How to Remit Profits as Dividends in China

By Jim Qiao, Jenny Liao and Eunice Ku, Dezan Shira & Associates

SHANGHAI – For foreign companies with subsidiaries in China, repatriating cash from their subsidiaries has always been an important and challenging issue. China maintains a strictly regulated system of foreign exchange controls, meaning funds flowing into and out of China are tightly regulated. It is important to incorporate a profit repatriation strategy into the set-up planning for a subsidiary in China to ensure one’s ability to access the profits earned. Adopting the right strategy to optimize profit repatriation from China can result in significant cost savings.

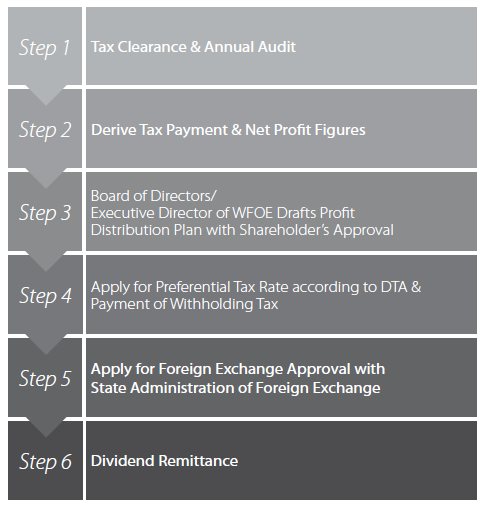

There are several ways of repatriating cash from China, the most obvious being for a company’s entity in China to pay dividends directly to its foreign parent company. Only profit that has undergone annual audit can be repatriated. Annual audit for tax compliance conducted by the local tax authority is usually completed around June or July every year (see accompanying timeline). The audit allows the State Administration of Taxation (SAT) to make sure all corporate income tax (CIT) has been paid up with regard to the profits being distributed. In addition, no profits can be distributed before losses from previous years have been made up, after which the remaining balance will be available for redistribution. The tax authorities will confirm how much a company can repatriate based on the net profit percentage.

RELATED: Dividend Repatriation: Limits and Tax Considerations in China

When remitting the funds, banks will generally require an audit report and annual CIT return to substantiate the distributable profit for the year. If the company chooses to postpone repatriation to the following year because of cash flow concerns, an additional special audit report will be required.

Not all profits can be repatriated or reinvested after tax clearance. A portion of the profit (at least 10 percent for WFOEs) must be placed in a company’s reserve fund account. This account is capped when the amount of reserves reaches 50 percent of the registered capital of the company. The investor can also choose to allocate some of the remainder to a staff bonus or welfare fund or an expansion fund, although these are not mandatory for WFOEs. Joint ventures are also required to allocate money for welfare funds, staff incentives, and the enterprise development funds (for investment purposes), with the exact percentages determined by the Board of Directors.

Not all profits can be repatriated or reinvested after tax clearance. A portion of the profit (at least 10 percent for WFOEs) must be placed in a company’s reserve fund account. This account is capped when the amount of reserves reaches 50 percent of the registered capital of the company. The investor can also choose to allocate some of the remainder to a staff bonus or welfare fund or an expansion fund, although these are not mandatory for WFOEs. Joint ventures are also required to allocate money for welfare funds, staff incentives, and the enterprise development funds (for investment purposes), with the exact percentages determined by the Board of Directors.

China levies withholding CIT on profits or dividends repatriated to non-resident taxpayers, with the amount varying from 0 percent to 10 percent depending on the stipulations of the relevant DTA. Dividends connected to profits made prior to January 1, 2008 are exempt from this withholding tax.

Procedure for the Declaration & Repatriation of Dividends

This article is an excerpt from the June 2014 edition of China Briefing Magazine, titled “Strategies for Repatriating Profit from China.” In this issue, we guide you through the different channels for repatriating profits, including via intercompany expenses (i.e., charging service fees and royalties to the Chinese subsidiary) and loans. We also cover the requirements and procedures for repatriating dividends, as well as how to take advantage of lowered tax rates under double tax avoidance treaties.

This article is an excerpt from the June 2014 edition of China Briefing Magazine, titled “Strategies for Repatriating Profit from China.” In this issue, we guide you through the different channels for repatriating profits, including via intercompany expenses (i.e., charging service fees and royalties to the Chinese subsidiary) and loans. We also cover the requirements and procedures for repatriating dividends, as well as how to take advantage of lowered tax rates under double tax avoidance treaties.

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email china@dezshira.com or visit www.dezshira.com.

Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

- Previous Article Remitting Royalties from China: Procedures and Requirements

- Next Article China Agrees to FATCA Compliance