The Disproportionate Rise of China’s Real Estate Market

By Nicholas Hopper

Jul. 20 – China’s real estate market has seen massive development since it’s opening to private investors in the late 1990s. This rapid development, not unlike that seen in the United States before the 2008 crisis, is a risky one for several reasons, which we get into below.

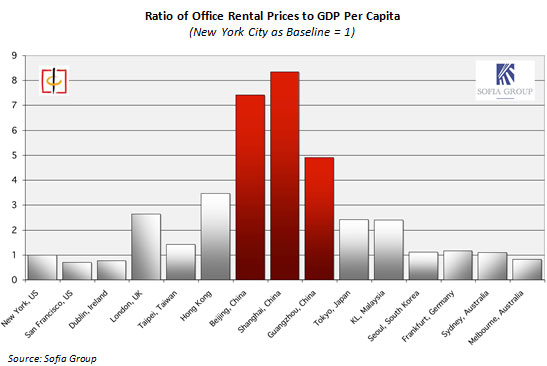

For one, the disproportional value of real estate prices compared to the average citizen’s wages and standard of living has become cause for concern in today’s China. This can be seen when comparing office rental prices across various locations to each country’s GDP per capita, as illustrated by the graph below. Taking New York City as a baseline, Shanghai’s ratio is more than eight times as high, Beijing seven, and Guangzhou nearly five.

Real estate markets in emerging economies often see disproportionate valuation increases mirroring the hopes and expectations that investors have towards the country; with financial centers of such economies especially vulnerable to such speculation. The overvaluation is usually corrected when the market saturates and growth rates return to a sustainable level. Shanghai is of course one example illustrating this effect, and Mumbai is another.

Taking into account average national purchasing power parity, an average Chinese worker would need to save every yuan of their income for over 230 years to be able to afford a 100 square meter apartment in a prime location in Shanghai, according to a recent Knight Frank LLP report. This is topped only by Mumbai, where an average Indian would need to save every rupee they earn for over 300 years.

“Multinational companies from the United States and from Europe are frequently shocked when finding out that labor and material costs in China are still much cheaper than in their home countries, but that office rental rates are often a lot higher,” Bjarne Bauer, commercial director of the Shanghai-based real estate agency Sofia Group, told China Briefing. “The rental cost of the same high quality office space in Shanghai is more than three times higher than in Berlin, for example.”

However, the risk and impact of a potential crash in China’s real estate market cannot be compared to the recent U.S. housing bubble that peaked in 2006 and began to deflate in 2007-2008. China has far more conservative mortgage lending standards (with minimum down payments typically required ranging from 40 percent to 70 percent) and has a growing economy that still consistently maintains high growth rates that could help absorb any potential shock. That being said, property development accounts for roughly 10 percent of China’s GDP. The economy would therefore suffer substantially in cases of major price dumping and development hiatuses, but would most likely be able to recover within a short period of time from any such developments in the coming years.

China’s current trend perhaps best resembles Japan in the 1980s, when prices inflated disproportionately, and then lost 60 percent in value within 10 years. The Chinese government is well aware of this threat and has promised to stop at nothing to gradually deflate any bubble. Over the past year, price caps have been put on new homes, new property taxes have been introduced in some cities, and mortgage lending standards have been tightened.

Wen Jiabao said earlier this month that the government has no intention of letting real estate prices inflate again and places utmost importance on mitigating speculation within the market.

However, concrete policies to curb real estate inflation may prove hard to implement. Because of the volatility of the Chinese stock market and a lack of other viable investment alternatives, many wealthy Chinese people have turned to real estate investments as a way to store their wealth. Furthermore, additional speculation by major real estate companies continues to inflate the market.

Everyone seems to want a piece of the action, as many developers hold units for investment purposes only, and don’t even bother renting them out. Depending on what statistics you use, some 10 million to 65 million units across China are estimated to be held as vacant investment assets. However, despite this oversupply of housing in many metropolitan areas, average Chinese citizens can barely afford housing close to the main cities.

As many aspects of the industry remain fairly unregulated, the future has to show whether the government is able to contain the risks associated with China’s expanding real estate sector. The market needs to gradually saturate and prices need to stabilize while demand catches up, otherwise the consistent development of China’s real estate market may come to an abrupt end.

You can stay up to date with the latest business and investment trends across China by subscribing to The China Advantage, our complimentary update service featuring news, commentary, guides, and multimedia resources.

Related Reading

Report: Mumbai Tops Shanghai as Least Affordable City

Property Prices May Decline in Mumbai. What About Shanghai?

Taxation on Real Estate Rental Income in China

China’s Property Developers Slash Real Estate Prices to Court Buyers

- Previous Article China Reforms Foreign Exchange Administration for Trade in Goods

- Next Article China Issues Guiding Opinions to Regulate Taxation Administrative Discretion