April-May Hong Kong Tax Compliance: A Practical Checklist for Businesses

Hong Kong tax compliance April May 2026 brings four IRD returns, new e‑filing rules, and tighter deadlines. Many businesses struggle to track these overlapping requirements, especially with the mandatory iXBRL and MNE e‑filing requirements. This checklist breaks down what to file, when to file, and how to stay compliant without last‑minute stress.

Hong Kong’s April–May filing season is always busy, but the 2026 cycle is particularly demanding. The IRD issues four major tax returns (profits, property, employer, and personal income) within a short window, while new e‑filing rules, iXBRL tagging, and mandatory requirements for large multinational enterprise (MNE) groups add extra pressure. Missing a deadline or misunderstanding the new rules can lead to penalties or unnecessary audit exposure.

This guide provides a practical, Hong Kong–specific checklist based on the IRD’s 1 April 2026 announcements. It helps businesses, tax teams, and representatives stay ahead of the April-May compliance crunch.

Filing requirements and deadlines

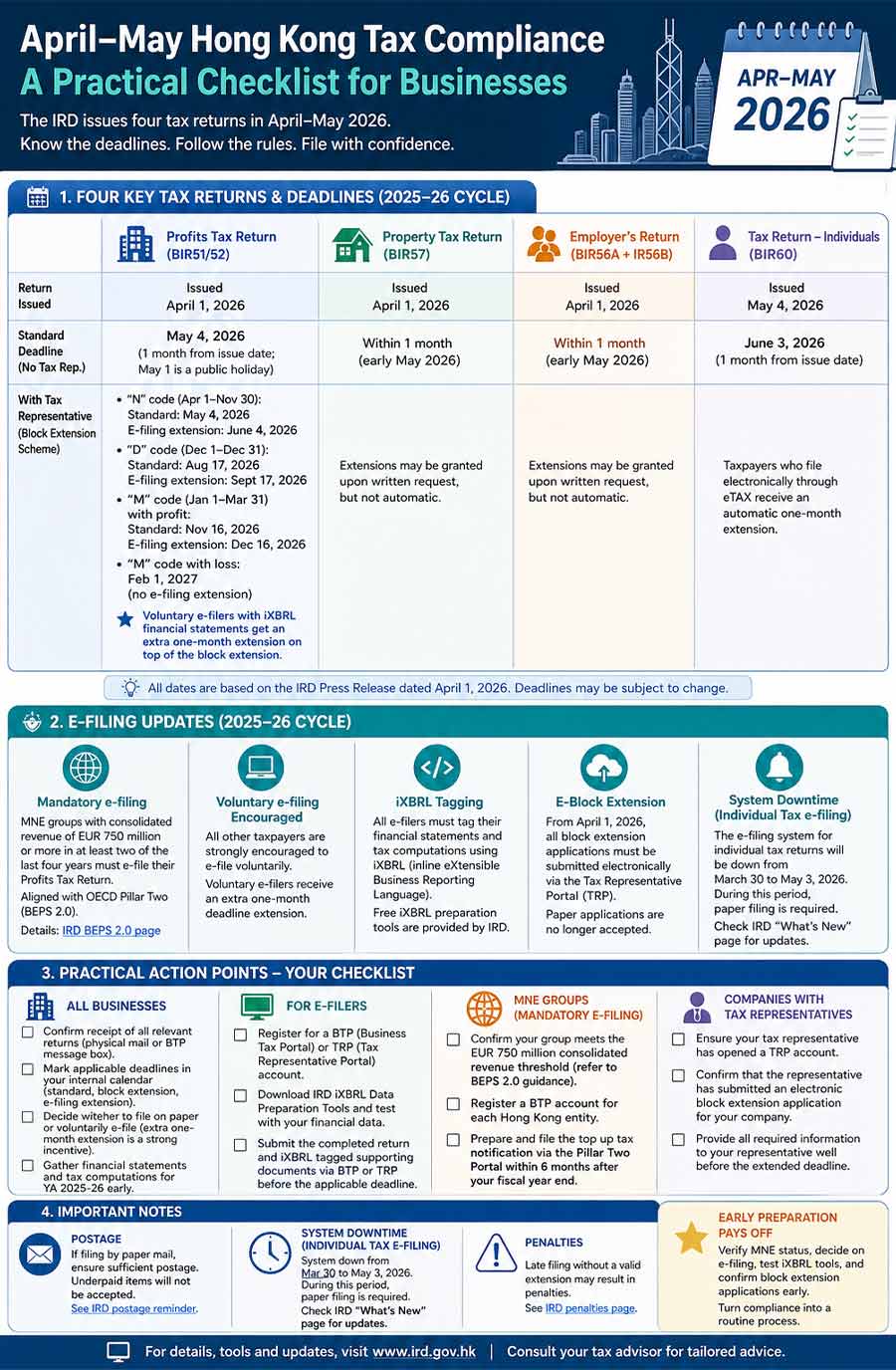

Profits Tax Return (BIR51/52)

The IRD issued the 2025-26 Profits Tax Return on April 1, 2026. Filing deadlines depend on whether the company has a tax representative and its accounting year‑end.

Before diving into the dates, businesses should confirm whether they fall under the Block Extension Scheme and whether they plan to e‑file (which provides an extra one‑month extension).

Companies without a tax representative: The filing deadline is May 4, 2026 (one month from issue, adjusted for the May 1 holiday). Read more: Hong Kong Public Holidays 2026 Schedule

Companies with a tax representative: The Block Extension Scheme applies. Detailed deadlines by code category are set out in the IRD’s Circular to Tax Representatives:

- “N” code (accounting year end April 1 to November 30): standard deadline May 4, 2026; e-filing extension to June 4, 2026.

- “D” code (December 1 to December 31): standard deadline August 17, 2026; e-filing extension to September 17, 2026.

- “M” code (January 1 to March 31) with profit: standard deadline November 16, 2026; e-filing extension to December 16, 2026.

- “M” code with loss: February 1, 2027 (no e-filing extension).

Voluntary e-filers: Taxpayers who voluntarily e-file and submit iXBRL financial statements receive an additional one-month extension on top of the block extension. Read more: Beyond Compliance: How to Approach Hong Kong’s 2026 Profits Tax Return

Property Tax Return (BIR57)

