China in 2017 – Increasing Trade Alliances With Eurasia

As we move into another year, we can look back on 2016 with some interesting perspectives on what happened, and reflect on how China’s trade relationships will develop in the coming twelve months. In fact, beyond the usual noise of US-China bilaterial relations, there have been some groundbreaking moves by the Chinese government in how it sees China’s development over the next year and beyond, some of which defy longstanding assumptions and others which show a new path of bilateral and multilateral cooperation. Is your business on top of what is happening in China and where new trade corridors are opening up? Let’s take a look at what’s been happening, and what opportunities are opening up.

China, the United States, and the European Union

It proved to be more of the same in 2016, although China-US bilateral trade actually dropped by 6.9 percent, with a trade imbalance in China’s favor of roughly US$320 billion. The US still purchases far more Chinese goods than any other nation, and is somewhat tied in terms of reducing that reliance as it too, like China, is energy hungry, and is not in a position to sell China what the Chinese are buying – energy and commodities. Chinese-EU trade picked up some nine percent in 2016, yet the same problem emerges – a huge trade deficit of about €180 billion. However, there were encouraging signs in the services industry, with China purchasing more services-related products from the EU than ever before. Part of this may be related to the Russia sanctions issue, with EU businesses unable to supply Russia except via China subsidiaries or partners. Either way, both the US and EU retain the same fundamental problem – neither are producing or capable of producing the commodities and reserves that China is in the market for. This has very specific implications for companies involved in the energy, infrastructure, and commodities trading industries. New, emerging markets and opportunities are arising as China continues its search for both growth and stability. American and European businesses involved in these fields will need to take a different dynamic view than in the past as how they can both assist and benefit from China’s new needs.

China’s overseas direct investment

When assessing the potential for Chinese money to pour into the West, much of the headlines have come from the US, with politicians, businesses, and analysts all betting on a massive increase in China’s overseas direct investment (ODI) spend in years to come. While that may be true, the reality of what this means is lost on many. While American infrastructure may well be creaking and badly in need of investment (two New York commuter train crashes in three months is symptomatic), and brokers and lawyers are licking their lips at the thought of Chinese companies wanting to list on Nasdaq, Chinese foreign investment isn’t actually flocking to America. As I pointed out here, of the actualized US$207 billion China positioned overseas in 2015, the vast majority went to Hong Kong. Latin America received nearly three times more Chinese FDI (US$14 billion) than the United States did (US$5 billion). Also, of the Hong Kong share of US$66 billion, while some of that ended up on the Hong Kong stock exchange in IPOs, a lot would have been round tripping and taking advantage of the Hong Kong-China CEPA Agreement, which provides some preferential tax and licensing treatments to companies based in Hong Kong investing in the mainland. Why would Chinese companies list on Nasdaq when they have Hong Kong?

That is today. What about tomorrow? Analysts are expecting that Chinese ODI will rise to US$305 billion by 2025 and that investment flows from China to the West will start to look more interesting. While America’s railroads – all privately owned – are in dire need of investment, and the Chinese more than capable of providing finance, whether they will want to or even be able to is an interesting point. The US and EU are somewhat estranged from attracting Chinese ODI both politically and also via labor – much of Chinese attractiveness in submitting bids for development projects lies in the caveat that China also provides the labor – a situation that works in other parts of the world but isn’t going to fly far in the West. Additionally, current Chinese ODI trends point to where China can extract maximum and longer term value from its investment. Why spend money on short term Western projects, when it has longer term ‘projects with benefits’ to aim for? In this I specifically refer to the Silk Road, where China wishes to develop considerable infrastructure and can accomplish several goals at once in doing so:

- Secure enhanced and new trading routes across Eurasia;

- Secure access to important mineral and natural resources: energy, water, agriculture, and other supplies;

- Lessen the likelihood of regional conflicts in the near West (Xinjiang etc) by promoting trade;

- Increase political influence over invested and neighboring countries; and

- Generate financial returns.

That concept ticks several boxes for China. Would-be recipients of Chinese ODI should start to realize that in order to attract Chinese money, rather more than a simple financial ROI needs to be in position.

China has already signaled its ODI intention in this regard, and has begun taking steps that illustrate where its current and future ODI is likely to be heading. It isn’t the US or the EU. Instead, China’s real ambitions and intentions for the development of Eurasia can be flagged via a few key development markers. These are:

- Iran and India join the Shanghai Co-Operation Organisation;

- Russia and the Eurasian Economic Union commence tax reforms;

- China expands its DTA scope to include services;

- China and the Philippines “agree to disagree” over the South China Sea;

- India signs an FTA with the Eurasian Economic Union; and

- China signs an FTA with the Eurasian Economic Union.

