Hong Kong BEPS Bill: New Transfer Pricing Regime to Regulate Documentation

By Paul Dwyer, Director, Head of International Tax and Transfer Pricing

On December 29, 2017, the Inland Revenue (Amendment) (No. 6) Bill 2017 (BEPS bill) was gazetted in Hong Kong. The BEPS bill introduces a transfer pricing regulatory regime and mandatory transfer pricing documentation requirement in Hong Kong as well as a variety of other anti-BEPS changes.

The BEPS bill marks a significant step up in Hong Kong’s transfer pricing enforcement regime and was formally introduced into the Legislative Council on January 10, 2018. The BEPS bill is a lengthy document and as such it is expected to take a few months before it can be enacted.

On the basis of the arm’s length principle, the BEPS bill proposes fundamental transfer pricing rules that further empower the Inland Revenue Department (IRD). This includes the ability to adjust the profits or losses of an enterprise where the actual provision made or imposed between two associated persons departs from the provision that would have been made between independent persons and has created a tax advantage.

The BEPS bill further introduces mandatory documentation requirements based on the three-tiered approach of Country-by-Country (CbC) Reporting, Master File, and Local File. The BEPS bill also provides further details into the Advance Pricing Arrangement (APA) programme and other related provisions.

In addition, the 2017 version of the Organization for Economic Cooperation and Development’s (OECD) transfer pricing guidelines is cited in the BEPS bill as the version to follow along with the OECD Model Tax Convention on Income and on Capital.

The BEPs bill introduces a more comprehensive transfer pricing regime to Hong Kong. Businesses with a presence in Hong Kong should review the new developments to ensure compliance with the new rules, which are more expansive than anticipated.

![]() RELATED: Transfer Pricing Investigation in China

RELATED: Transfer Pricing Investigation in China

Key provisions of the BEPs bill

The BEPS bill confirms most of the key provisions that were proposed in the Consultation Report on Measures to Counter Base Erosion and Profit Shifting (Consultation report), which was released late last year. We have set out a summary of these key provisions below:

Requirements and exemption thresholds for Master File and Local File

- Hong Kong constituent entities of a group will be required to prepare a Master File and a Local File for each accounting period beginning on or after April 1, 2018.

- The Master File and Local File must be prepared within six months after the end of the entity’s accounting period. However, the BEPS bill does not state whether these documents need to be submitted to the IRD.

- The information items to be included within the Master File and the Local File are largely in-line with the OECD’s guidance.

- Taxpayers will not be required to prepare Master and Local Files if they meet either of the following two sets of exemptions:

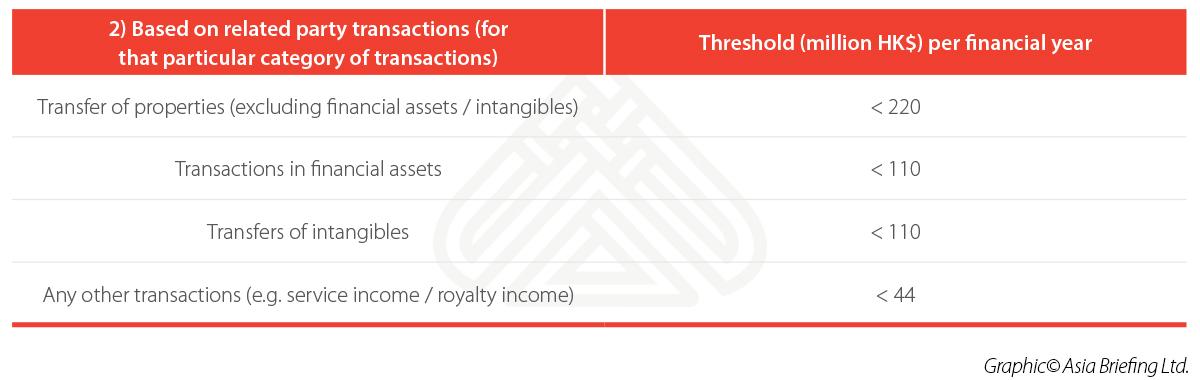

- If the amount of a category of related party transactions for the relevant accounting period is below the respective threshold, the entity will not be required to prepare a Local File for that category of transactions.

- If all of an entity’s controlled transactions are exempted by the above related party transaction criteria, the entity is not required to prepare both the Master File and the Local File.

