China’s Import-Export Trends 2024-25: A Comprehensive Review of the First 10 Months

The recently released foreign trade statistics for October and the first 10 months of 2024 reveal significant trends in China’s import-export activities for 2024-25. We will explore these trends by examining the trading structure, methods, partners, products, and sectors involved.

On November 7, 2024, the General Administration of Customs (GAC) released statistics showing that China’s goods exports in October far exceeded expectations. Exports increased by 11.2 percent year-on-year in RMB terms and 12.7 percent in dollar terms, marking the largest expansion since March 2023.

In the first 10 months of 2024, the total value of China’s goods trade reached 36.02 trillion RMB (US$5.05 trillion), reflecting a 5.2 percent year-on-year increase. This includes 20.8 trillion RMB (US$2.89 trillion) in exports (up 6.7 percent) and 15.22 trillion RMB (US$2.09 trillion) in imports (up 3.2 percent). Notably, the trade surplus expanded by 17.6 percent, reaching 5.58 trillion RMB (US$770 billion).

In this article, we analyze China’s import-export trends in 2024 by delving into the statistics for the first 10 months.

October’s goods exports exceeded expectations

In October, China’s total import and export value reached RMB 3.7 trillion (US$520 billion), marking a 4.6 percent year-on-year increase, which is nearly 4 percentage points higher than the growth rate in September. Exports amounted to RMB 2.19 trillion (US$305 billion), reflecting an 11.2 percent increase, while imports totaled RMB 1.51 trillion (US$210 billion), a 3.7 percent decline. The trade surplus for October was RMB 679.1 billion (US$95 billion).

The double-digit growth in exports for October can be attributed to various factors:

- Dissipation of short-term disruptions: The impact of extreme weather, global shipping disruptions, and anticipated strikes by dockworkers on the U.S. East Coast in September significantly affected exports. These disruptions have lessened to varying degrees in October.

- Lower year-on-year comparison base: In October of last year, exports fell by 7.5 percent, which is notably lower than the average decline of 3.9 percent over the past decade.

- Strong growth in new export drivers: Preliminary data from the Ministry of Commerce (MOFCOM) indicates that cross-border e-commerce exports grew by 15.2 percent year-on-year in the first three quarters, outpacing the overall export growth by 9 percentage points. The trading environment in October showed no significant changes, suggesting that cross-border e-commerce will continue to experience high growth.

- Resilience in external demand: Current external demand remains somewhat resilient, supported by strong trends in the U.S. economy.

The strong performance in export growth and trade surplus in October indicates that foreign trade continues to contribute significantly to economic growth. Coupled with unexpected counter-cyclical policy measures domestically, this will further enhance market confidence in achieving annual economic targets.

However, it is important to note that imports and exports saw a month-on-month decline of 1.2 percent in October. This decline is primarily due to weak domestic demand, cautious import decisions by market participants, low prices for bulk commodities, and the impact of a higher comparison base from last year.

China’s import-export trends revealed in the first 10 months

Trade methods

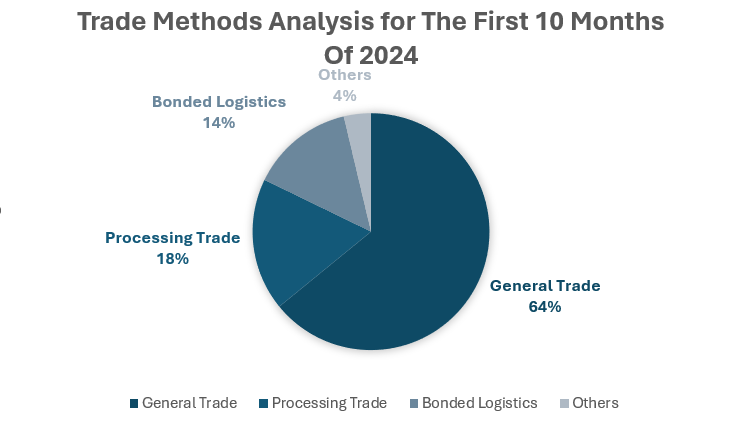

General trade remains the leader, while trade through bonded logistics is experiencing robust growth

In the first 10 months of 2024, China’s import-export trade structure showcases a diverse and evolving landscape. General trade remains the dominant category, accounting for 64.1 percent of the total trade value. The value of general trade reached RMB 23.09 trillion (US$3.23 trillion), with a growth of 3.9 percent in this sector. Exports in general trade reached RMB 13.58 trillion (US$1.91 trillion), indicating steady demand for Chinese goods in global markets.