Of these markers, the first four have all occurred while both China and India have commenced negotiations concerning an FTA with the Eurasian Economic Union. Other potential markers, such as the EU dropping sanctions against Russia, and China agreeing to a deal with the EU, are yet to happen. However, I believe that the message is clear – China’s ODI is going into Eurasia, new trade corridors are beginning to emerge, and businesses globally need to adapt to the idea of Eurasia becoming a new investment and development hub, and position themselves accordingly.

A resurgent China-Russia trade corridor

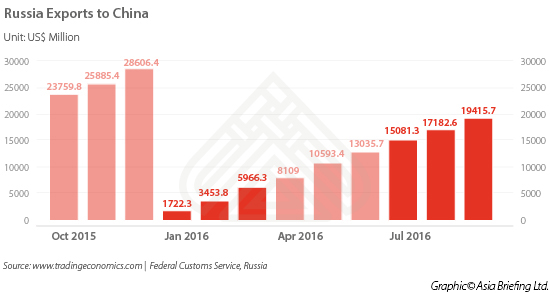

Russia was rarely out of the news last year, and this will continue. While sanctions have had an effect, President Putin has used the opportunity wisely and in fact lessened Russian dependence on EU imports. He has also paid down Russia’s debt at the same time. The damage caused by sanctions have impacted rather more on the EU. New public transport infrastructure in Moscow and Saint Petersburg such as buses and trains, for example, are now sporting Korean and Chinese manufacturer logos instead of European ones. GDP growth is returning in 2017, with the World Bank anticipating 1.5 percent growth this year, coincidentally the same growth rate as can be expected in the EU. In fact, the Russian economy is now on the upswing, while the EU’s is slowing down. The sanctions have also been a boon for Sino-Russian trade, which has significantly picked up over 2016.

As can be seen in the graph below, trade plummeted following the introduction of sanctions, but is now recovering to pre-sanctions levels. The EU’s loss has been China’s gain.

It is also worth remembering that the world’s wealthiest sporting event will take place in Russia next year – the 2018 World Cup Soccer Finals. Russia is spending US$15 billion to host them, and I would expect sanctions to be lifted well before then.

Russia also has commodities that China wants – oil, gas, and vast tracts of agricultural land – all areas in which it can out-compete with the US and EU for generating China trade and investment.

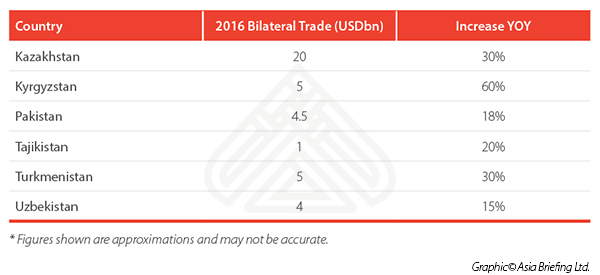

Developing trade ties with Central Asia

Along with the Russian resurgence of trade, Central Asia is also enjoying an increase in bilateral trade with China. Although it can be difficult to obtain precise data from Central Asia, online research of existing local media coverage suggests the following has taken place:

In addition to these trade figures, it is interesting to note that most of the above economies enjoy rather more balanced trade figures than either the US or the EU, mainly because they are exporting oil and gas to China. Additionally, China is making significant investments into these countries, particularly in the same energy sector but also in infrastructure such as road and rail. Chinese trade with these nations may seem small when compared to the huge volumes traded with the West; however, they are becoming increasingly strategically important. Though the West buys cheap Chinese products, Central Asian economies have important commodities to sell in return. These trends can be expected to continue for the foreseeable future, and are reflected in figures that show that China’s western city of Urumqi is a key location in Central Asia – its most populous and its most wealthy.

Urumqi has long been a Central Asian development hub, and is China’s gateway to the Silk Road. Its development can be assessed in that in 2016, its total GDP value was about US$30 billion – similar to Copenhagen – and achieved a 7.3 percent growth rate, one of the highest in China. Businesses looking to enter the China Silk Road market would do well to consider Urumqi as a regional hub from which to operate and direct Central Asian operations. A combination of Chinese, Russian, and Islamic sensibilities, languages, and cultural backgrounds will be required.

