows the original VAT (before the VAT reform) rates for different tax items:

Development

First implemented in Shanghai in 2012 for the transportation and certain modern service sectors, the VAT pilot reform was expanded to Beijing in September 2012, then to Jiangsu, Anhui, Fujian, Guangdong, Tianjin, Zhejiang, and Hubei later that same year. On August 1, 2013, the VAT pilot reform was implemented nationwide.

To date, the VAT pilot reform has been applied to railway transportation, postal services, telecom (starting June 1, 2014) and certain modern service sectors such as IT services and film and television services. By the end of June, 2014, the number of pilot taxpayers had increased by 690,000 to 3.42 million from 2.73 million, including 640,000 general taxpayers (19 percent) and 2.78 million small-scale taxpayers (81 percent).

RELATED: Implications of the VAT Reform in China

Furthermore, the VAT reform has substantially lessened the burden for enterprises, with more than 96 percent of taxpayers witnessing a decrease in their tax burden. During the first half of 2014, tax payable was reduced by RMB 85.1 billion due to the VAT reform, said Guo Xiaolin, spokesman for the State Administration of Taxation (SAT).

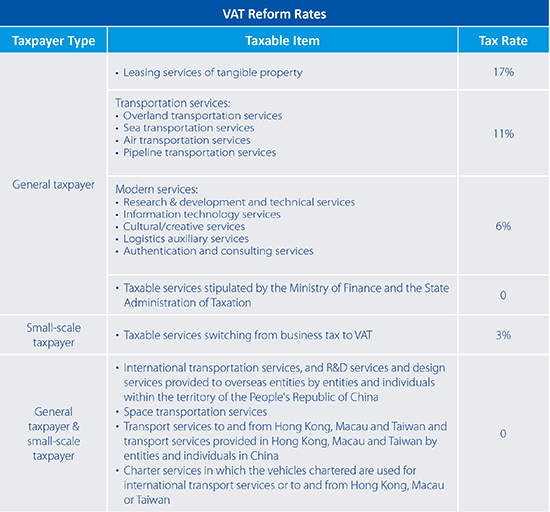

Details of the industries currently covered by the VAT reform and the relevant tax rates can be found below:

Future

The most definitive targets for the future of VAT reform in China are contained in the Twelfth Five Year Plan Period (2011-2015), which stipulates that all sectors currently subject to BT should have switched over to VAT by the end of the period. Reinforcing this, on July 28, 2014, the State Council released the “Circular on Accelerating the Development of the Production Services Industry and Promoting Industrial Restructuring and Upgrading (Guo Fa [2014] No.26)” which urged that VAT reform be expanded to all service sectors as soon as possible.

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email china@dezshira.com or visit www.dezshira.com.

Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

Related Reading

Revisiting China’s Value-Added Tax Reform

Revisiting China’s Value-Added Tax Reform

In this issue of China Briefing Magazine, we review recent steps taken by the Chinese government to reform its value-added tax policy. Specifically, we examine the sectors covered by the new Pilot Reform program with a focus on tax rates, taxpayer status and the calculation of VAT. We also include a VAT Pilot Reform Rates Chart, which overviews each affected industry’s tax rate and VAT exempted services.

The China Tax Guide: Tax, Accounting and Audit (Sixth Edition)

The China Tax Guide: Tax, Accounting and Audit (Sixth Edition)

This edition of the China Tax Guide, updated for 2013, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in China, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in China in order to effectively manage and strategically plan their China operations.

- Previous Article Neither Down nor Out: The Diverging Competitiveness of Manufacturing in China

- Next Article Revisiting the Shanghai Free Trade Zone: A Year of Reforms – New Issue of China Briefing Magazine