Processing trade, which constitutes 18.1 percent of the total, experienced a slightly higher growth rate of 4 percent, with exports totaling RMB 4.13 trillion (US$0.58 trillion) and imports at RMB 2.4 trillion (US$0.34 trillion), reflecting a positive trend in this area.

Additionally, trade through bonded logistics has emerged as a significant contributor, with a notable 14 percent increase in trade volume, totaling RMB 5.09 trillion (US$0.71 trillion). This segment underscores the growing importance of logistics and supply chain efficiency in facilitating international trade, with exports rising by 11.5 percent to RMB 1.96 trillion (US$0.28 trillion) and imports increasing by 15.7 percent to RMB 3.13 trillion (US$0.44 trillion).

Overall, while general trade continues to lead, the increasing contributions from bonded logistics and the steady growth in processing trade indicate a shift towards more integrated and efficient trade practices, positioning China favorably in the global market.

|

Trade Type Analysis of the First 10 Months 2024 |

|||||||

| Trade type | Ratio of total trade (%) | Total (RMB trillion) | Growth rate (%) | Export (RMB trillion) | Export growth rate (%) | Import (RMB trillion) | Import growth rate (%) |

| General Trade | 64.1 | 23.09 | 3.9 | 13.58 | 7.8 | 9.51 | -1.2 |

| Processing Trade | 18.1 | 6.53 | 4.0 | 4.13 | 1.6 | 2.40 | 8.3 |

| Bonded Logistics | 14.1 | 5.09 | 14.0 | 1.96 | 11.5 | 3.13 | 15.7 |

Source: GAC

Trading partners

Trade with ASEAN, the EU, the United States, and South Korea continues to increase

Based on the trade data for the first 10 months of 2024, several key trends emerge regarding China’s trade relationships with its major partners:

- ASEAN as the leading partner: ASEAN has solidified its position as China’s largest trading partner, with a total trade value of RMB 5.67 trillion (US$0.79 trillion), reflecting an 8.8 percent growth. Notably, exports to ASEAN increased by 12.5 percent, indicating strong demand for Chinese goods. The trade surplus with ASEAN expanded significantly by 38.2 percent, reaching RMB 1.05 trillion (US$0.15 trillion), highlighting a favorable trade balance.

- Stable growth with the EU: The European Union (EU) remains China’s second-largest trading partner, with a total trade value of RMB 4.64 trillion (US$0.65 trillion), growing by 1.2 percent. Exports to the EU rose by 3.5 percent, while imports decreased by 2.9 percent, resulting in an increased trade surplus of RMB 1.44 trillion (US$0.20 trillion), up 11.6 percent. This suggests a shift towards a more favorable trade balance with the EU.

- Consistent trade with the USA: The United States is China’s third-largest trading partner, with a total trade value of RMB 4.01 trillion (US$0.56 trillion), growing by 4.4 percent. Exports to the U.S. increased by 4.9 percent, while imports grew by 2.9 percent, leading to a trade surplus of RMB 2.07 trillion (US$0.29 trillion), which expanded by 5.8 percent. This indicates a stable trade relationship despite ongoing geopolitical tensions.

- Mixed results with South Korea: South Korea ranks as the fourth-largest trading partner, with a total trade value of RMB 1.91 trillion (US$0.27 trillion), growing by 6.7 percent. However, exports to South Korea declined by 0.8 percent, while imports surged by 13.8 percent, resulting in a significant trade deficit of RMB 1.99 trillion (US$0.28 trillion), which has more than doubled. This trend suggests a growing reliance on South Korean imports.

