Clean Energy Investing in China

By Roy K. McCall

Foreign investors visiting China receive a personal introduction to clean energy—or at least its importance. With every breath, one is reminded that China relies on coal for 65-70 percent of its energy needs—40 percent above the world average—and leads the world in carbon emissions. The latest annual environmental report revealed that acid rain fell upon 44 percent of Chinese cities. If China is serious about improving air quality, then coal and carbon energy will need to be replaced by renewable clean energy, namely wind, solar, hydropower, biomass and other viable alternatives such as geothermal and ocean energy.

Globally, clean energy investments in 2013 still trailed investment into fossil fuel by US$43 billion. Last year marked the first time ever that China invested more in renewable energy than Europe, and thereby led the world. Though compared to the year before, total investment was down in several countries around the world: China by 6 percent to $54.2 billion; Europe by 42 percent to $55 billion; the U.S. by 9 percent to US$36 billion; India by 15 percent to $6 billion; and Brazil by a whopping 55 percent to $3 billion—its lowest since 2005. Exceptionally, Japan’s solar boom helped to drive an 80 percent jump in renewable energy investment to US$29 billion in 2013.

China has also built the world’s largest renewable energy capacity of 191 GW. In 2013, the country installed a record 12.1 GW of solar and 14 GW of wind energy capacity. Its stated goals for 2014 includes 14 GW of new solar capacity and 18 GW of new wind capacity.

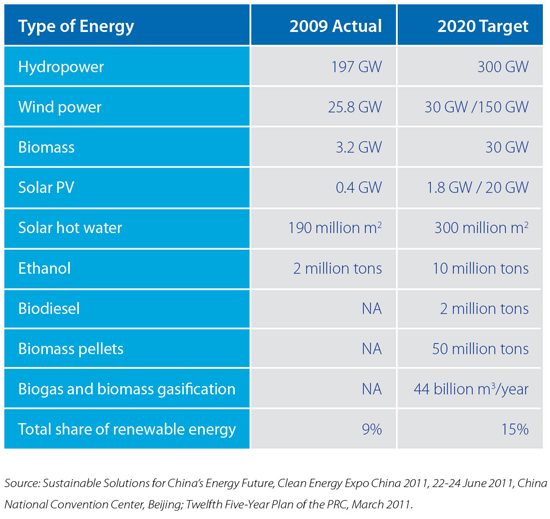

China aims to increase the share of renewable energy (excluding natural gas and nuclear) in its overall energy profile from 9 percent in 2009 to 15 percent or more by 2020:

Where are the opportunities for foreign investment? Hydropower would appear the obvious answer. China is already home to a fifth of the world’s hydropower capacity and half of its largest dams. The Three Gorges Dam on the Yangtze, the world’s largest, generates 22.5 GW—about 14 percent of China’s total hydropower and 1 percent of its total energy. Moreover, China aims to add 15 GW of hydropower per year. Currently, the government is focused on building large dams on the Yangtze and Yellow rivers and their tributaries, such as the Jinsha. The latter is the site of the Xiangjiaba Dam—with eight giant 800 MW turbines, the largest in the world. These projects require capital, long investment horizons, and household relocation projects suitable only for bulk investment banks and MNCs.

Other hydropower investors in China have focused on smaller dams scattered between Yunnan and Fujian. One such firm is CHC (China Hydroelectric Corporation) with 25 dams generating 0.5 GW (518MW). In 2011, during the sell-off of U.S. listed Chinese stocks, CHC fell about 90 percent, resulting in a shareholder revolt that forced out the founder and CEO. Despite this, the company continued to suffer at the mercy of rainfall, and from tariffs imposed by the National Development and Reform Commission (NDRC), resulting in a string of uncontrollable losses. After investment cuts allowed the company to return to a positive cash flow, CHC announced in 2014 that it would merge with clean energy fund NewQuest.