The Property Tax Return (BIR57) is also part of the IRD’s April issuance cycle and was released on April 1, 2026. The filing deadline is one month later (early May 2026). In practice, businesses should expect to mail or e-file by around May 4, 2026, given the May 1 holiday.

Although the filing window is relatively short, property owners often underestimate the time needed to gather rental income records, tenancy agreements, and allowable deductions. Any discrepancies between reported rental income and lease documents can trigger follow‑up questions from the IRD, so early preparation is essential. Landlords should also confirm whether any periods of vacancy, rent concessions, or agent commissions have been properly documented before completing the return.

Employer’s Return (BIR56A + IR56B)

Issued on April 1, 2026. The standard deadline is within one month (early May 2026). Extensions may be granted upon written request, but they are not automatic.

The Employer’s Return package, issued on April 1, 2026, requires employers to report all employee remuneration for the 2025-26 tax year. The standard filing deadline falls in early May, leaving a narrow window to compile payroll data, bonus records, share‑based compensation details, and departure notifications. While extensions may be granted, they are not automatic, and the IRD expects employers to justify the need for additional time. Businesses with large workforces or complex compensation structures should begin data consolidation immediately to avoid late filing penalties and ensure accurate reporting for each employee.

Read more: Hong Kong Employer’s Return 2026 Opens: Are You Ready?

Tax Return – Individuals (BIR60)

The Tax Return – Individuals (BIR60) is issued later in the cycle, on May 4, 2026, with a standard filing deadline of June 3, 2026. Many taxpayers rely on the IRD’s automatic one‑month extension available through eTAX, which extends the deadline to early July. However, individuals with multiple income sources, such as rental income, sole proprietorship profits, or overseas employment, should begin gathering supporting documents early to avoid last‑minute issues. Those expecting provisional tax adjustments or claiming deductions (e.g., MPF voluntary contributions, charitable donations, home loan interest) will benefit from preparing their records ahead of time to ensure a smooth filing process.

E-filing updates 2025-26

Hong Kong’s digital filing requirements continue to expand. Businesses should review the following changes before preparing their returns for the 2025-26 tax year.