- Belt and Road Initiative impact: Trade with countries involved in the Belt and Road Initiative totaled RMB 16.94 trillion (US$2.37 trillion), growing by 6.2 percent. Exports to these countries increased by 8 percent, while imports rose by 3.9 percent. This reflects the ongoing commitment to enhancing trade ties with Belt and Road nations, contributing positively to China’s overall trade landscape.

| Trade Partner Analysis of the First 10 Months 2024 | |||||||||

| Trading partner | Ratio of total (%) | Total trade (RMB trillion) | Growth rate (%) | Exports (RMB trillion) | Export growth rate (%) | Imports (RMB trillion) | Import growth rate (%) | Trade surplus/deficit (RMB trillion) | Surplus growth rate (%) |

| ASEAN | 15.7 | 5.67 | 8.8 | 3.36 | 12.5 | 2.31 | 3.8 | 1.05 | 38.2 |

| EU | 12.9 | 4.64 | 1.2 | 3.04 | 3.5 | 1.60 | -2.9 | 1.44 | 11.6 |

| US | 11.1 | 4.01 | 4.4 | 3.04 | 4.9 | 0.97 | 2.9 | 2.07 | 5.8 |

| South Korea | 6.7 | 1.91 | 6.7 | 0.86 | -0.8 | 1.05 | 13.8 | -1.99 | 110.0 |

| Belt and Road countries | 46.9 | 16.94 | 6.2 | 9.48 | 8.0 | 7.46 | 3.9 | N/A | N/A |

Source: GAC

Trade players

Private enterprises and FIEs see growth in foreign trade

The trade data of the first 10 months highlights the dominant role of private enterprises in China’s trade landscape, contributing significantly to both exports and imports. In contrast, foreign-invested enterprises (FIEs) show slower growth, while state-owned enterprises (SOEs) are experiencing a decline, particularly in imports.

Private enterprises have demonstrated strong performance, with total trade reaching RMB 19.85 trillion (US$2.79 trillion), marking a growth of 9.3 percent. This segment accounts for 55.1 percent of China’s total foreign trade, an increase of 2.1 percentage points compared to the previous year.

Exports from private enterprises totaled RMB 13.37 trillion (US$1.87 trillion), also growing by 9.3 percent, which represents 64.3 percent of China’s total exports. Imports stood at RMB 6.48 trillion (US$0.91 trillion), reflecting the same growth rate of 9.3 percent and constituting 42.6 percent of total imports.

This robust performance underscores the vital role of private enterprises in driving China’s trade growth.

FIEs reported a total trade value of RMB 10.61 trillion (US$1.48 trillion), with a modest growth of 1.3 percent. This segment represents 29.5 percent of the total trade. Exports from these enterprises reached RMB 5.77 trillion (US$0.81 trillion), growing by 1.9 percent, while imports were RMB 4.84 trillion (US$0.68 trillion), with a minimal increase of 0.5 percent.

The slower growth rates compared to private enterprises may indicate challenges in this sector, possibly due to changing global market dynamics or regulatory environments.

SOEs faced a decline in trade performance, with total trade amounting to RMB 5.48 trillion (US$0.77 trillion), down 0.5 percent. This segment accounts for 15.2 percent of total trade. Exports from SOEs grew by 4.2 percent to RMB 1.63 trillion (US$0.23 trillion), indicating some resilience in their export activities. However, imports fell to RMB 3.85 trillion (US$0.54 trillion), down 2.3 percent, reflecting potential challenges in sourcing or increased competition from private and foreign-invested enterprises.

| Foreign Trade Analysis by Type of Enterprises for the First 10 Months of 2024 | |||||||

| Type of Enterprise | Total trade (RMB trillion) | Growth rate (%) | Exports (RMB trillion) | Export growth rate (%) | Imports (RMB trillion) | Import growth rate (%) | Share of total trade (%) |

| Private enterprises | 19.85 | 9.3 | 13.37 | 9.3 | 6.48 | 9.3 | 55.1 |

| FIEs | 10.61 | 1.3 | 5.77 | 1.9 | 4.84 | 0.5 | 29.5 |

| SOEs | 5.48 | -0.5 | 1.63 | 4.2 | 3.85 | -2.3 | 15.2 |

Source: GAC

Product structure

Electromechanical products constitute nearly 60% of China’s exports

Overall, China’s trade trends indicate a strong performance in high-tech and electromechanical products, with significant growth in integrated circuits and automobiles. While labor-intensive products show more modest growth, agricultural exports remain stable. The mixed results in metal and fuel exports highlight the complexities of global demand and supply dynamics. These trends reflect China’s ongoing transition towards a more technology-driven economy while maintaining its traditional manufacturing strengths.

Electromechanical products constitute a significant portion of China’s exports, accounting for 59.4 percent of the total export value. In the first 10 months, exports in this category reached RMB 12.36 trillion (US$1.73 trillion), growing by 8.5 percent. In October, exports of electromechanical products reached US$18.798 billion, setting a new monthly record for the past two years and marking a 14.4 percent year-on-year increase, the highest growth rate of the year. This significant rise can be attributed to last year’s lower comparison base and some shipment delays caused by September’s weather conditions. This robust performance highlights the strength of China’s manufacturing sector, particularly in high-tech and machinery products.