Country-by-Country Reporting

- Reportable groups whose annual consolidated group revenues exceed HK$6.8 billion (€750 million) will be required to file a CbC report for accounting periods beginning on or after January 1, 2018.

- Each Hong Kong entity of a reportable group must file a written notification informing within three months after the end of the accounting period.

- Reportable groups with Hong Kong tax-resident Ultimate Parent Entities (UPE’s) may voluntarily file CbC returns for accounting periods beginning on or after 1 January 2016 but before 1 January 2018.

Related enterprises

- The fundamental transfer pricing rules apply to cases where the affected persons are associated. This means one affected person is directly or indirectly participating not only in the management or control of the other but also extends to its capital.

- If a third person is participating in the management, control, or capital of both affected persons, they would also be considered as associated.

Permanent establishments

- The transfer pricing rules will also apply to the dealings between different parts of an enterprise, such as between the head office and a permanent establishment (PE).

Intellectual property

- The BEPS bill adds provisions in the Inland Revenue Ordinance (IRO) to ensure that non-resident persons carrying out the function of Development, Enhancement, Maintenance, Protection and Exploitation (DEMPE) of intellectual property in Hong Kong will be taxed on the basis of that person’s contribution in carrying on such functions.

Advance pricing arrangements

- The BEPS bill has included provisions that allow taxpayers to apply not only bilateral and multilateral advanced pricing arrangements (APAs) but also unilateral APAs.

Penalties

- An administrative penalty relating to transfer pricing is introduced.

- The BEPS bill proposes to set the administrative penalty at a level lower than the existing one for other non-compliances under section 82A of the IRO.

- Specifically, the taxpayer will be liable to an administrative penalty by way of additional tax not exceeding the amount of tax undercharged.

- The BEPS bill also specifies that any director or officer committing an offense is liable on conviction to the penalty provided for that offense.

![]() Transfer Pricing Solutions from Dezan Shira & Associates

Transfer Pricing Solutions from Dezan Shira & Associates

Developments in line with international practice

The BEPs bill is poised to bring Hong Kong’s transfer pricing regime closer in line with international standards. The bill, however, is more comprehensive than expected, and contains some unanticipated additions. For example, the requirement to prepare the Master File and Local File within six months after the end of the accounting period is a significantly shorter timeframe than expected.

It is important that companies assess their current business operations and continue to monitor the situation to enable adequate compliance. This is the case even if companies do not meet the requirements to prepare Master and Local file documentation. In light of the IRD’s focus on related party transactions, it is imperative that companies ensure they have a reasonable charging mechanism in place and that any related party payments made in Hong Kong are arm’s length in nature.

|

China Briefing is published by Asia Briefing, a subsidiary of Dezan Shira & Associates. We produce material for foreign investors throughout Asia, including ASEAN, India, Indonesia, Russia, the Silk Road, and Vietnam. For editorial matters please contact us here, and for a complimentary subscription to our products, please click here. Dezan Shira & Associates is a full service practice in China, providing business intelligence, due diligence, legal, tax, IT, HR, payroll, and advisory services throughout the China and Asian region. For assistance with China business issues or investments into China, please contact us at china@dezshira.com or visit us at www.dezshira.com

|

Dezan Shira & Associates Brochure

Dezan Shira & Associates is a pan-Asia, multi-disciplinary professional services firm, providing legal, tax and operational advisory to international corporate investors. Operational throughout China, ASEAN and India, our mission is to guide foreign companies through Asia’s complex regulatory environment and assist them with all aspects of establishing, maintaining and growing their business operations in the region. This brochure provides an overview of the services and expertise Dezan Shira & Associates can provide.

An Introduction to Doing Business in China 2017

This Dezan Shira & Associates 2017 China guide provides a comprehensive background and details of all aspects of setting up and operating an American business in China, including due diligence and compliance issues, IP protection, corporate establishment options, calculating tax liabilities, as well as discussing on-going operational issues such as managing bookkeeping, accounts, banking, HR, Payroll, annual license renewals, audit, FCPA compliance and consolidation with US standards and Head Office reporting.

In this issue of China Briefing magazine, we analyze macro-level foreign investment trends into China, and how the high-tech sector stands out above others. We then shift our focus to China’s healthcare sector in the context of policy reforms and demographic changes. We also examine how to invest in China’s education industry and how China’s war on pollution introduces new opportunities for foreign investors.

- Previous Article China-France Relations Gaining Momentum in 2018

- Next Article Britain Needs to Get Serious about Business with China and the Commonwealth