Mandatory e-filing

MNE groups with consolidated revenue of EUR 750 million or more in at least two of the last four years must e-file their Profits Tax Return. This threshold aligns with the OECD’s Pillar Two rules.

Read more: A Guide to Global Minimum Tax in Hong Kong – Compliance Requirements for MNEs (Part II)

Voluntary e-filing encouraged

All other taxpayers are strongly encouraged to e-file voluntarily. As an incentive, voluntary e-filers receive a one‑month extension, making digital filing the more flexible option.

iXBRL tagging

All e-filers must tag their financial statements and tax computations in iXBRL (inline extensible business reporting language). The IRD provides free iXBRL preparation tools, but testing them early is essential.

E-Block Extension

From April 1, 2026, all block extension applications must be submitted electronically via the Tax Representative Portal (TRP). Paper applications are no longer accepted.

Practical action points for businesses

For all businesses

- Confirm receipt of all relevant returns (check physical mail or your BTP message box).

- Mark the applicable deadlines in your internal calendar, distinguishing standard, block extension, and e-filing extension dates.

- Decide early whether to file on paper or voluntarily e-file. The extra one-month extension is a strong incentive to go digital.

- Gather financial statements and tax computations for the year of assessment 2025-26 well ahead of time.

For e-filers

- Register for a BTP (Business Tax Portal) or TRP (Tax Representative Portal) account. BTP is for businesses filing on their own; TRP is for tax representatives.

- Download the IRD iXBRL Data Preparation Tools and test them with your financial data.

- Submit the completed return and iXBRL‑tagged supporting documents via BTP or TRP before the applicable deadline.

For MNE groups (mandatory e-filing)

- Confirm whether the group meets the EUR 750 million consolidated revenue threshold. Refer to the BEPS 2.0 guidance.

- Register a BTP account for each Hong Kong entity.

- Prepare and file the top‑up tax notification via the Pillar Two Portal within six months after your fiscal year‑end.

For companies with tax representatives

- Make sure your tax representative has an active TRP account.

- Confirm that the representative has submitted an electronic block extension application for your company.

- Provide all required information to your representative well before the extended deadline.

Important notes for 2026

- Postage: If filing by paper mail, ensure sufficient postage. Underpaid items will not be accepted (More details in IRD’s postage reminder).

- System downtime: The e-filing system for individual tax returns will be down from March 30 to May 3, 2026. During this period, paper filing is required for individual tax return (More details in IRD’s What’s New).

- Penalties: Late filing without a valid extension can lead to penalties. Businesses should consult the IRD’s Penalty Policy or seek professional advice if unsure (More details on the IRD’s penalties page).

Key takeaway

Staying ahead of the April-May Hong Kong tax compliance cycle requires more than just noting dates. Businesses should verify their MNE status, decide on e-filing, test iXBRL tools, and confirm that tax representatives have submitted electronic block extension applications. Early preparation turns compliance from a scramble into a routine process. Companies are advised to consult their tax advisors and monitor the IRD website for any further updates.

(Source: IRD, Asia Briefing; AI-powered image)

Tax planning and compliance in Hong Kong require careful navigation of evolving local and international tax rules. Our experienced advisors support businesses with corporate tax, indirect tax, individual tax, international tax, and transfer pricing, helping them remain compliant while optimizing their tax position in Hong Kong and the wider Asia?Pacific region.

About Us

China Briefing is one of five regional Asia Briefing publications. It is supported by Dezan Shira & Associates, a pan-Asia, multi-disciplinary professional services firm that assists foreign investors throughout Asia, including through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Haikou, Zhongshan, Shenzhen, and Hong Kong in China. Dezan Shira & Associates also maintains offices or has alliance partners assisting foreign investors in Vietnam, Indonesia, Singapore, India, Malaysia, Mongolia, Dubai (UAE), Japan, South Korea, Nepal, The Philippines, Sri Lanka, Thailand, Italy, Germany, Bangladesh, Australia, United States, and United Kingdom and Ireland.

For a complimentary subscription to China Briefing’s content products, please click here. For support with establishing a business in China or for assistance in analyzing and entering markets, please contact the firm at china@dezshira.com or visit our website at www.dezshira.com.

- Previous Article China Outbound Direct Investment (ODI) Tracker 2026

- Next Article US-China Relations in the Trump 2.0 Era: A Timeline