Strong growth was observed in the key subcategories below:

- Automatic data processing equipment and components: Exports in this segment totaled RMB 1.2 trillion (US$0.17 trillion), with a growth rate of 10.9 percent. This reflects the increasing global demand for computing and data processing technologies.

- Integrated circuits: Exports surged to RMB 931.17 billion (US$130 billion), marking an impressive 21.4 percent growth. This trend underscores China’s pivotal role in the global semiconductor supply chain.

- Automobiles: Exports reached RMB 698.54 billion (US$97 billion), growing by 20 percent. In October alone, automobile exports totaled US$10.68 billion, marking a 4 percent year-on-year increase and exceeding US$10 billion for the third consecutive month. From January to October, cumulative exports reached 5.285 million vehicles, reflecting a 24.8 percent increase, surpassing the total export volume for all of 2023. This growth indicates a rising acceptance of Chinese automotive products in international markets.

Exports of labor-intensive products in China totaled RMB 3.48 trillion (US$0.49 trillion), reflecting a growth of 3.2 percent and accounting for 16.7 percent of total exports. Within this category, clothing and accessories saw exports of RMB 932.75 billion (US$130 billion), with a modest growth of 0.7 percent. Textiles performed slightly better, increasing by 5.8 percent to reach RMB 829.52 billion (US$116 billion). Additionally, plastic products experienced growth of 7.4 percent, totaling RMB 615.58 billion (US$86 billion). These figures indicate a stable demand for labor-intensive products, although their growth rates are lower compared to the more robust increases seen in high-tech items.

In the metal and fuel sector, steel exports saw a significant increase of 23.3 percent, totaling 9.19 million tons, which reflects strong global demand, particularly for construction and infrastructure projects. Conversely, finished oil exports experienced a decline of 7.2 percent, dropping to 4.92 million tons, suggesting a potential oversupply or reduced demand in key markets. Meanwhile, fertilizer exports remained stable, with a slight increase of 0.6 percent, totaling 2.59 million tons. This mixed performance highlights the varied dynamics within the metal and fuel export markets.

In the same period, imports of electromechanical products reached RMB 5.75 trillion (US$0.80 trillion), reflecting a growth of 8.6 percent. Notably, integrated circuits accounted for 455.62 billion units, marking a 15 percent increase, with a total value of RMB 2.24 trillion (US$0.31 trillion), which grew by 13 percent. However, automobile imports saw a decline, with 577,000 units imported, down 9.3 percent, and their total value decreased by 13 percent to RMB 233.44 billion (US$32.5 billion). This data highlights the strong demand for integrated circuits while indicating challenges in the automotive sector.

China’s import-export trends and outlook for 2024-25

The incremental fiscal policies introduced since late September are expected to boost a continued recovery in import demand as we approach the end of the year. Additionally, the impact of rising international commodity prices observed in late September and early October is likely to become more pronounced, affecting import prices. Overall, with slight improvements in both import volume and price, along with a lower year-on-year comparison base, November is anticipated to show positive year-on-year growth in imports.

On the export side, there are mixed signals. China’s robust industrial system, combined with ongoing optimization and enhancement of its trade structure and quality, positions the country favorably. In the electromechanical sector, the resilience and competitiveness of China’s supply in finished goods, intermediate goods, and capital goods are expected to become more evident as the global economy improves and demand recovers.

However, concerns persist regarding geopolitical issues, trade friction, and chaotic competition within industries, which may impact business expectations. Demand from traditional markets, particularly in Europe and the U.S., is showing signs of slowing down, potentially disrupting China’s foreign trade. Furthermore, the lack of long-term and forward orders is a significant issue that warrants attention, as it could place pressure on electromechanical exports in 2025.

In summary, while challenges lie ahead—especially in the export sector—the overall outlook for China’s trade remains stable, supported by strong domestic capabilities and strategic policy measures. The ability to adapt to changing global conditions will be crucial for sustaining growth in both imports and exports.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Trump Wins the 2024 US Presidential Election: Implications for China

- Next Article China-Indonesia Closer Economic Ties: Trade and Investment Opportunities