Wind energy in China is currently over capacity, with little room for expansion. Domestic wind farms are prevalent in Inner Mongolia and Yunnan, with few other installation destinations available, except abroad. OECD markets are now sensitive to China underselling their own industries, driving China-based exporters to South America and Africa, where wind power can compete with coal. But the wind energy sector may be headed for a capacity correction much like the solar industry of two years ago.

RELATED: The East is Green: The Future of China’s Environmental Regime (Part 1 and 2)

China recently invested massive resources into producing solar cells for the rest of the world, especially Germany — which currently derives about 4.5 percent of its electricity needs from solar power, and aims to produce at least 80 percent of its energy via renewables by 2050 under its Energiewende policy. China’s solar industry then overexpanded, overleveraged, and when German subsidies moderated, Chinese producers needed to be rescued by the PRC government. With reduced leverage and lowered production capacity, China’s solar industry now seems to be stabilizing.

It also helped that in September 2013 the NDRC newly established a 0.42 RMB/KWH subsidy for distributed PV (photovoltaic) units. Previously, the Central Government had subsidized clean energy equipment producers only on a project basis—a form of “cost-push.” Now, it has introduced distributed consumption, a “demand-pull.” But given that China has already cut capacity to strengthen pricing and fight domestic firm bankruptcies, it is unlikely to welcome additional foreign investment in solar power, unless it remains committed to pushing solar power in Tibet and displacing over 160,000 tons of burning coal.

Biomass, plant-based fuel, has been a focus of China’s large-scale SOEs such as CNPC (China National Petroleum Corporation), Sinopec, CNOOC (China National Offshore Oil Corporation), COFCO (China Oil and Food Import and Export Corporation) and others—some of which are cooperating with European technology leaders in this regard.

Natural gas represents a non-renewable but clean source of energy, contributing 4 percent of China’s total energy needs. Consumption first outstripped supply in 2009 and has since continued to do so. As a result, China has considered overland natural gas pipelines from the west (including Central Asia, Myanmar, and Russia) and imported LNG from the coast. Global leaders in natural gas such as Shell have been active in China. Opportunities for large-scale foreign investment are to be found in exploration, production, and pipeline development in areas where domestic competition is limited (e.g., the Ordos, Sichuan and Talim basins).

Investment into China’s clean energy sector may be “hot” but related political issues—such as domestic grid rates and dumping allegations by foreign countries—have been known to “cool off” returns, beaconing a range of consultants to sell advice without risking principal.

Nevertheless, for serious investors, three opportunities remain glaringly open. Real estate developers can build “greener” offices and homes—powered by anything other than coal. Secondly and on the supply side, the challenge is to build a more efficient electrical grid through which to move electricity. Thirdly, innovation in lowering vehicle emissions is needed to clean up vehicle pollution. In a word, efficiency on both the demand and supply sides will remain an important theme for successful investors.

Roy K. McCall CFA/CPA recently advised on clean energy investments in China and has written a case on clean energy investing in China. Roy wrote a thesis on clean energy while a second year student at Harvard Business School 1983-1984.

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email china@dezshira.com or visit www.dezshira.com.

Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

Related Reading

Adapting Your China WFOE to Service China’s Consumers

Adapting Your China WFOE to Service China’s Consumers

In this issue of China Briefing Magazine, we look at the challenges posed to manufacturers amidst China’s rising labor costs and stricter environmental regulations. Manufacturing WFOEs in China should adapt by expanding their business scope to include distribution and determine suitable supply chain solutions. In this regard, we will take a look at the opportunities in China’s domestic consumer market and forecast sectors that are set to boom in coming years.

Industry Specific Licenses and Certifications in China

In this issue of China Briefing, we provide an overview of the licensing schemes for industrial products; food production, distribution and catering services; and advertising. We also introduce two important types of certification in China: the CCC and the China Energy Label (CEL). This issue will provide you with an understanding of the requirements for selling your products or services in China.

- Previous Article China-Switzerland Free Trade Agreement Comes Into Force

- Next Article China’s Rising Manufacturing Costs: Challenges and Opportunities