Better India ties

China’s trade with India has remained buoyant, at about US$75 billion (the Indian fiscal year runs March-April), although there are concerns that the Chinese side of this equation accounts for a whopping 70 percent of the total. Nonetheless, developing ties and increasing Indian business confidence in China is signaling an increase of Indian investment into China – Dezan Shira & Associates‘ Delhi, Mumbai, and various China offices reported a record high of Indian corporate investments being made into China during 2016, with this expected to double this year. Politically too, both countries have been improving ties. India has been accepted into the Shanghai Co-Operation Organisation, and is also engaged, along with China, in negotiating a Free Trade Agreement with Russia’s Eurasian Economic Union.

Conclusion

China’s trade fundamental relationship with the US and EU is unlikely to alter much in the way of China continuing to satisfy the West’s enjoyment of cheap Chinese products. Large trade imbalances will still remain, although the decline in overall US-Sino trade by nearly seven percent in 2016 must be a concern. The fundamental weakness of both the US and EU economies when it comes to China remains: neither is able to provide in any serious quantities enough products or services to make any impact on their respective trade deficits, although there is at least some good news for the EU in terms of services provision, which is ticking up. In order to show staying power, however, much of this must be geared towards provision of services and technologies that match what China is looking for – energy, commodities, and agriculture.

Meanwhile, the sanctions imposed by the US and EU upon Russia look in hindsight to have been a huge strategic mistake; the EU has effectively lost trade volume estimated at US$60 billion, which China and other markets such as South Korea have been only too happy to pick up on in terms of becoming preferred suppliers. It will be hard for the EU to reclaim these trade flows when sanctions are lifted.

These issues, plus the trends we are seeing vis-a-vis China’s increased trade with Central Asia, Russia, and to some extent Africa and South America, dictate the future when dealing with China. China is increasing trade and investment in countries that can supply it with the products and commodities it wants. It is as simple as that. In order to participate in the new China trade, provision of a simple financial ROI is not enough. Getting involved with China’s ODI and new trade flows means looking at investments from a strategic perspective, knowing the customer, what they want to buy, and why. The new trade routes will be along the Silk Road, and will be harder and less geographically obvious for American and to some extent European businesses to follow. But the trends are clear to see. Is your business prepared to offer China what it really wants in 2017 and beyond?

|

Chris Devonshire-Ellis is the Chairman of Dezan Shira & Associates in Asia, and a consultant to Russia Consulting in Moscow. He is able to advise on all matters of Chinese expansion and development into Asia. Dezan Shira & Associates are a multi-disciplinary practice advising foreign investors throughout Asia, and have offices throughout China, Hong Kong, India, and ASEAN. Please contact the firm at asia@dezshira.com or visit www.dezshira.com. |

China’s New Economic Silk Road: The Great Eurasian Game & The String of Pearls

China’s New Economic Silk Road: The Great Eurasian Game & The String of Pearls

This unique and currently only available study into the proposed Silk Road Economic Belt examines the institutional, financial and infrastructure projects that are currently underway and in the planning stage across the entire region. Covering over 60 countries, this book explores the regional reforms, potential problems, opportunities and longer term impact that the Silk Road will have upon Asia, Africa, the Middle East, Europe and the United States.

Russia Investment Road Map – The e-Commerce Industry

This issue of Russia Briefing shows how you set up your e-commerce business in Russia. E-Commerce in Russia has been posting double digit growth rates for several years, and this trend is set to continue for cross-border e-commerce. This grants good opportunities for Western manufacturers seeking a simple and fast market entry into Russia and its neighboring countries.

China Investment Roadmap: the Food & Beverage Industry

China Investment Roadmap: the Food & Beverage Industry

In this edition of China Briefing, we examine two areas of Chinese food regulations most pertinent for foreign investors today – licensing and certification, and food safety standards. Both have undergone significant change in recent years, altering the way in which foreign companies must engage with the food & beverage industry, and must be thoroughly understood prior to market entry.

Taking Advantage of India’s Improving Business Environment

Taking Advantage of India’s Improving Business Environment

In this issue of India Briefing Magazine, we look at the important regulatory reforms, policy initiatives, and increased incentives for investing in the Indian market that have emerged since Prime Minister Narendra Modi took office in 2014. Foreign companies should take note of the pro-business agenda of the current government and stay updated with the new reforms and sectoral policies that might ease their entry, investment, and expansion of business operations in India.

- Previous Article Navigating Cross Border e-Commerce Regulations in China’s Pet Food Industry

- Next Article Curtain Call: Prospects for Foreign Investment in China’s Culture and Entertainment Industry