Optimizing Employee Take-home Pay in China through Annual Bonuses (Part 1)

SHANGHAI — According to a survey conducted by China Youth, 36.2 percent of employees considered their annual bonus to be a major factor in whether or not they will change jobs in the next year. When determining bonuses, it is critical that employers pay close attention to the calculation of individual income tax (IIT), as this can considerably diminish employee take-home pay. In this two-part article, we detail how employers can reduce the overall tax burden of their employees through carefully balancing salaries and bonuses, and thereby retain valuable talent.

According to the State Administration of Taxation’s Announcement No. 9, 2005 (Guo Shui Fa [2005] No.9), IIT on annual bonuses should be calculated as explained below.

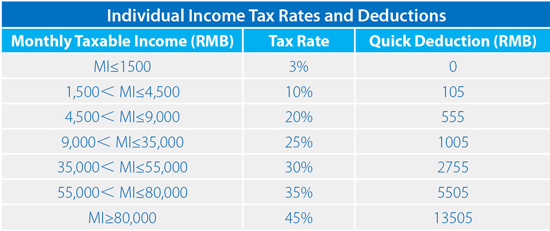

Step 1 — Determine the applicable IIT tax rate and quick deduction

The employer should first divide the lump-sum annual bonus by 12 to determine the applicable tax rate and quick deduction amount. The chart below shows the applicable IIT tax rate and quick deduction for each IIT tax bracket.

For example, if employee “A” receives a lump-sum annual bonus of RMB 120,000. According to the chart, the applicable tax rate should be 25 percent (120,000/12=10,000), and the quick deduction amount should be 1005.

Additionally, if employee “B” receives an annual bonus of RMB 13,000, with a monthly wage of RMB 4000 and deductible expenses amount of RMB 5000, then monthly taxable income will be calculated as: [13,000 – (5000-4000)]/12=12,000/12=1,000. According to the chart, the applicable tax rate should be 3 percent and the quick deduction amount will be zero. If the employee’s monthly wage is less than the deductible expenses amount stipulated in the Tax Law, the tax rate and quick deduction amount should be determined based on the formula: [annual bonus – (deductible expenses amount – monthly wage)]/12. The deductible expenses amount is set at the regional level based on local social insurance standards.

Step 2 — Determine the applicable formula

There are two basic formulas for calculating IIT on annual bonuses. First, if the employee’s monthly wage is more than (or equal to) the deductible expenses amount stipulated in the Tax Law, the applicable formula shall be:

IIT on lump-sum annual bonus = lump-sum annual bonus x applicable tax rate – corresponding quick deduction amount

To illustrate, for employee “A”, whose annual bonus is RMB 120,000 (subject to a 25 percent tax rate and quick deduction amount of 1005), IIT should be paid based on:

IIT on the lump-sum annual bonus = RMB120, 000 x 25% – RMB1, 005 = RMB28, 995

Second, if the employee’s monthly wage is less than the deductible expenses amount stipulated in the Tax Law, the applicable formula shall be:

IIT on lump-sum annual bonus = [lump-sum annual bonus – (deductible expenses amount – monthly wage)] × applicable tax rate – quick deduction amount

For employee “B”, whose annual bonus is RMB 13,000 (subject to a 3 percent tax rate and quick deduction amount of 0), IIT should be paid based on:

IIT on the lump-sum annual bonus = [RMB13,000 – (RMB5000 – RMB4000)] x 3% – RMB0 = RMB360

Notably, the annual bonus here refers to that given to employees prior to tax deductions. If the employer pays part of the IIT on employee annual bonuses, the amount paid will be regarded as part of the employee’s taxable annual bonus according to the State Administration of Taxation’s Announcement No. 28 issued, 2011 (SAT Announcement [2011] No. 28), which further complicates the issue of IIT calculation.

In Part 2 of this article, we introduce IIT calculation methods for foreign employees under different circumstances, and discuss how to strategically reduce the related tax burdens.

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email china@dezshira.com or visit www.dezshira.com.

Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

Related Reading

The China Tax Guide: Tax, Accounting and Audit (Sixth Edition)

The China Tax Guide: Tax, Accounting and Audit (Sixth Edition)

This edition of the China Tax Guide, updated for 2013, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in China, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in China in order to effectively manage and strategically plan their China operations.

Social Insurance in China

Social Insurance in China

In this issue of China Briefing Magazine, we introduce China’s current social insurance system and provide an update on the status of foreigners’ participation in the system. We also include a comprehensive chart of updated average wages across China, which is used to calculate social insurance contribution floors and ceilings. We hope this will give you a better understanding of the system in China.

Revisiting China’s Value-Added Tax Reform

Revisiting China’s Value-Added Tax Reform

In this issue of China Briefing Magazine, we review recent steps taken by the Chinese government to reform its value-added tax policy. Specifically, we examine the sectors covered by the new Pilot Reform program with a focus on tax rates, taxpayer status and the calculation of VAT. We also include a VAT Pilot Reform Rates Chart, which overviews each affected industry’s tax rate and VAT exempted services.

- Previous Article Xi’s Visit to India & Sri Lanka Promises Infrastructure, Shipping & Tourism

- Next Article Golden Years: The Coming Investment Boom in China’s Elderly Care Industry